1.3: An Overview of the Investment Universe

- Page ID

- 79464

Let’s become casually acquainted with the major investment asset classes. We will dispense with all the tedious details. Concern yourself with just what we cover here. Don’t fret. There will be plenty of time later on to learn the many intricacies of these investments. As we introduce each investment asset class, we will also touch on the risk and return that we can expect from each.

Equity Securities, Also Known as Common Stocks or Stocks

In the investment world, equity refers to ownership. Equity securities, also known as common stocks, represent partial ownership in corporations. Most people just use the term stocks. The term stocks is a bit unfortunate. Your Humble Author prefers to refer to them as companies or better yet, businesses. You are investing in a business. Why invest in a business? When all goes well, businesses grow and earn money. This creates two great opportunities for investors. When the business grows, your partial ownership of the business should also grow. That’s capital appreciation, also known as capital gains. Also, the business can optionally distribute earnings to you in the form of dividends. (You can think of dividends like interest payments even though they are legally two different forms of payments.) We invest in businesses for potential capital appreciation and potential dividends. We invest for growth and income.

Note that we said, “When all goes well.” Obviously, all doesn’t always go well in this wicked world of ours, does it? Both capital appreciation and dividends are optional and are not guaranteed. Therefore, we find that stocks are high-risk investments. We say that stocks are volatile. Stocks exhibit high volatility. Volatility is a euphemism for, “I lost a whole lotta’ money!” You might ask someone how that stock he or she bought is doing and they may sheepishly say, “Oh, it’s been volatile.” That means they bought it for $11.88 and sold it for 30¢. Do you know anyone who bought a stock for $11.88 and sold it for 30¢? I do. I have known him all my life. He’s kind of a goofy guy who teaches Introduction to Investments at Southwestern Community College in Chula Vista … Look, it was a really good company and they were going to strike it rich by making artificial blood and there would be no more need for blood banks or calls to the public to donate blood and well, um, it just didn’t turn out the way it was supposed to. Ahem. Stocks are volatile. Stocks are risky. In fact, to paraphrase Professor Burton Malkiel from his famous book, A Random Walk Down Wall Street discussed in our Bibliography, the 2008 definition of stocks is, “Stocks are equity investment instruments designed to lose value.”

However, if we can learn to stomach the volatility that comes along with stock investing, history tells us that we can reasonably expect to receive some of the best long-term returns available from the investment world. We like to say that stocks have an average annual return of 8%, 9%, or even 10% over the long term. The problem is that they almost never return 8% or 9% or 10% in any given year. The returns vary substantially, up and down. For this reason, when we want to invest in stocks, we must think long term. We must give our stock investment enough time to reward us with 8% or 9% or 10% annually. As Warren Buffett is quoted as saying, “If you aren’t thinking about owning a stock for ten years, don’t even think about owning it for ten minutes.” Stocks are long-term investments.

Disclaimers: The real estate fans are most likely jumping up and down and screaming that real estate has given investors better returns than stocks. Calm down and please accept my apologies. In one sense, they are correct. In another, they are not. The problem is how we measure investment returns and how different investments are typically purchased. We will deal with this thorny issue later on. Some stock fans might also be screaming saying that 8%, 9%, 10% is too low. Stocks have done better. This is actually true. Stocks as a whole have done better than 10% over the last 100 years and some stocks have done a whole lot better. However, some have done a whole lot worse. We prefer to keep new investors’ expectations muted, especially since there are long periods of time where stocks have done a whole lot worse than 8%, 9%, or 10%. Finally, a scant few stocks can be considered moderate risk and moderate return vehicles. In the presentation for the previous section ‒ You have watched it already, right? ‒ we discussed Nestlé, the world’s largest food company. Companies such as Nestlé can be categorized as moderate risk and moderate return investments.

Fixed-Income Securities, Also Known as Bonds

Fixed-income securities are typically referred to as bonds. Bonds are long-term loans to corporations, state and local municipalities, and the Federal government. When you invest in a bond, you get to play the part of a bank. You lend your money to one of these entities. In return, they promise to repay the principal ‒ the money you lent them ‒ and along the way, they will pay you interest. Most people pay their debts to the banks. Likewise, most corporations and state and local governments also pay their debts. The United States Treasury has always paid its debts. Hence, we find that bonds are far less risky than stocks. And subsequently, we find the long term return from bonds is far less than stocks. (Are you starting to see a pattern here, Dear Students?) What can we expect from bonds? Investors used to be accustomed to receiving 3% to 8% in interest from their bond investments. During the years after the Global Financial crisis, many bonds paid 1% to 3%. Greater than 4% is unusual. In 2022, interest rates rose and investors could again find attractive interest rates from many bonds.

Remember that bonds are securities and bond prices change in the marketplace every day just like stocks. At first, it may seem a bit odd that the value of a loan could vary. Yet there are times when the prices of bonds can fall, too. However, as mentioned though, the volatility with regard to bonds is much less than what stocks exhibit. To repeat, the fall will typically be far less than stocks but it can still sting. For example, when some stocks lost well over 50% during the Global Financial Crisis of the late 2000’s, many bonds lost between 10% and 20%. A similar decline in bonds was experienced in 2022. We again paraphrase Professor Malkiel by saying the 2008 definition of bonds is, “Bonds are fixed-rate investment instruments designed to lose value.”

Short-term Investments, Also Known as “Cash” ‒ A Place to Park Your Money

Short-term investments are often referred to as “cash.” We usually see cash put in quotes because these investments are not dollar bills that we stuff under our mattresses. Many of these short-term instruments are tradable securities so again, their prices do change. However, they are vehicles that are typically guaranteed by some governmental organization. And if they are not guaranteed, they are pretty darned close. If you have been paying attention, you should be able to guess correctly that since these choices have very low risk, these investments will not give us much reward. Therefore, we say that short-term investments are a place to park your money. You aren’t going to lose your money, but you also aren’t going to make much money. That is why we call them short-term investments. If we need the money in the short-term, we don’t want to place our funds into the stock market. Even the bond market might be too risky for us. We need to park our money into a short-term investment so that in three, six, or nine months, we know it will not have lost 10%, 20%, or more of its value. At the end of this introductory chapter, we will cover short-term investments in detail. Our 2008 Definition? “Short-term investments are instruments designed to accept what remains of investors’ money after they have given up on stocks and bonds.”

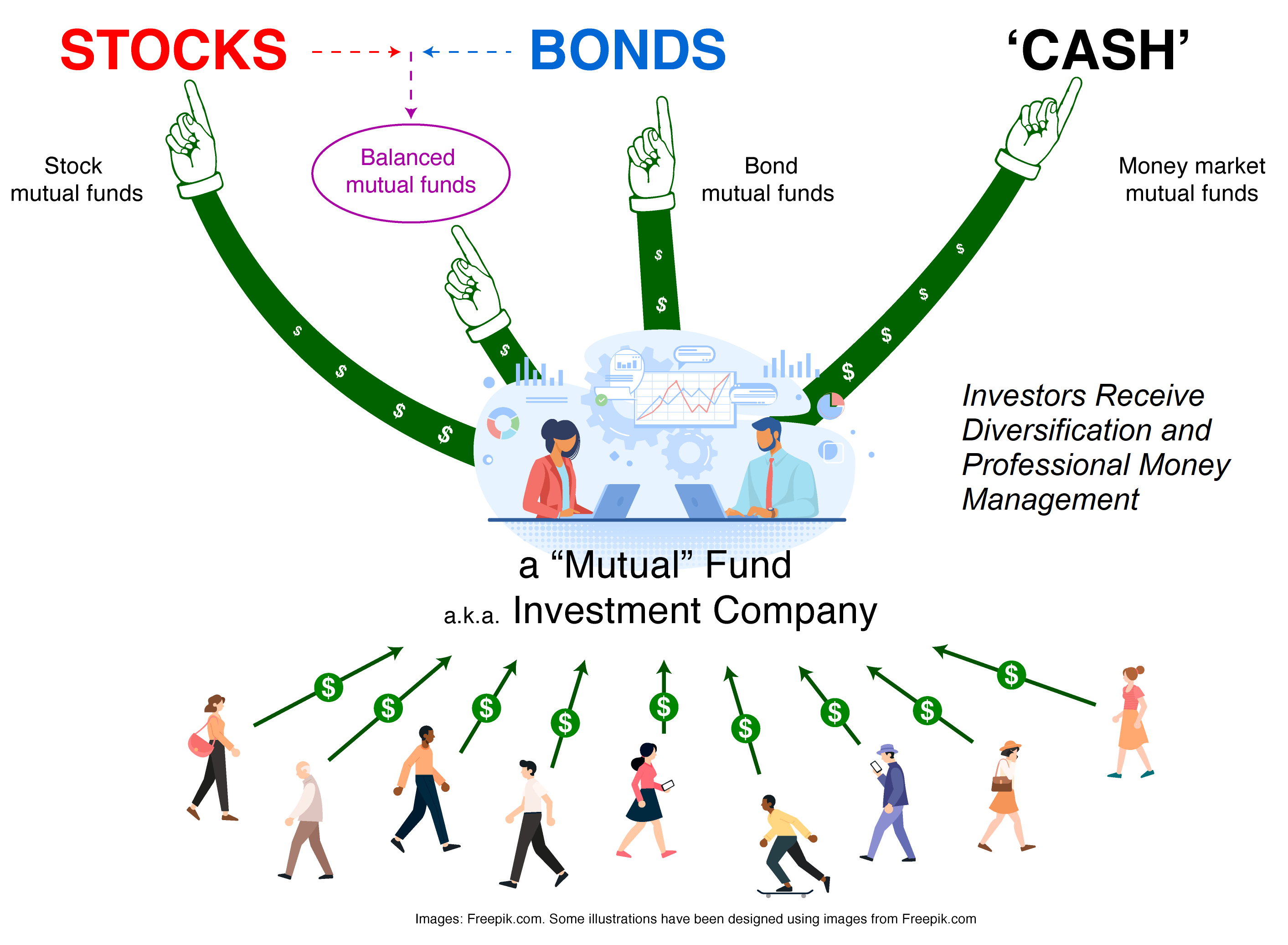

Mutual Funds, Also Known as Investment Companies ‒ Investments for the Masses

Unless you live on a deserted island or somehow effectively have shut out all forms of mass media, you no doubt have been subjected to advertisements for mutual funds. There is a valid reason for this. Mutual funds are investments for the masses. Just as most of us workaday individuals don’t build our own cars, make our own shoes, or grow our own food, most people will not dedicate the time to learn how to invest. (This is most unfortunate. Everyone should take Introduction to Investments, not that I’m biased, of course.) And education is just the beginning! They then need to spend many hours doing the necessary research to identify, choose, and monitor their individual stock and bond investments. You, Dear Readers, are going to make this a fun and profitable labor of love. Many other people are either not interested, too nervous or frightened, or just simply too busy living their lives. This is where mutual funds come into the picture.

The legal term for a mutual fund is an investment company. Now doesn’t that name make more sense? The term investment company tells you what the mutual fund does for you. Do you need a car? You go to a car company. You need shoes? You go to a shoe company. You need investments? You go to an investment company! Mutual funds / investment companies are companies that pool investors’ money and invest in a diversified portfolio of securities, typically stocks, bonds, or a combination of stocks and bonds. Investors receive two valuable benefits, diversification and professional money management. Because of the size of the typical mutual fund, they are not limited to 10 or 20 stocks or bonds as is common with an individual investor. More than 20 stocks and an individual investor often becomes overwhelmed with the necessary research to simply keep track of their holdings. A typical mutual fund will hold 100 or 200 securities. Some hold many more.

So how does the mutual fund keep from becoming overwhelmed? The mutual fund is managed by professional money managers, the second major benefit of investing in mutual funds. The mutual fund portfolio managers are highly skilled and very well-paid professionals whose day-to-day job is to identify, choose, and then monitor the diversified portfolio of investments in the mutual fund. As we shall see, it is not an easy job and there is some controversy over whether these individuals are actually worth the high salaries they demand. We will explore this debate in our chapter dedicated to mutual funds.

Because of these two valuable benefits ‒ diversification and professional money management ‒ mutual funds have become extremely popular. Adding to their popularity are the countless employer-sponsored retirement programs such as 401(k) and 403(b) plans. Mutual funds are the dominant investment choice for employer-sponsored retirement programs. Almost half of all American households own mutual funds. In our next chapter, because of their importance as investments for the masses, we will spend a great deal of time on mutual funds.

Mutual Funds: Investments for the Masses, Graphics courtesy of Ferran Capo: StudioCapo

What kinds of risks and returns can we expect from mutual funds? Mutual funds will exhibit risks and returns similar to their underlying investments. There are many mutual funds that fall into the short-term investment category. These are called money market funds. Low risk, low return. However, most mutual funds are dedicated to stocks or bonds or both and they will exhibit the same risk versus return characteristics of stocks and bonds. Hence, what is their 2008 definition? “Yeah, them too.” 2008 was a very difficult year for everyone.

Hybrid Securities – Preferred Stocks and Convertible Securities

Hybrid securities are designed to offer the stability of fixed-income investments (bonds) with the opportunity for capital growth of equity investments (stocks). With these investments, we are trying to get the best of both worlds. The pesky fly in the ointment with this approach is that along with the advantages of both stocks and bonds, you also get the disadvantages of both stocks and bonds. So, we get the best of both worlds … and we get the worst of both worlds.

Other annoying flies buzzing around the hybrid security worlds are the names of the major types of hybrid securities. The two major examples of hybrid investments are preferred stock and convertible securities. Don’t they sound enticing? Wouldn’t you really rather have “preferred stock” instead of just “common stock?” Well, actually, no, you and I and most individual investors don’t really want preferred stock. They are typically owned by corporations. Plus anything that has to do with convertibles must be cool, right? You know, driving down the highway in your convertible car with the wind blowing through your hair? Well, convertible securities are nowhere near as sexy as that, as we shall see. For now, all you need to know is that hybrid securities are an attempt to combine the advantages of stocks and bonds together but they also combine the disadvantages of stocks and bonds. We will postpone discussing these oddities until much later in our class. Finally, they constitute a very small part of the investment universe.

Other Investment Alternatives – Real Estate, Physical Assets

Not everyone wants to invest in just stocks or bonds or mutual funds. For them, they may want to dabble in the world of real estate or try their hand at precious metals, art, collectibles, cars, or even enter the high-stakes world of commodities. Suffice to say, these investments are not for everyone. For many people, just scraping together the resources to purchase a home is enough real estate for a lifetime. Also, as we will see, some alternatives such as gold that get a great deal of attention have not necessarily been very good investments over the long term. At the very end of our journey together, we will touch on these alternatives. By the way, none of these choices were spared during the Global Financial Crisis in 2008.

Derivatives – Options Contracts, Futures Contracts

Derivative assets are speculative securities that derive their value from an underlying security or asset such as a stock or bond. “What? You are not buying the stock or bond?” No, you are buying a security that depends upon the price movements of a stock or bond. That sounds very confusing. Well, yes, it is. Derivatives are very confusing. More importantly, they are immensely risky. You can make 100% in one day … and then lose it all the next day. For this reason, we do not categorize them as investments. They are speculations. (Throughout the class, when you see the words speculative or speculation, simply substitute the word gambling, okay?)

Two major examples of derivatives are options and futures. Actually, to show you how confusing these things really are, their actual names are options contracts and futures contracts. Try saying those names three times fast. For now, this is all you need to know about derivatives: Derivatives derive their value from another asset, two major examples of derivatives are options and futures, and derivatives are extremely dangerous. In 2008, the derivative speculators did not feel so all alone. Usually, they are the only ones who are proud to have only lost 30%.

We have completed our Overview of the Investment Universe. Once again, we remind you that, for now, the material in this chapter is all you need to study and learn with regard to the investment alternatives discussed above. As you may have gathered by now, in this class, we will emphasize stocks, bonds, short-term investments, and mutual funds. For the vast majority of us retail investors, these are the most popular and most important financial investment options. It is now time for us to delve deeply into the Eternal Struggle of Investing, Risk versus Return. But before we do that, we want you to review the investment alternatives we have just covered. Please make sure you watch the presentation on the class website. There is a comprehension checking exercise at the very end of the presentation. Also, work through the Security Types Handout. Memorize this document for the first exam. (Hint, hint. Wink, wink. Nudge, nudge.)