8.2: Types of Bonds

- Page ID

- 79784

Let’s review the major bond types. We will start from the least risky to the most risky types of bonds.

Treasury Bonds and Notes

“Flight to quality!” When you hear these words, you know that someone is talking about Treasury bonds. Treasury bonds, or just “Treasuries,” are the safest bonds available. When some shock happens in the world, whether it be economic or political or a natural disaster, you can always count on Treasury bonds to shine. Some professionals tell their clients that they should think of Treasury bonds as air bags. In a crash, they inflate and will protect a portfolio from catastrophic disaster. You most likely have heard one or two wingnut radio or Internet commentators rail about the national debt being unconstitutional and that Treasury bonds will become worthless and that the United States government will default. Yes, we have a serious debt problem that will cause us pain in the future. However, the United States will pay its debts.

An example of the Flight to Quality was during the Global Financial Crisis of 2008 and 2009. All major investment classes fell sharply, stocks, mutual funds, oil and other commodities, real estate, and even most bonds, that is, except for Treasury bonds. Treasury bonds became scarce and their prices went up even as the supply increased. Another example of the topsy-turvy world of investment came in 2011 when political brinkmanship between the Obama Administration and the Republicans in Congress prompted Standard and Poor's to lower the credit rating of Treasury bonds. Typically, when an individual or corporation or any other entity has their credit rating lowered, the interest rates they must pay to borrow rise. This was not so with the United States Treasury! Treasury bond prices actually increased and interest rates fell as investors once again sought Treasury bonds as a safe haven from the turmoil.

Don’t forget that 2-year to 10-year Treasury notes are technically different from 20-year to 30-year Treasury bonds but also remember that there are many of us who just don’t care about the distinction. However, don’t confuse Treasury notes and bonds with Treasury bills which are short-term investments that use the discount method for paying interest. Treasury notes and bonds pay interest every six months and then repay the principal upon maturity.

So far, the Treasury has never issued anything other than non-callable notes and bonds. The interest on Treasury notes and bonds is exempt from state and local taxes but not Federal tax.

An increasingly popular Treasury offering are Treasury Inflation-Protected Securities, often referred to as “TIPS.” TIPS are guaranteed to keep pace with inflation and as such, remove one of the risks associated with bond investing, purchasing power risk, also known as inflation risk. TIPS pay much less interest than other Treasury bonds. However, every year, the par value principal is adjusted upwards according to the rate of inflation as measured by the Consumer Price Index (CPI). Hence, if inflation for the year were 5%, a $1,000 TIPS bond would rise $50 ($1,000 * 5%) and the new par value would be $1,050. Accordingly, next year’s interest would be based on the new par value so the bond investor’s interest would also rise. TIPS are very popular with investors who fear inflation. One disadvantage of TIPS is that the IRS requires a bond investor to pay income tax on the increase in par value, even though the investor did not receive the price rise in cash. This is known as phantom income.

Often associated with Treasury bonds and notes are agency bonds. Agency bonds are not direct obligations of the United States Treasury. They are offered by agencies that were initially sponsored by the Congress. Technically, they do not have the same weight as Treasuries, but they are considered very safe with almost no risk of default. Time and time again for decades, our government officials would swear that these entities were not backed by the full faith and credit of the United States Treasury and would not be bailed out in case of a default. This was the case until the Global Financial Crisis of 2008. Subsequently, Uncle Sam had to go back on his word and bail them out. These agency bonds are the topic of our next section.

Mortgage-Backed and Asset-backed Bonds

Mortgage-backed bonds are debt issues secured by a pool of home mortgages, issued primarily by the government-sponsored entities we just introduced. They are a type of agency bond that pools together home mortgages and repackages them into bond issues that are then sold to bond investors. The original goal was to increase the availability of home mortgages as a way to encourage and promote more home ownership. They have been very successful and now are responsible for 70% of home loan funding in the United States. The various flavors of mortgage-backed bonds go by various names including Pass-through Securities, Participation Certificates, Collateralized Mortgage Obligations (CMOs), Collateralized Debt Obligations (CDOs), and Mortgage-Backed Securities. Unlike most other bonds, the payments a bond investor receives consist of both interest and principal, similar to home mortgages.

The three main agencies are the Government National Mortgage Association (“Ginnie Mae”), the Federal Home Loan Mortgage Corporation (“Freddie Mac”), and the Federal National Mortgage Association (“Fannie Mae”). For decades, these entities were very successful and earned a healthy profit while accomplishing the admirable goal of increasing home ownership. That is, until the real estate bubble of the 2000’s came along. These entities got caught up in the fervor and contributed much to the Global Financial Crisis. So much so, that, as mentioned, the United States Treasury had to step in and rescue Fannie and Freddie. So now, Dear Reader, as a citizen and taxpayer of the United States of America, you are proud co-owners of Fannie and Freddie. Maybe surprisingly or maybe not surprisingly, they have rewarded you well. Every quarter, Fannie and Freddie pay several billion dollars to the Treasury from their earnings. Not bad for a country that decries socialism and wants the government to have no part of any business! Everyone can agree that the current situation is not ideal. However, no one can seem to agree on how the government should extricate itself from the industry. Stay tuned for continuing developments!

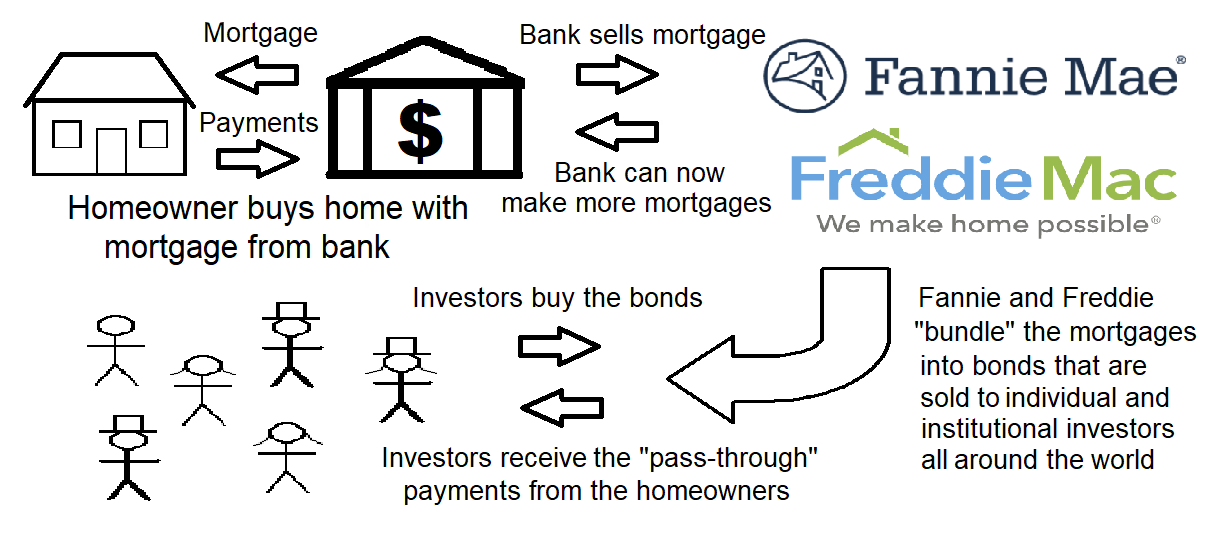

Before the advent of government-sponsored entities such as Fannie and Freddie, a potential homeowner went to their bank, credit union, savings and loan, or other type of mortgage company and applied for the mortgage. The financial institution lent the home buyer the mortgage so they could buy the house and make it their home. Every month, the homeowner made their monthly payment consisting of interest and principal to the bank, credit union, or savings and loan and the interest was credited to the financial institution as part of their earnings. Life was simple.

Life ain't so simply anymore.

Now let’s see if we can follow the money once Fannie and Freddie come onto the scene. Life became far more complicated. As before, our potential home buyers still go to a financial institution for their mortgage. Except this time, the financial institution has no intention of keeping the loan in their portfolio. They immediately sell the loan to Fannie or Freddie. Why? They receive an infusion of cash that they can use to sell another mortgage to the next wave of home buyers, generating more new mortgage-related fees and more earnings. Plus they no longer have to worry about the homeowner going bankrupt. It’s not their loan anymore. They typically will continue to service the loan which means they are accepting the monthly mortgage payments and simply forwarding the money to Fannie or Freddie.

Now here is where it gets confusing. Fannie and Freddie bundle the mortgage into packages of thousands of home loans. They then create bond issues based on the mortgages. These bonds are then sold to investors, mostly institutional investors such as life insurance companies, pension funds, and mutual funds. The investors receive the “pass-through” payments from the homeowners. As mentioned, this system was very successful for decades until the real estate bubble of the 2000’s. That’s when it was learned that many of the mortgages were sold to home buyers who did not have the necessary resources to make the payments over the long term. Many of the mortgages were so-called “no doc loans,” also known as “liar loans.” Many started with very low payments that quickly increased to the point where they could no longer make the payments. The ensuing crisis almost brought us a second Great Depression. Although there is still much controversy over the handling of the crisis, the consensus is that those in charge at the Federal Reserve Bank and the United States Treasury somehow managed to avoid the worst of a depression and instead, we suffered through the Great Recession. History is still being written about this sad chapter in our financial history.

The process of transforming lending vehicles such as mortgages into marketable securities is called securitization. The issuer pools various income producing instruments together and packages them for investors. This process can be done with almost any debt or asset. The success of the securitization of mortgage-backed bonds spread into many other areas and led to the development of asset-backed securities. Asset-backed securities go by various names such as Collateralized Bond Obligations (CBOs) and Structured Investment Vehicles (SIVs).

Asset-backed bonds are securities that are similar to mortgage-backed bonds except they are backed by a pool of bank loans, leases, and other assets such as car loans, credit card loans, patents, stocks and bonds, and even pop artists. In the late 1990’s, the artist David Bowie shocked the financial world when he issued “Bowie Bonds.” These were bonds backed by Mr. Bowie’s artistic endeavors such as his upcoming concerts and previous album releases. Although many in the industry were skeptical, the Bowie Bonds survived a credit downgrade and all the interest and principal payments were made in full. Other artists soon followed suit. Who said bonds were boring?

Municipal Bonds

Municipal bonds, often called muni bonds or just “muni’s,” are debt securities issued by states, counties, cities, and other political and governmental entities such as school districts, water or bridge authorities, or hospitals. The most attractive feature of municipal bonds is the interest paid is free of Federal taxes. Note that the IRS wants us to call them tax-exempt; they don’t appreciate the term tax-free. Also note that any capital gains from the sale of a municipal bond are not tax-exempt. Municipal bonds are very popular with individual investors, especially high income and high net worth taxpayers in the upper tax brackets. These investors must take care when they purchase municipal bonds, though, as some municipal bonds do not keep their tax-exempt status if the investor is subject to the Alternative Minimum Tax (AMT). Some municipal bonds are insured which is a desirable feature.

There are three major types of Municipal Bonds. General Obligation Bonds, also known as GOs, are municipal bonds that are backed by the full faith, credit, and taxing power of the issuer. This means that in case the entity runs into financial trouble, the entity will be required to raise revenues in any manner they can to pay the interest and principal, including raising taxes. Some time ago, the City of San Diego, California, was finally coming to terms with a pension plan that was overly generous. This led none other than The New York Times to christen San Diego, “Enron by the Sea.” (Just for the record, the overly generous plan was offered to the city employees by Republicans in the City Council in exchange for their support of a pet project on behalf of the mayor. All those leaders were long gone by the time the organic matter hit the ventilating device.) The new leaders who were left holding the bag demanded concessions from the city employees and publicly threatened that San Diego would declare bankruptcy if the employees did not agree to the concessions. This was pure bluster. If San Diego had gone to the courts claiming bankruptcy, the courts would have noted that unlike many other cities, San Diego still had plenty of untapped tax revenue streams that they could employ. Suffice it to say, the city never came hat in hand to the courts asking to be placed in bankruptcy.

The second type of municipal bonds are Revenue Bonds. Revenue Bonds are municipal bonds that require payment of principal and interest only if sufficient revenue is generated by the issuer. They are generally considered less desirable than GO bonds since GOs must seek new sources of income to meet the interest and principal payments while Revenue Bonds do not. However, Revenue Bonds typically come with higher interest rates than GOs. When researching potential Revenue Bonds, an investor should investigate the projects behind the bonds in much the same manner as when an investor researches a stock. Is the project fiscally sound? Is it desirable? Will it be able to pay the future interest and principal payments?

The last major type of municipal bonds are Special Tax Bonds. Special Tax Bonds are payable from the proceeds of a special tax that is typically voted on by the citizens of the jurisdiction. As mentioned, the college where I teach, Southwestern College, issued bonds to upgrade the buildings and other facilities of our campuses. The college asked the voters to approve bond propositions via local elections. We are happy and grateful to report that the voters approved both our bond propositions. With the proceeds from the sale of the bonds, we have been replacing older builders with new ones. The money to pay the interest and principal on the bonds will come from a special tax that is levied on property owners in the district. Although many in our community have pointed with pride to our new stadium, Southwestern recently has earned Onion Awards for architectural cluelessness. Oh, well. Everything changes; some things mutate.

As mentioned, municipal bonds offer investors attractive tax advantages, especially higher income investors. They are typically free from Federal income taxes. If the bonds are purchased by investors in that municipality, they are also often free from state and local taxes. This is sometimes referred to as double-tax exempt or double-tax free interest. If an investor is based in California and purchases California municipal bonds, they will not pay any Federal income tax nor will they pay any California income tax on the interest from the California municipal bonds. Recall that the interest payments on some bonds are subject to taxes if the investor is subject to the Alternative Minimum Tax. Also recall that any capital gains taxes on the sale of municipal bonds are not tax-exempt.

Because of this tax-exempt feature, when we research municipal bonds, we must always look at the Taxable Equivalent Yield. This allows us to compare municipal bonds with corporate and Treasury bonds. There is a Taxable Equivalent Yield calculation for Federal tax-exempt municipal bonds and a Double-Tax Exempt Taxable Equivalent Yield for both Federal & state tax-exempt municipal bonds. We will learn how to calculate these in the next chapter. We will find that the higher the tax bracket of the investor, the higher the taxable equivalent yield. For this reason, we find that municipal bonds are favored by high-income investors and eschewed by lower-income investors for the mere fact that they are just more valuable for high-income investors who then bid the prices up relative to other bonds.

Corporate Bonds

There are two major types of corporate bonds, secured and unsecured. Secured corporate bonds are backed by a claim on specific property of the issuing corporation, such as real estate, airplanes, or railroad equipment. The secured bonds are then delineated as either senior bonds, also known as senior lien bonds, or junior bonds, also known as junior lien bonds. The senior bonds have priority over the junior bonds and would be satisfied first in case of any bankruptcy proceedings. This relationship is similar to the first mortgage and a subsequent home equity line of credit (HELOC) that are associated with a house. In the event of a foreclosure, the first mortgage must be paid first before the HELOC would receive any funds.

Unsecured corporate bonds are called debentures. They are backed by the “full faith and credit” of the corporation. These are similar to a credit card loan where there is no identified collateral for the credit card company to attach for payment. The credit card company must go after whatever income or assets that the credit card holder may have. Likewise, unsecured corporate bond investors must seek payment from whatever assets are available when a company goes through bankruptcy. Similar to the pecking order described above with secured corporate bonds, there are subordinated debentures which are only able to seek payment after the debentures are satisfied. Finally, corporations can issue income bonds which are unsecured bonds that require that interest be paid only after a certain amount of income is earned.

Junk Bonds

The riskiest bonds are typically referred to as junk bonds. This is not the most flattering of titles but it is the most commonly used when referring to bonds that are in distress. More gentle names include high-yield bonds, non-investment grade bonds, distressed bonds, and speculative bonds. Junk bonds are high-risk securities that have low ratings but can produce high yields. Traditionally, junk bonds were held in very low esteem and often compared to penny stocks. They were investments to be avoided. Junk bonds were not to be discussed in polite company.

This changed in the 1980’s. Junk bonds became an industry as companies not large enough to issue bonds began to issue bonds with very high interest rates. One individual, Michael Milken, of the firm Drexel Burnham Lambert, was generally regarded as creating this industry. Sadly, Mr. Milken became involved with a trader by the name of Ivan Boesky and the two set upon a scheme to use insider information to become filthy rich. (Recall: The legal term for insider information is non-public material information.) The two inspired the movie Wall Street. The famous speech from the movie where the character brazenly declares that, “Greed is good,” is based on a speech that Mr. Boesky gave at a graduation ceremony. Both gentlemen spent time in prison, paid large fines, and were barred from the securities industry for life.

Before Mr. Milken and Drexel Burnham Lambert, junk bonds were only associated with corporations that were in dire distress. Occasionally, the bonds of a municipality qualify as junk but this is the exception, not the norm. As we have learned, the eternal struggle between risk and return applies to all investments, including bonds. With junk bonds, there is tremendous risk but they also often offer the opportunity for large capital gains along with the high income.

Unlike other bonds, junk bonds tend to follow the stock market. We say they are highly correlated with stocks. (We will discuss correlation later on in our journey together.) Why is this? Recall that most junk bonds are corporate bonds. When the stock market is doing well, it is usually a sign that the economy is prospering. Hence, corporate earnings are strong and the companies associated with the junk bonds can more readily make their interest and principal payments. When the economy is in recession, corporate earnings are depressed. Hence, not only is the stock market typically suffering but so are junk bonds because the corporations associated with the junk bonds are having a difficult time making their necessary interest and principal payments because of the depressed earnings. In contrast, in a recession, interest rates typically go down and we learned in our previous section that when interest rates go down, bond prices go up.

Zero-Coupon Bonds

We now turn our attention to a type of bond that is a bit of an oddity in the bond world, zero-coupon bonds. Zero-coupon bonds, also known as “zeros,” do not offer semi-annual interest payments. Recall that many years ago, bonds had coupons attached to them and the investor would clip the coupon, send it to the bond issuer, and the bond issuer would send them a check for the interest. Hence, a bond that pays no interest has zero coupons to clip and send. Zero-coupon bonds are sold at a deep discount from par value, similar to the savings bonds we saw in our first chapter. Instead of receiving the interest in cash, the bonds simply accrue in value until maturity. (Accrue is the fancy accounting word for increase.) For example, a $1,000 bond maturing in 20 years at 6.25% would cost $300 when it is issued. After 10 years, it would be worth $550. After 20 years, the investor would receive the full $1,000 par value.

Zero-coupon bonds are popular with those who do not need the interest income and are more interested in growing their wealth. There are a couple of disadvantages, though. They are very sensitive to interest rate changes exhibiting wide price swings. However, if you don’t plan on selling your zero-coupon bonds before maturity, then this is not an issue that concerns you. The second disadvantage is that the IRS expects you to pay taxes on the accrued interest even though you didn’t receive it in cash. There’s that phantom income problem again! To circumvent this, investors will utilize municipal zero-coupon bonds since the interest is tax-exempt or the zero-coupon bonds will be purchased inside a tax-qualified account such as an IRA or other retirement plan.

Foreign Bonds

With all due respect to the beloved memory of Jack Bogle, founder of the Vanguard Group, who stubbornly advocated investing only in the United States, our country is not the only country in the world that offers bonds. However, for many years, Mr. Bogle’s advice was worth considering with regard to bonds. Traditionally, investing in foreign bonds was not easy for retail investors. Thankfully, the wide availability of international brokerage accounts has made investing in foreign bonds easier. Also, traditionally, most other countries had much less stringent regulations and standards than the United States but that has changed dramatically for many countries. Some countries now have stricter regulations and standards. However, there are still serious considerations a potential investor must take into account when considering purchasing foreign bonds.

Along with all the normal risks associated with bonds, foreign bonds carry currency risk. When a bond is purchased abroad, interest and principal payments are paid in foreign currencies. All other things being equal (and they never are), if the U.S. dollar rises relative to the foreign currency, the value of the bond will fall. Contrariwise, if the U.S. dollar falls relative to the foreign currency, the value of the bond will rise. It is an inverse relationship. Again, think of the see-saw analogy.

To counter the currency risk and attract investors from the United States, in the past, many foreign entities issued dollar-denominated bonds. The foreign bond issuer promised to pay the interest and principal payments in dollars, no matter what happened to the currency exchange rate. This removed the currency risk from the investor. However, some jurisdictions saw their currency fall precipitously against the dollar. This meant that the foreign bond issuers saw their payment double, triple, or more since they needed far more of their own currency to pay the dollar interest and principal obligations. Needless to say, some of the entities defaulted.

Ultimately, for the vast majority of retail investors, global and international bond mutual funds are the preferred choice for those interested in foreign bonds. Established and successful mutual fund companies have the resources to conduct the international transactions and more importantly, have the global research teams necessary to properly assess the risks and rewards of bonds based outside the United States.