3.11: LIFO Base Illustration

- Page ID

- 88512

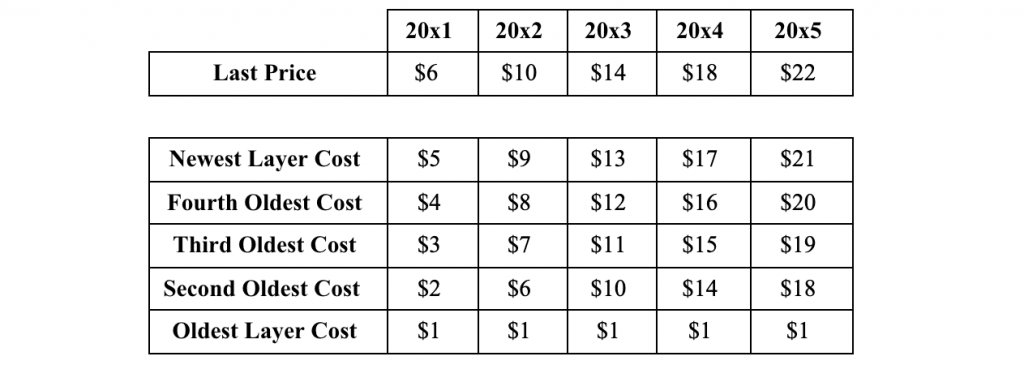

XYZ Corp. costs its inventory on a LIFO basis due to the cost and price inflation its product continuously manifests.

In the first year illustrated, “20×1,” the company purchased 5 units. It sold 4 units, leaving the oldest unit to be carried forward as the LIFO Base Inventory to the next year, “20×2.” See the table below.

Each year going forward, it continues to purchase 4 units and sell 4 units. Therefore, the LIFO Base, initially costed at $1, carries over until “20×5.” The revenue the company receives equals the average of the last price in the current and prior years. The last price in “20×0” was $2. Due to the high LIFO costing method, the gross profits remain low, thereby minimizing taxes. Had it done its inventory on a FIFO basis, its gross profits would have been slightly higher. (You can figure this out.)

In 20×5, the company sells all 5 units that were available for sale. The last unit sold was at a price of $22 and a cost, based on LIFO, of only $1. The company would therefore book a high, “windfall” profit on that unit, contrary to the intent of LIFO, which is to keep profits low.

The purpose of using LIFO Inventory Accounting is to reduce gross profits and thus taxes. We have seen that selling product from the LIFO Base will negate this objective. To avoid this problem, management should order a 6th unit in 20×5 so that the LIFO Base is not costed out. In doing so, management is “manipulating” the effect of its inventory costing method.

Remember, this is accounting fiction in the sense that the costs are unrelated to the actual age of the units. A good merchandiser would have long ago moved out any product that is subject to physical aging.