14.10: The Battle Unfolds

- Page ID

- 4586

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Learning Objectives

After studying this section you should be able to do the following:

- Understand the challenges of maintaining growth as a business and industry mature.

- Recognize how the businesses of many firms in a variety of industries are beginning to converge.

- Critically evaluate the risks and challenges of businesses that Google, Microsoft, and other firms are entering.

- Appreciate the magnitude of this impending competition, and recognize the competitive forces that will help distinguish winners from losers.

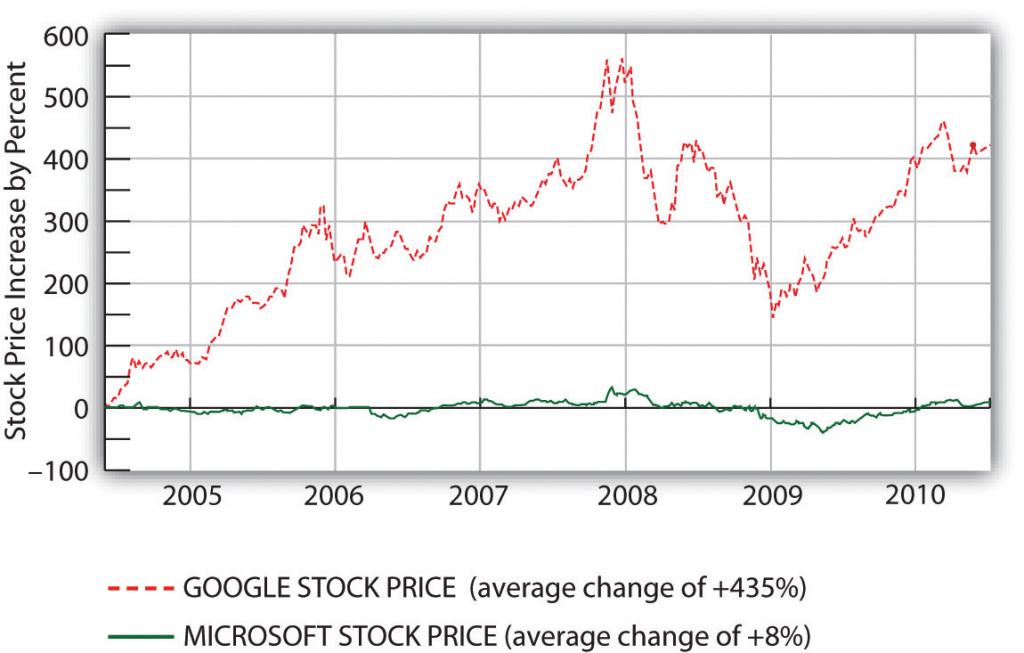

Google has been growing like gangbusters, but the firm’s twin engines of revenue growth—ads served on search and through its ad networks—will inevitably mature. And it will likely be difficult for Google to find new growth markets that are as lucrative as these. Emerging advertising outlets such as social networks and mobile have lower click-through rates than conventional advertising, suggesting that Google will have to work harder for less money.

For a look at what can happen when maturity hits, check out Microsoft. The House that Gates Built is more profitable than Google, and continues to dominate the incredibly lucrative markets served by Windows and Office. But these markets haven’t grown much for over a decade. In industrialized nations, most Windows and Office purchases come not from growth, but when existing users upgrade or buy new machines. And without substantial year-on-year growth, the stock price doesn’t move.

Figure 14.14 A Comparison of Roughly Five Years of Stock Price Change—Google (GOOG) versus Microsoft (MSFT)

For big firms like Microsoft and Google, pushing stock price north requires not just new markets, but billion-dollar ones. Adding even $100 million in new revenues doesn’t do much for firms bringing in $24 billion and $58 billion a year, respectively. That’s why you see Microsoft swinging for the fences, investing in the uncertain, but potentially gargantuan markets of video games, mobile phone software, cloud computing (see Chapter 10 “Software in Flux: Partly Cloudy and Sometimes Free”), music and video, and of course, search and everything else that fuels online ad revenue.

Search: Google Rules, but It Ain’t Over

PageRank is by no means the last word in search, and offerings from Google and its rivals continue to evolve. Google supplements PageRank results with news, photos, video, and other categorizations (click the “Show options…” link above your next Google search). Yahoo! is continually refining its search algorithms and presentation (click the little “down” arrow at the top of the firm’s search results for additional categorizations and suggestions). And Microsoft’s third entry into the search market, the “decision engine” Bing, sports nifty tweaks for specific kinds of queries. Restaurant searches in Bing are bundled with ratings stars, product searches show up with reviews and price comparisons, and airline flight searches not only list flight schedules and fares, but also a projection on whether those fares are likely go up or down. Bing also comes with a one-hundred-million-dollar marketing budget, showing that Microsoft is serious about moving its search market share out of the single digits. And in the weeks following Bing’s mid-2009 introduction, the search engine did deliver Microsoft’s first substantive search engine market share gain in years.

New tools like the Wolfram Alpha “knowledge engine” (and to a lesser extent, Google’s experimental Google Squared service) move beyond Web page rankings and instead aggregate data for comparison, formatting findings in tables and graphs. Web sites are also starting to wrap data in invisible tags that can be recognized by search engines, analysis tools, and other services. If a search engine can tell that a number on a restaurant’s Web site is, for example, either a street address, an average entrée price, or the seating capacity, it will be much easier for computer programs to accurately categorize, compare, and present this information. This is what geeks are talking about when they refer to the semantic Web. All signs point to more innovation, more competition, and an increasingly more useful Internet!

Both Google and Microsoft are on a collision course. But there’s also an impressive roster of additional firms circling this space, each with the potential to be competitors, collaborators, merger partners, or all of the above. While wounded and shrinking, Yahoo! is still a powerhouse, ranking ahead of Google in some overall traffic statistics. Google’s competition with Apple in the mobile phone business prompted Google CEO Eric Schmidt to resign from Apple’s board of directors. Meanwhile, Google’s three-quarters-of-a-billion-dollar purchase of the leading mobile advertiser AdMob was quickly followed by Apple snapping up number two mobile ad firm Quattro Wireless for $275 million. Add in eBay, Facebook, Twitter, Amazon, Salesforce.com, Netflix, the video game industry, telecom and mobile carriers, cable firms, and the major media companies, and the next few years have the makings of a big, brutal fight.

Strategic Issues

Google’s scale advantages in search and its network effects advantages in advertising were outlined earlier. The firm also leads in search/ad experience and expertise and continues to offer a network reach that’s unmatched. But the strength of Google’s other competitive resources is less clear.

Within Google’s ad network, there are switching costs for advertisers and for content providers. Google partners have set up accounts and are familiar with the firm’s tools and analytics. Content providers would also need to modify Web sites to replace AdSense or DoubleClick ads with rivals. But choosing Google doesn’t cut out the competition. Many advertisers and content providers participate in multiple ad networks, making it easier to shift business from one firm to another. That likely means that Google will have to retain its partners by offering superior value.

Another vulnerability may exist with search consumers. While Google’s brand is strong, switching costs for search users are incredibly low. Move from Google.com to Bing.com and you actually save two letters of typing!

Still, there are no signs that Google’s search leadership is in jeopardy. So far users have been creatures of habit, returning to Google despite heavy marketing by rivals. And in Google’s first decade, no rival has offered technology compelling enough to woo away the googling masses—the firm’s share has only increased. Defeating Google with some sort of technical advantage will be difficult, since Web-based innovation can often be quickly imitated. Google now rolls out over 550 tweaks to its search algorithm annually, with many features mimicking or outdoing innovations from rivals (Levy, 2010).

The Google Toolbar helps reinforce search habits among those who have it installed, and Google has paid the Mozilla foundation (the folks behind the Firefox browser) upwards of $66 million a year to serve as its default search option for the open source browser (Shankland, 2008). But Google’s track record in expanding reach through distribution deals is mixed. The firm spent nearly $1 billion to have MySpace run AdSense ads, but Google has publicly stated that social network advertising has not been as lucrative as it had hoped (see Chapter 8 “Facebook: Building a Business from the Social Graph”). The firm has also spent nearly $1 billion to have Dell preinstall its computers with the Google browser toolbar and Google desktop search products. But in 2009, Microsoft inked deals that displaced Google on Dell machines, and it also edged Google out in a five-year search contract with Verizon Wireless (Wingfield, 2009).

How Big Is Too Big?

Microsoft could benefit from embedding its Bing search engine into its most popular products (imagine putting Bing in the right-mouseclick menu alongside cut, copy, and paste). But with Internet Explorer market share above 65 percent, Office above 80 percent, and Windows at roughly 90 percent1 (Montalbano, 2009), this seems unlikely.

European antitrust officials have already taken action against Redmond’s bundling Windows Media Player and Internet Explorer with Windows. Add in a less favorable antitrust climate in the United States, and tying any of these products to Bing is almost certainly out of bounds. What’s not clear is whether regulators would allow Bing to be bundled with less dominant Microsoft offerings, such as mobile phone software, Xbox, and MSN.

But increasingly, Google is also an antitrust target. Microsoft has itself raised antitrust concerns against Google, unsuccessfully lobbying both U.S. and European authorities to block the firm’s acquisition of DoubleClick (Broach, 2007; Kawamoto & Broach, 2007). Google was forced to abandoned a fall 2008 search advertising partnership with Yahoo! after the Justice Department indicated its intention to block the agreement (Yahoo! and Microsoft have since inked a deal to share search technology and ad sales). The Justice Department is also investigating a Google settlement with the Authors’ Guild, a deal in which critics have suggested that Google scored a near monopoly on certain book scanning, searching, and data serving rights (Wildstrom, 2009). And yet another probe is investigating whether Google colluded with Apple, Yahoo! and other firms to limit efforts to hire away top talent (Buskirk, 2009).

Of course, being big isn’t enough to violate U.S. antitrust law. Harvard Law’s Andrew Gavil says, “You’ve got to be big, and you have to be bad. You have to be both” (Lohr & Helft, 2009). This may be a difficult case to make against a firm that has a history of being a relentless supporter of open computing standards. And as mentioned earlier, there is little forcing users to stick with Google—the firm must continue to win this market on its own merits. Some suggest regulators may see Google’s search dominance as an unfair advantage in promoting its related properties such as YouTube and Google Maps over those offered by rivals (Vogelstein, 2009)—an advantage not unlike Microsoft’s use of Windows to promote Media Player and Internet Explorer. While Google may escape all of these investigations, increased antitrust scrutiny is a downside that comes along with the advantages of market-dominating scale.