7.8: Budgeted Balance Sheet

- Page ID

- 26086

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

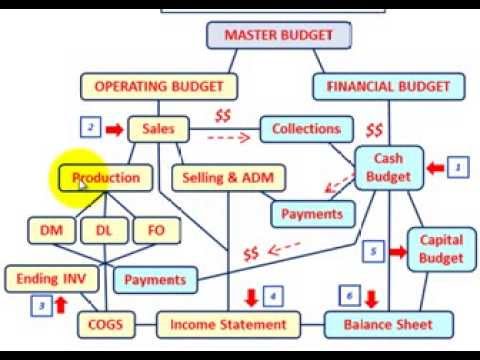

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Preparing a projected balance sheet, or financial budget, involves analyzing every balance sheet account. The beginning balance for each account is the amount on the balance sheet prepared at the end of the preceding period. Then, managers consider the effects of any planned activities on each account. Many accounts are affected by items appearing in the operating budget and by either cash inflows or outflows. Cash inflows and outflows usually appear in a cash budget discussed later in the chapter.

The complexities encountered in preparing the financial budget often require the preparation of detailed schedules. These schedules analyze such things as planned accounts receivable collections and balances, planned material purchases, planned inventories, changes in all accounts affected by operating costs, and the amount of federal income taxes payable. Dividend policy, inventory policy, financing policy and constraints, credit policy, and planned capital expenditures also affect the amounts in the financial budget. This video will give you an overview of the budgeted balance sheet process (the first 3 minutes reviews the entire master budget process).

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=162

Now that Leed’s management has prepared the operating budget (or projected income statement), it can prepare its financial budget. Remember that the financial budget is a projected balance sheet.

To prepare a projected balance sheet, Leed’s management must analyze each balance sheet account. Managers take the beginning balance from the balance sheet at the end of the preceding period (remember, ending balances of one period are the beginning balances of the next period). Look at Leed Company’s balance sheet as of December 31 last year. Management must consider the effects of planned activities on these balances. Many accounts are affected by items in the planned operating budget, by cash inflows and outflows, and by policy decisions. Management uses the planned operating budgets and cash budget to prepare the project balance sheet for this year.

| Leed Company | ||

| Balance sheet | ||

| December 31 (last year) | ||

| Assets | ||

| Current assets: | ||

| Cash | $130,000 | |

| Accounts receivable | 200,000 | |

| Inventories: | ||

| Materials | $40,000 | |

| Finished goods | 130,000 | 170,000 |

| Total current assets | $500,000 | |

| Property, plant, and equipment: | ||

| Land | $60,000 | |

| Buildings | $1,000,000 | |

| Less: accumulated depreciation | 400,000 | 600,000 |

| Factory Equipment | $600,000 | |

| Less: accumulated depreciation | 180,000 | 420,000 |

| Total property, plant, and equipment | $1,080,000 | |

| Total assets | $1,580,000 | |

| Liabilities and stockholders‘ equity | ||

| Current liabilities: | ||

| Accounts payable | $80,000 | |

| Income taxes payable | 100,000 | |

| Total current liabilities | $180,000 | |

| Stockholders’ equity: | ||

| Common stock (100,000 shares of $10 par value) | $1,000,000 | |

| Retained earnings | 400,000 | |

| Total stockholders’ equity | $1,400,000 | |

| Total liabilities and stockholders’ equity | $1,580,000 | |

We will look at each account and determine the new budgeted balances based on the previous schedules.

Cash

We can get the ending cash balance from the Ending Cash balance in the cash budget. The ending cash balance is $188,000.

Accounts Receivable

The balance in Accounts Receivable represents credit sales that have not been collected during the year. This would be 40% of Quarter 4 sales of $1,000,000 or $400,000 to be collected during the 1st quarter of the next year.

Inventory

For a manufacturer like Leed Company, there are two inventory accounts: Raw Materials inventory and Finished Goods inventory. Raw Materials inventory will come from the materials purchases budget using desired ending inventory for quarter 4 or the year x cost per material. For Leed Company, there were 30,000 lbs of materials for ending inventory x $2 per lb of material = $60,000. For Finished Goods inventory, we will use the desired ending inventory units from the production budget x production cost per unit. For Leed Company, the production cost is $20.50 per unit including direct materials, direct labor, variable and fixed overhead. The ending balance in finished goods inventory is calculate as 6,000 units x $20.50 per unit or $123,000.

For a merchandising company, you would use the quarter 4 or year Ending merchandise inventory units x the cost per unit.

Property, Plant and Equipment

This section will look at the balances from the previous year and add any depreciation and additional purchases for the year. Property, Plant and Equipment (also called Fixed Assets) refer to long term assets used in the business including land, equipment, machinery, buildings, etc. Depreciation is applied to all of these items except for land, which is not depreciated.

For Leed Company, there were no changes to the Land account so the balance will remain at $60,000. Leed purchased a new building for $650,000 in the 4th quarter so the new building balance is $1,650,000 ($1,000,000 last year + 650,000 new building). According to the selling and administration expense budget, we had depreciation on the office building of $80,000 so we will add this to the existing balance from the previous year to get a new balance of $480,000 ($400,000 prior year + $80,000 current year depreciation). We are not planning on buying any new equipment this year. The equipment balance will remain the same at $600,000. According to the manufacturing overhead budget, we planned $40,000 of factory equipment depreciation this year. The new balance for equipment accumulated depreciation is $220,000 ($180,000 prior year + $40,000 current year depreciation).

Current Liabilities

Current Liabilities are liabilities we expect to pay in the next year. Accounts Payable is determined using the purchases budget (material purchases for a manufacturer or inventory purchase budget for a merchandiser) and the schedule of cash payments.

Leed Company budgets purchase payments as 80% in the quarter of purchase and 20% in the quarter after the purchase. We can calculate Leed’s ending accounts payable by looking at the Quarter 4 material purchases of $217,500 x 20% to be paid in the first quarter of next year for $43,500.

Income taxes are typically paid in the quarter after they were calculated or during the first quarter of the next year. For Leed Company, income taxes are paid in the quarter after they were calculated. We can determine the budgeted income tax amount from the budgeted income statement. In quarter 4, Leed Company plans income taxes of $142,500 to be paid in the first quarter of the following year making this the ending balance for Income Taxes Payable.

Stockholder’s Equity

Stockholder’s Equity is comprised of common stock and retained earnings. Common stock represents ownership in the company. Retained Earnings is the earnings of the company over time minus any dividends paid.

Leed Company did not have any new issues of common stock so the ending common stock balance will remain the same as $1,000,000. For retained earnings, we will need to calculate the ending balance using the following formula:

Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings

Beginning retained earnings comes from the balance of last year’s balance sheet of $400,000. Net Income comes from the budgeted income statement for the year of $855,000. Dividends can be determined from the schedule of cash payments which shows $120,000 paid this year. Ending Retained Earnings is $1,135,000 ($400,000 + 855,000 – 120,000).

The full budgeted balance sheet will look like this:

| Leed Company | ||

| Budgeted Balance sheet | ||

| December 31 | ||

| Assets | ||

| Current assets: | ||

| Cash | 188,000 | |

| Accounts receivable | 400,000 | |

| Inventories: | ||

| Materials | 60,000 | |

| Finished goods | 123,000 | 183,000 |

| Total current assets | 771,000 | |

| Property, plant, and equipment: | ||

| Land | 60,000 | |

| Buildings | 1,650,000 | |

| Less: accumulated depreciation | 480,000 | 1,170,000 |

| Factory Equipment | 600,000 | |

| Less: accumulated depreciation | 220,000 | 380,000 |

| Total property, plant, and equipment | 1,550,000 | |

| Total assets | 2,321,000 | |

| Liabilities and stockholders‘ equity | ||

| Current liabilities: | ||

| Accounts payable | 43,500 | |

| Income taxes payable | 142,500 | |

| Total current liabilities | 186,000 | |

| Stockholders’ equity: | ||

| Common stock (100,000 shares of $10 par value) | 1,000,000 | |

| Retained earnings | 1,135,000 | |

| Total stockholders’ equity | 2,135,000 | |

| Total liabilities and stockholders’ equity | 2,321,000 | |

The preparation of Leed’s financial budgeted balance sheet completes the master budget. Management now has information to help appraise the policies it has adopted before implementing them. If the master budget shows the results of these policies to be unsatisfactory, the company can change its policies before serious problems arise.