8.1: Bond Basics

- Page ID

- 79783

Bonds are negotiable, publicly traded long-term debt securities. The issuer of the bonds agrees to pay a fixed amount of interest over a specified period of time and to repay a fixed amount of principal at maturity. Bonds are also known as Fixed-income Securities, Fixed Investments, or Debt Financing. A bond is basically an IOU issued by corporations, a state or local municipality such as a state, city, or school district, or the Federal government. The bond investors loan their money to the bond issuers. Bond investors are loaners as opposed to stock investors who are owners. The bond issuers agree to repay the money they borrowed with interest.

When a bond is issued, a document is created called the trust indenture. The trust indenture is the contract that sets forth the terms between the issuer and the bondholders. The indenture describes the bond investors’ rights and issuer’s obligations. A trustee is appointed to oversee that these obligations are carried out. The trustee is usually a commercial bank or a trust company. The trust indenture stipulates protective covenants, such as an obligation of the bond issuer to keep doing business, to keep equipment in good working order, to make payments on time, etc. For example, recently, the college where I teach, Southwestern Community College in Chula Vista, California, issued bonds to build a new stadium and the other new buildings. In the trust indenture is a protective covenant that states that the money received from the bond issue must be used for “capital improvements,” a fancy term for either new building or restoring old building. In other words, we could not use the money to give the staff and faculty raises.

Why Invest in Bonds?

Bond investors receive interest during the life of the bond. The interest is normally paid every six months. When the bond is redeemed at the end of the life of the bond, the principal is returned to the bond holder. Bonds mature anywhere from 1 to 30 years. However, bond terms are typically in the 20-to-30-year range. One might think of bonds like a mortgage, a long-term loan where the payments are stretched out over many years.

With bonds, there is also the potential for a capital gain or a capital loss. The potential capital gain or capital loss is normally much less than what is exhibited by stocks. “Wait a minute,” you ask, “how could there be a capital gain or capital loss on a loan? That doesn’t make sense. Wouldn’t the amount of the loan remain constant?” Yes, you are correct. The principal remains constant throughout the bond’s life but the price of the bond will fluctuate as interest rates fluctuate. We will discuss the relationship between interest rates and bond prices in detail soon. If interest rates fall, there is a potential for a capital gain but there is also a potential for a capital loss if interest rates rise. However, if you intend to hold the bond to maturity when your principal is returned, capital gains or losses will not affect you.

Some bonds offer tax advantages. We will see that municipal bonds are free from Federal income taxes and Treasury bonds are free from state and local taxes. Lastly, some bonds can be converted into stocks. These are called convertible bonds and they give us the opportunity for outsized capital gains if the underlying stock does well. That might sound exciting but these are bonds, remember? Bonds are boring. Convertible bonds rarely deliver in a big way for their investors. We will cover “convertibles” when we discuss hybrid securities in a later chapter.

Bond holders are first in line for repayment if there is default on the loans. Actually, any payroll or tax expenses must be paid first. Guess who is at the end of the line. That’s right, the stock investors. When a company goes through bankruptcy, the bond investors get to pick at the carcass first. By the time they are through, there is invariably nothing left for the stock investors. Just as most people pay their home mortgages and car loans, etc., most all bond issuers pay their interest payments and repay the principal. For this reason, bond prices are far less volatile than stocks. However, bond prices still fluctuate. Bond prices can go down and do go down when interest rates rise. Again, we will discuss this inverse relationship in detail later.

What kind of long-term results can we expect from bonds? For several decades, bond investors became accustomed to typically being paid between 4% and 8% on a diversified bond portfolio. Treasury and municipal bonds paid 4% to 5% while corporate bonds paid 6% to 8%. For several years, the return on bonds has been much, much less. Recently, they are beginning to rise again. As of May 2023, Treasury bonds were paying 4% to 4½%. Municipal bonds were paying between 3% and 4½%. High-quality corporate bonds were paying 4% to 6% while some lower quality, riskier corporate bonds were paying over 7%. Not surprisingly, this has renewed interest in bonds on the part of bond investors after many years of uninspiring returns.

Bonds versus Stocks

Over the long term, stocks have outperformed bonds. So why invest in bonds? Stocks are far more volatile and carry more risk than bonds. Bonds offer an element of stability to your portfolio. For some investors, stocks are simply too risky. They reason, “If I can obtain my long-term goals without taking on the risk of being invested in stocks, so be it.” Some call this the “I-Can-Sleep-Better-At-Night” factor. The investor’s time frame should also be considered. Bonds make good intermediate-term investments while stocks are better thought of as good long-term investments. And sometimes, bonds are just screaming good deals. Who wouldn’t want to earn 8% or 9% on a high-quality, fixed-income investment that had a very small probability of default? The last time that bonds offered these opportunities was in the 1980’s.

Even though stocks have performed better than bonds over time, there have been periods of time when bonds have outperformed stocks, sometimes for long periods of time. The last major example of this was the 2000’s, sometimes called the Lost Decade for stocks. The 10-year average annual return was approximately -1%. Before that you have to go back to the Great Depression to see a negative 10-year average annual return. However, I am going to tell you the truth, even though as a licensed investment professional, I could have my license revoked for saying it to a potential client. Stocks must outperform bonds over the long term. Why is this so? The reason for this comes from the fundamental structure of our capitalist society.

Corporations pay the interest and principal on the bonds that they issue mainly from their earnings. If the economy and the stock market have crashed … and subsequently don’t recover, then that means corporate and private individual earnings have evaporated and our society is in shambles. With no corporate earnings, it is only a short matter of time before the corporate bonds default and become worthless. Municipalities such as state and local governments and the United States Treasury rely on corporate and individual taxes to pay the interest and principal on the bonds that they issue. If corporations and private individuals are not producing earnings, then they are not paying taxes. Likewise, it is only a short matter of time before the municipal and Treasury bonds default and become worthless. Of course, we are discussing a situation where there is no food at the grocery stores, no gas at the service stations, no clothes at the mall, the cell phones and the gas and electric companies are no longer providing service, the schools, the banks, the hospitals, the fire departments, the police stations, etc., are all boarded up, and there are brown-shirted individuals driving around with guns attached to their vehicles, using up what little resources are left to scavenge. In this case, your stock and bond investments will be the last items on your list of things to concern yourself about.

Failure is not an option. We must never let this doomsday scenario become a reality. Hence, corporations and private individuals must thrive. Over the long term, for our capitalist society to survive, stocks must perform better than bonds. Sports analogies are always a slippery slope. However, I always like to think of stocks as baseball and bonds as football. In football and most other games that are played on a rectangular field, one must stay within the boundaries of the field. Their world is fixed, like bonds. In baseball, theoretically, the foul lines are open-ended and extend indefinitely, like stocks. The world of bonds is bound. The world of stocks is limitless. I think so.

The Risks Associated with Bond Investments

Although bonds are far less risky than stocks, there are still several risks that need to be taken into consideration when investing in bonds. The first is interest rate risk. Interest rate risk comes from the inverse relationship of interest rates and bond prices. As we will cover in detail, when interest rates rise, bond prices fall. If you intend to sell the bonds in the future before they mature, a rise in interest rates can translate into capital losses. If you plan to hold your bonds until maturity, interest rate risk is not an issue you would need to consider.

Purchasing power risk is the risk that your purchasing power will fall if inflation outstrips your return from bonds. Inflation is the bond investor’s worst nightmare. If inflation runs out of control, the dollars a bond investor receives in interest and principal repayments are worth far less and the investor’s purchasing power is gutted. Business risk and financial risk are risks that are shared by both stocks and bond investors. For bond investors, business failure or financial failure on the part of the bond issuer may result in default on interest payments or principal repayments. This is much less a problem with municipal bonds although some municipalities have gone bankrupt in the past. Except for the occasional political theatrics practiced in our nation’s capital, the United States Treasury has never defaulted since the founding of the Republic and will not default anytime within our lifetimes or our children’s children’s lifetimes, unless some politicians who are far less responsible than children have their way.

Some bonds exhibit liquidity risk, the risk that there may not be sufficient buyers when and if an investor wants to sell their bonds before maturity. This is less of a problem with municipal and Treasury bonds. It could be a serious problem with thinly traded bonds. However, with high-quality bonds, it is normally not something that an investor needs to concern themselves with. For investors who plan to hold their bonds to maturity, this risk is not an issue.

The last risk is call risk, also called prepayment risk. This is the risk that a bond will be “called away” from the investor before its scheduled maturity date. This is similar to what happens when a homeowner decides to prepay their mortgage and refinance with a new mortgage, normally in response to falling interest rates. The bond investor receives their principal. However, since interest rates have fallen, the bond investor must now invest in lower-yielding bonds. For this reason, some bond issuers offer non-callable or deferred-callable bonds. We will discuss the call feature of some bonds in detail soon.

Bond Interest, Principal, and Maturity

The feature of a bond that defines the amount of annual interest income is called the coupon rate. It also goes by the names nominal rate, coupon yield, and nominal yield. Interest on bonds is usually paid every six months, although some bonds pay from every month to quarterly to once a year. The term “coupon rate” came from the fact that bonds used to have coupons attached to them. When the interest was due, an investor was required to send the coupon into the bond issuer and the issuer would then send the bondholder the interest. To this day, earning interest from a bond is often called “clipping the coupon” even though now virtually all transactions are done electronically.

The amount of the loan and the amount of capital that must be paid at maturity is called the principal. (Careful. Principle is a different word with a different meaning.) The principal is also referred to as the par value or face value. The principal of most bonds is $1,000. Another way of saying this is that bonds are denominated in $1,000 increments. There are some bonds that are denominated in $5,000 and $10,000 increments. However, for our journey together, we will always use $1,000 as our denomination, our par value, our face value, our principal.

Putting the coupon rate and principal together tells you how much interest you will receive each year. For example, a coupon rate of 7% and a principal of $1,000 gives $70 of interest each year. And since almost all bonds are denominated in $1,000 increments, knowing the coupon rate gives you the amount of interest. Therefore, normally bond investors simply refer to their bonds by the coupon rate and maturity. “I bought a 7% 30-year bond.” So if we ask you what the annual interest on a 7% bond is, you will say, “$70.” For a 5% bond, it will be $50. For a 3% bond, $30. Careful: A 10% bond would yield $100 of annual interest whereas a 1% would yield $10.

The maturity date is the date on which a bond matures and the principal must be repaid. Most bonds are term bonds. Term bonds mature all at once. For example, a company will issue 20-year bonds that all mature in 20 years on the same date. There are also serial bonds. Serial bonds have a series of maturity dates. For example, a company may issue “series” of 20-year serial bonds with 20 maturity dates, each series maturing each year for 20 years. Each year, a certain portion of the issue would come due and be paid off as that series matures.

Technically, there is a difference between a bond and a note. Notes mature in 2 to 10 years whereas bonds mature in 10 or more years, usually 20 to 30 years. Some bonds mature in 50 or 100 years. Recently the Government of México issued 100-year bonds. A very small number of bonds never mature. They are often referred to as perpetuities or consols. Examples of these are railroads and other industries that had their starts in the 19th century. Although there is technically a difference between a 10-year note and 30-year bond, most investors, including Your Humble Author, use the term bond to refer to both bonds and notes.

The Call Provision on Bonds

As briefly mentioned above regarding the risks of bonds, many bonds have a call provision. The call provision specifies whether and under what circumstances the bond issuer can retire the bond prior to the maturity date. If interest rates drop, just as a homeowner would want to refinance their mortgage, a bond issuer would want to refinance their bond loans. The issuer “calls in” the bonds. The bonds are “called away” from the bond investor. This is also called prepaying the bonds. All other factors being equal (and they never are), investors would prefer non-callable bonds to callable bonds.

There are three types of call provisions. Freely callable bonds can be retired at any time. With non-callable bonds, the issuer is prohibited from retiring the bond before the maturity date. The third type is a hybrid of the first two. A bond with a deferred call states that the issuer must wait for a certain length of time to pass before the bonds can be called. This length of time is referred to as the call protection period or call deferment period. Most corporate and municipal bonds are freely callable or have a deferred call. Treasuries have always been non-callable. Which of the above provisions is the least desirable? Which is the most desirable? Obviously, a non-callable bond is more desirable than a freely callable bond with bonds with a deferred call somewhere in between. Of course, all other factors being equal (and again, they never are), you can expect to receive less interest from a non-callable bond than a callable bond since non-callable bonds carry the call risk whereas non-callable bonds do not.

Some callable bonds will have a call premium, an amount that is added to a bond’s par value and paid to investors if and when a bond is retired prematurely. For example, a bond might have a call premium of $85 that must be paid in addition to the principal if and when the bond is called away from the investor. This is similar to the “prepayment penalty” that some loans such as home mortgages have. The call price, also known as the redemption price, is the price the bond issuer must pay to the bond investors in order to retire the bond prematurely. It is equal to the par value plus the call premium. In our example, $85 call premium is added to the par value of $1,000 to give us a $1,085 call price. If there is no call premium, the bond is said to be “callable at par.”

Bonds and Interest Rates

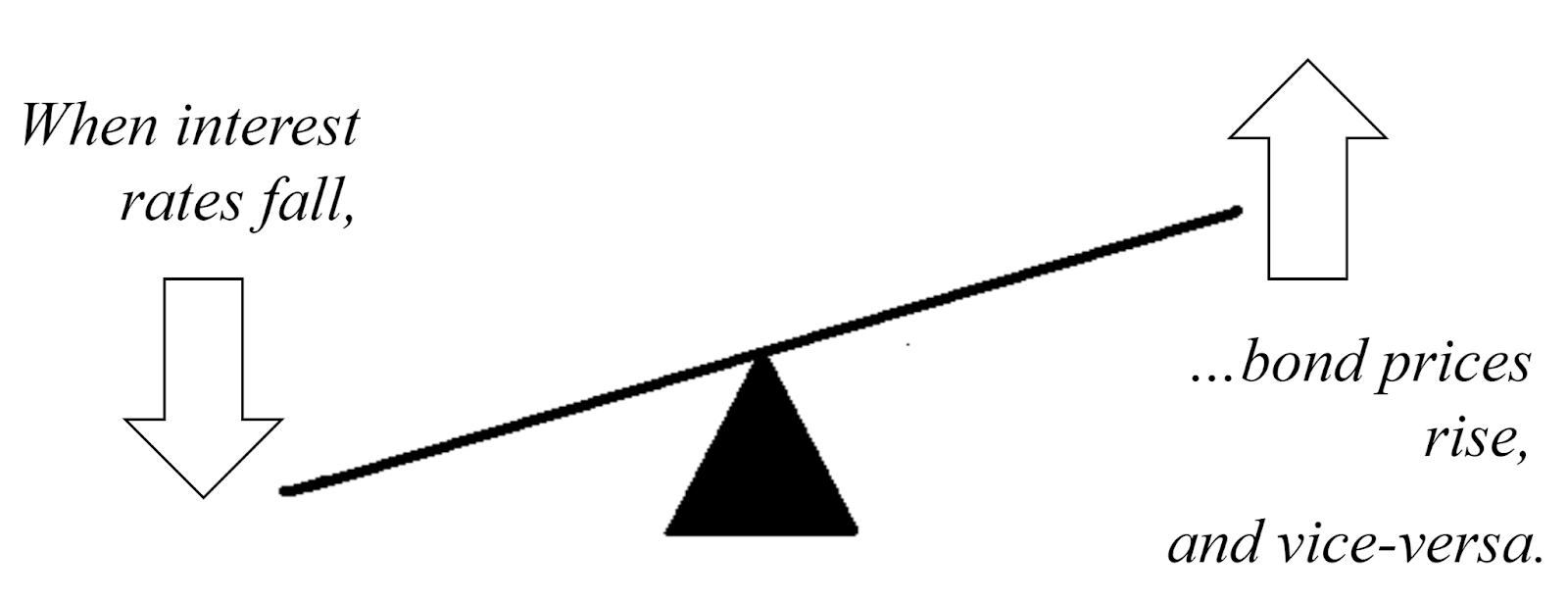

By far, the most misunderstood feature about bonds is their inverse relationship with interest rates. When interest rates fall, bond prices rise. When interest rates rise, bond prices fall. For many investors, the image of the playground seesaw is helpful.

Keep this image front and center in your mind when thinking about bonds. The inverse relationship of interest rates and bonds trips up everyone, even seasoned professionals.

Because of this ongoing relationship, the current market value of a bond could be greater than or lesser than the par value. A premium bond is a bond with a market value greater than the par value. This occurs when prevailing interest rates drop below the coupon rate of the bond. A discount bond is a bond with a market value lower than par value. Contrariwise, this occurs when prevailing interest rates are greater than the coupon rate. A bond selling at a discount to its par value can also occur when and if the investment community believes that the bond issuer is in danger of defaulting on interest payments or principal payments. If there is no premium or discount, the bond is said to be “selling at par.”

You may be wondering, “Wait a minute. Why would a bond sell at a premium or a discount to its par value? If the loan is for $1,000, the bond would always sell for $1,000, right?” No, this is not the case. Since the interest rate of your bond is fixed and cannot change, the price of the bond changes to reflect the change in the prevailing interest rates within the financial industry. Again, keep the image of the see-saw in your mind. Interest rates go down, bond prices go up. Interest rates go up, bond prices go down.

Let’s take a look at an example. You own a bond with a par value of $1,000. (Remember, in our class, all bonds will have par values, also known as face values, of $1,000.) It has a coupon rate of 10%. That means it is paying you $100 every year. (It actually will pay you $50 every six months. Picky, picky, picky.) Now what happens if two years after you purchase the bond, interest rates fall to 8%? New bonds with $1,000 par values are only paying $80 per year, $40 every six months. The result is that your bond is now worth more than it was. You would not sell your bond for $1,000 since now investors have to pay $1,250 to get the same amount of interest. You could sell your bond for more than $1,000. You would receive a capital gain on the sale of your bond.

What happens if interest rates rise? If we purchased the same 10% bond and then a few years later, interest rates rise to 12%, now investors only need to pay $833.33 to get the same amount of interest as your bond is paying. New bonds are paying $120 and investors only need to spend $1,000 to get that $120. The result is you could not get anyone to buy your bond for $1,000. If you wanted to sell, you would need to lower the price of your bond to attract a buyer. If you sold now, you would realize a capital loss. Your bond would be sold at a discount. Of course, if you have no plans to sell your bond, you will still receive the $100 each year until the bond matures and you receive your principal of $1,000 back.

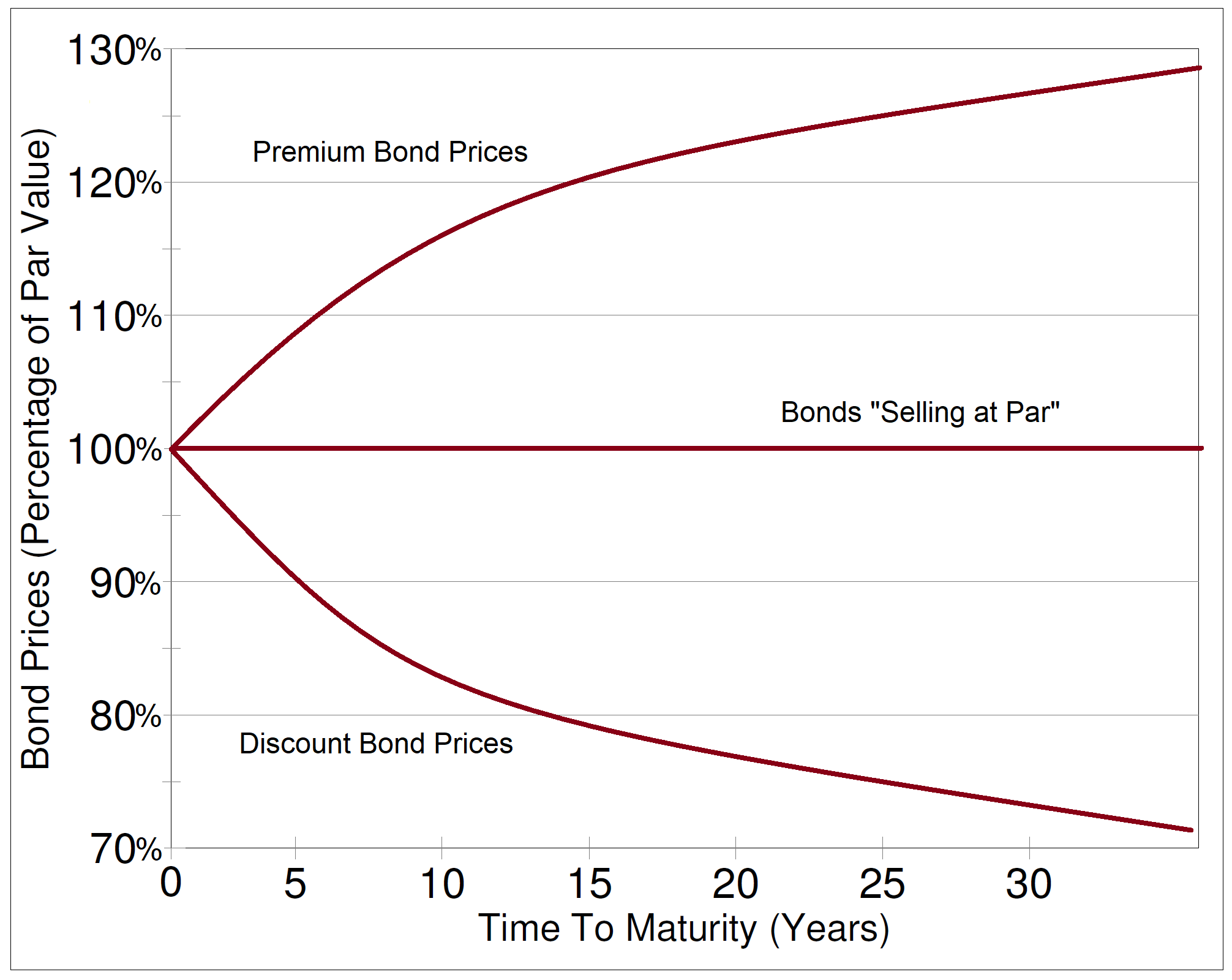

The amount of the premium or discount is not only related to the amount of the fall or rise of interest rates. In general, the greater the fall or rise in interest rates, the greater the premium or discount. The maturity date is also very important. In general, the longer the maturity, the greater the premium or discount. Just like a seesaw, the farther out you are, the greater the rise or fall. This is why long-term bonds are riskier than short-term bonds.

In the graphic above, we see that the farther you are out on the see-saw, the more dramatic the rise or fall. The same is true of the maturity of your bonds and the bond prices. The longer the time to maturity, the more dramatic the rise or fall of the bond price will be as interest rates fall and rise. The shorter the time to maturity, the less pronounced the rise or fall of the bond price.

In the graphic above, we see as bonds get closer and closer to their maturity date, the closer and closer the price of the bonds will get to their par values. In general, long-term bonds exhibit greater price volatility and a greater opportunity for capital gain or loss. Intermediate-term and short-term bonds exhibit less price volatility with a lesser opportunity for capital gain or loss. Bonds very close to maturity ‒ three, six, or nine months ‒ start to behave similarly to short-term investments such as commercial paper and Treasury bills. However, if you intend to keep the bonds until they mature, then you are not concerned about the price volatility. You will always receive the par value of the bond except in the rare case of a bond default.

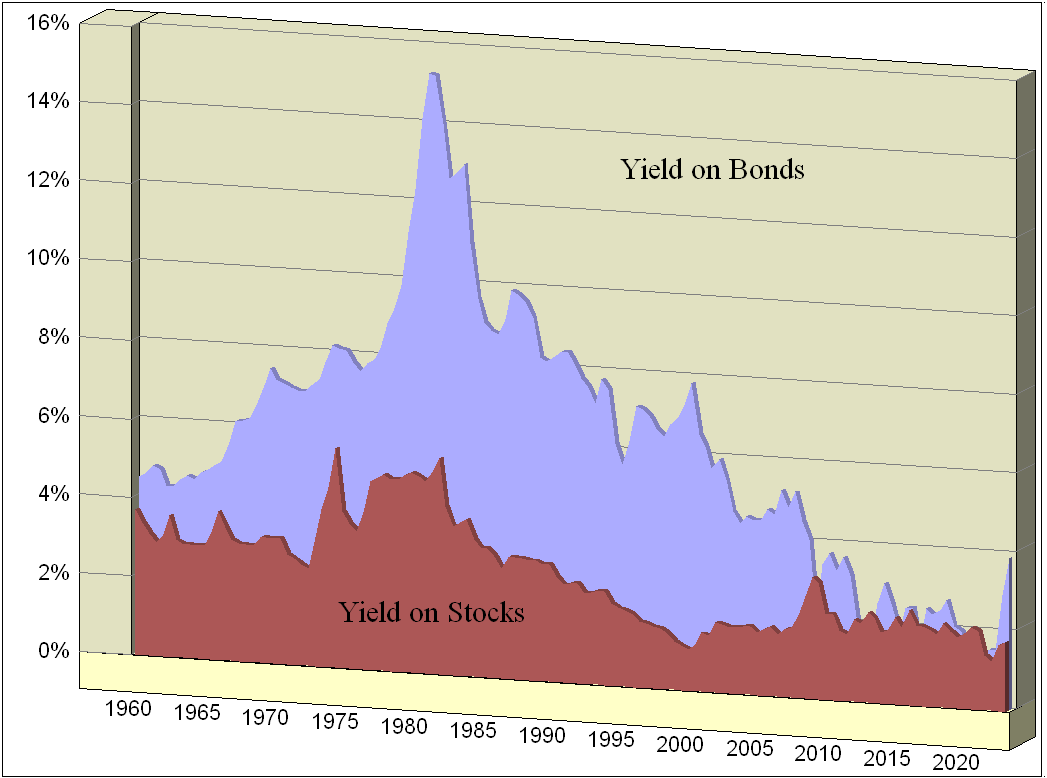

We revisit this graphic from our Introduction to Stocks chapter. We see that in 1960, the yields on bonds and stocks were very close. As inflation took hold in the 1970’s, bond investors demanded higher and higher yields. After the Federal Reserve Bank broke the back of inflation in the late 1970’s and early 1980’s, the yield on bonds fell more or less consistently until 2022 when the Federal Reserve Bank again began raising interest rates to curtail inflation caused by the effects of the COVID pandemic on the global economy. Subsequently, bond prices fell as interest rates rose and bond investors experienced a rare occurrence, negative bond returns for the year. As mentioned, bond investors have begun sniffing out attractive yields on bonds for the long term. Are they right? Is now a good time for long-term investors to invest in bonds? We will know in a few years. Stay tuned! In the meanwhile, would you be happy with 5% to 6% on 20-year corporate bonds? Do you want to eat well or do you want to sleep well?