2.3: The account and rules of debit and credit

- Page ID

- 19984

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)A business may engage in thousands of transactions during a year. An accountant classifies and summarizes the data in these transactions to create useful information.

Steps in recording business transactions

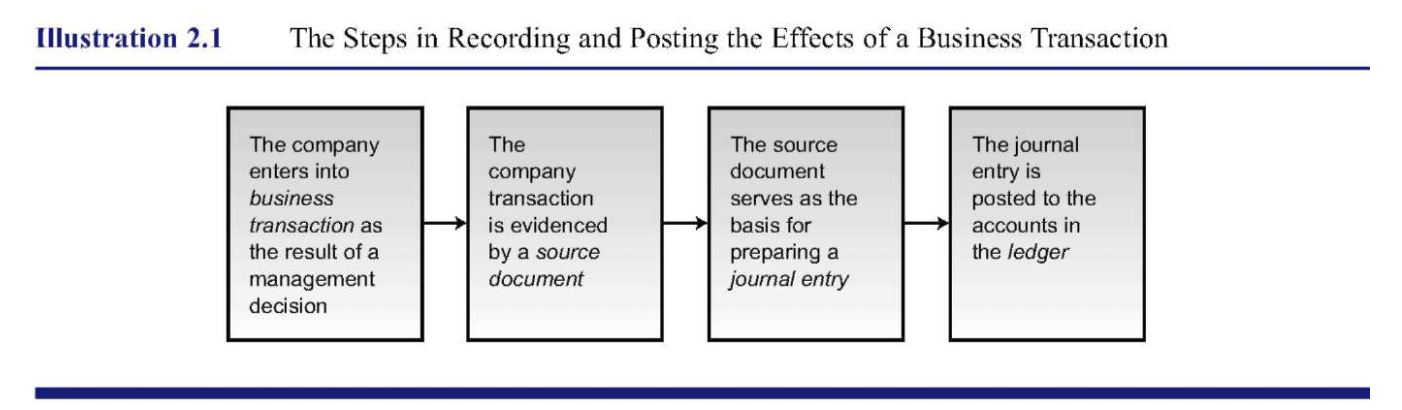

Look at Exhibit 9 to see the steps in recording and posting the effects of a business transaction. Note that source documents provide the evidence that a business transaction occurred. These source documents include such items as bills received from suppliers for goods or services received, bills sent to customers for goods sold or services performed, and cash register tapes. The information in the source document serves as the basis for preparing a journal entry. Then a firm posts (transfers) that information to accounts in the ledger.

You can see from Exhibit 9 that after you prepare the journal entry, you post it to the accounts in the ledger. However, before you can record the journal entry, you must understand the rules of debit and credit. To teach you these rules, we begin by studying the nature of an account.

Fortunately, most business transactions are repetitive. This makes the task of accountants somewhat easier because they can classify the transactions into groups having common characteristics. For example, a company may have thousands of receipts or payments of cash during a year. As a result, a part of every cash transaction can be recorded and summarized in a single place called an account.

An account is a part of the accounting system used to classify and summarize the increases, decreases, and balances of each asset, liability, stockholders' equity item, dividend, revenue, and expense. Firms set up accounts for each different business element, such as cash, accounts receivable, and accounts payable. Every business has a Cash account in its accounting system because knowledge of the amount of cash on hand is useful information.

Accountants may differ on the account title (or name) they give the same item. For example, one accountant might name an account Notes Payable and another might call it Loans Payable. Both account titles refer to the amounts borrowed by the company. The account title should be logical to help the accountant group similar transactions into the same account. Once you give an account a title, you must use that same title throughout the accounting records.

The number of accounts in a company's accounting system depends on the information needs of those interested in the business. The main requirement is that each account provides information useful in making decisions. Thus, one account may be set up for all cash rather than having a separate account for each form of cash (coins on hand, currency on hand, and deposits in banks). The amount of cash is useful information; the form of cash often is not.

To illustrate recording the increases and decreases in an account, texts use the T-account, which looks like a capital letter T. The name of the account, such as Cash, appears across the top of the T. We record increases on one side of the vertical line of the T and decreases on the other side. A T-account appears as follows:

An accounting perspective:

Bussiness insight

Have you ever considered starting your own business? If so, you will need to understand accounting to successfully run your business. To know how well your business is doing, you must understand and analyze financial statements. Accounting information also tells you why you are performing as reported. If you are in business to sell or develop a certain product or perform a specific service, you cannot operate profitably or consider expanding unless you base your business decisions on accounting information.

In Chapter 1, you saw that each business transaction affects at least two items. For example, if you—an owner—invest cash in your business, the company's assets increase and its stockholders' equity increases. This result was illustrated in the summary of transactions in Exhibit 1.3. In the following sections, we use debits and credits and the double-entry procedure to record the increases and decreases caused by business transactions.

Accountants use the term debit instead of saying, "Place an entry on the left side of the T-account". They use the term credit for "Place an entry on the right side of the T-account". Debit (abbreviated Dr.) simply means left side; credit (abbreviated Cr.) means right side.Thus, for all accounts a debit entry is an entry on the left side, while a credit entry is an entry on the right side. The abbreviations “Dr.” and “Cr.” are based on the Latin words “debere” and “credere”. A synonym for debit an account is charge an account.|

Any Account |

|

|

Left, or |

Right, or |

|

debit, side |

credit, side |

After recognizing a business event as a business transaction, we analyze it to determine its increase or decrease effects on the assets, liabilities, stockholders' equity items, dividends, revenues, or expenses of the business. Then we translate these increase or decrease effects into debits and credits.

In each business transaction we record, the total dollar amount of debits must equal the total dollar amount of credits. When we debit one account (or accounts) for USD 100, we must credit another account (or accounts) for a total of USD 100. The accounting requirement that each transaction be recorded by an entry that has equal debits and credits is called double-entry procedure, or duality. This double-entry procedure keeps the accounting equation in balance.

The dual recording process produces two sets of accounts—those with debit balances and those with credit balances. The totals of these two groups of accounts must be equal. Then, some assurance exists that the arithmetic part of the transaction recording process has been properly carried out. Now, let us actually record business transactions in T-accounts using debits and credits.