7.7: Cash Budgets

- Page ID

- 26085

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Cash budget After the preceding analyses have been prepared, sufficient information is available to prepare the cash budget and compute the balance in the Cash account for each quarter. Preparing a cash budget requires information about cash receipts and cash disbursements from all the other operating budget schedules.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=160

Cash receipts We can prepare the cash receipts schedule based on how the company expects to collect on sales. We know, from past experience, how much of our sales are cash sales and how much are credit sales. We also can analyze past accounts receivable to determine when credit sales are typically paid.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=160

Leed Company has determined that all sales are on credit and they do not have any cash sales. For the credit sales, experience tells Leed they will collect 60% of sales in the quarter of the sale and the remaining 40% is collected the quarter after the sale (yes, we understand collecting 100% is unlikely but Leed chooses to budget for 100% collection). Accounts Receivable at the beginning of the year is $200,000 and is expected to be collected in the 1st Quarter. Leed Company prepares the following schedule of planned cash receipts:

| Leed Company | ||||

| Schedule of Cash Receipts | ||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | |

| Budgeted Sales | $600,000 | $1,600,000 | $800,000 | $1,000,000 |

| Cash receipts, current quarter (60% x quarter sales) | 360,000 | 960,000 | 480,000 | 600,000 |

| (600,000 x 60%) | (1,600,000 x 60%) | (800,000 x 60%) | (1,000,000 x 60%) | |

| Cash receipts, from previous qtr (40% x previous quarter sales) | 200,000** | 240,000 | 640,000 | 320,000 |

| (600,000 x 40%) | (1.600,000 x 40%) | (800,000 x 40%) | ||

| Total Cash Collections from Sales | $560,000 | $1,200,000 | $1,120,000 | $920,000 |

** Cash receipts from previous quarter for Quarter 1 comes from the beginning balance in Accounts Receivable.

We can calculate the ENDING balance of Accounts Receivable for the budgeted balance sheet by taking the 4th Quarter sales $1,000,000 x 40% to be received in 1st Quarter of the next year as $400,000. In addition to cash receipts, we also need to understand how we plan to make our cash payments or disbursements.

Cash disbursements Companies need cash to pay for purchases, wages, rent, interest, income taxes, cash dividends, and most other expenses. We can obtain the amount of each cash disbursement from other budgets or schedules.

This video discusses the purchases budget for a merchandiser but if you begin at minute 9 it will pick up with the cash disbursement schedule example.

Leed Company is a manufacturing company and will need to use the information from the materials purchases budget first. Leed Company makes all material purchases on credit. Leed Company will pay for material purchases 80% in the quarter of purchase and 20% in the quarter after the purchase. Accounts Payable at the beginning of the year is $80,000 and will be paid in the 1st Quarter. We will calculate cash payments for material purchases as shown in the following table.

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | |

| Budgeted Material Purchases | $250,000 | $295,000 | $217,500 | $217,500 |

| Cash payments, current quarter (80%) | $200,000 | $236,000 | $174,000 | $174,000 |

| (250,000 x 80%) | (295,000 x 80%) | (217,500 x 80%) | (217,500 x 80%) | |

| Cash payments, from previous qtr (20%) | 80,000** | 50,000 | 59,000 | 43,500 |

| (250,000 x 20%) | (295,000 x 20%) | (217,500 x 20%) | ||

| Total Cash Pmts for Material Purchases | $280,000 | $286,000 | $233,000 | $217,500 |

** Cash payments from previous quarter for Quarter 1 comes from the beginning balance in Accounts Payable.

We can calculate the ENDING balance of Accounts Payable for the budgeted balance sheet by taking the 4th Quarter merchandise purchases of $217,500 x 20% to be paid during 1st Quarter of the next year as $43,500. In addition to these cash payments for merchandise, we also need the cash disbursements from the direct labor budget, manufacturing overhead budget, and selling and administrative budget. Remember, we want the CASH PAYMENT amounts only and not the total budget amount (depreciation is a non-cash expense and is excluded from cash payments).

youtu.be/I96n57H2p54

Using our example, Leed Company, we need the information from the cash payments of merchandise we just calculated, cash payments for direct labor (all direct labor paid in the quarter it was incurred), cash payments for manufacturing overhead and cash payments for selling and administrative expenses. But, we also need information on dividends payments, and income taxes.

Income taxes are assumed to be 40% of budgeted income before income taxes and are paid in the next quarter. *Income taxes payable on January 1 were $100,000. We assume that $40,000 of dividends will be paid in the second quarter and $80,000 in the third quarter. Also, Leed plans to expand operations into a new building that will cost $650,000 in Quarter 4. Leed plans to pay cash for the new building.

The complete schedule of cash payments would look like this:

| Leed Company | |||||

| Schedule of Cash Payments | |||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | ||

| Total Cash Pmts for Material Purchases | 280,000 | 286,000 | 233,000 | 217,500 | from schedule above |

| Budgeted direct labor dollars | 126,000 | 192,000 | 132,000 | 156,000 | from direct labor budget |

| Cash payments for mfg overhead | 80,750 | 89,000 | 81,500 | 80,750 | from mfg overhead budget |

| Cash payments for selling and admin | 110,000 | 160,000 | 120,000 | 130,000 | from selling and admin budget |

| Cash payments for Income Taxes | 100,000* | 57,500 | 270,000 | 100,000 | from budgeted income

stmt |

| Cash payments for dividends | 40,000 | 80,000 | given in information above | ||

| Cash payment for new building | 650,000 | given in information above | |||

| Total Cash Payments | $696,750 | $824,500 | $916,500 | $1,304,250 | |

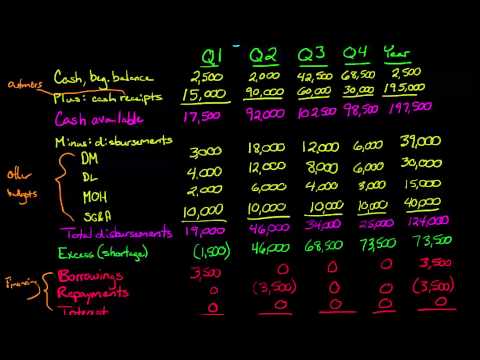

Now let’s put it all together in the complete cash budget. The cash budget is a plan indicating expected inflows and outflows of cash. At the simplest form, a Cash budget is:

| Beginning Cash Balance |

| Add: Cash Receipts |

| Cash Available |

| Subtract: Cash Payments |

| Budgeted Ending Cash Balance |

We can make it a little more complicated by adding financing considerations. The cash budget helps management to decide whether enough cash will be available for short-term needs. If a company’s cash budget indicates a cash shortage at a certain date, the company may need to borrow money on a short-term basis. If the company’s cash budget indicates a cash excess, the company may wish to invest the extra funds for short periods to earn interest rather than leave the cash idle. Knowing in advance that a possible cash shortage or excess may occur allows management sufficient time to plan for such occurrences and avoid a cash crisis.

youtu.be/9j48YgH2VfA

To illustrate, we will complete the cash budget for Leed Company. On January 1, Leed Company’s cash balance was $130,000. We will calculate the cash budget for each quarter using the information from the schedules on this page. We will get our cash receipts from the Schedule of Cash Receipts and the cash disbursements (or payments) from the Schedule of Cash Payments.

Important: The ending cash balance of one quarter is the beginning cash balance of the next quarter!

| Leed Company | ||||

| Cash Budget | ||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | |

| Beginning Cash Balance | $130,000 | $21,250 | $408,750 | $612,250 |

| Add: Cash Receipts (see Schedule of Cash Receipts) | $560,000 | $1,200,000 | $1,120,000 | $920,000 |

| Cash Available | $690,000 | $1,266,250 | $1,573,750 | $1,577,250 |

| Less: Cash Payments (see Schedule of Cash Payments) | $696,750 | $824,500 | $916,500 | $1304,250 |

| Budgeted Ending Cash Balance | -$6,750 | $368,750 | $572,250 | $188,000 |

Leed Company appears to have a little bit of a problem. There is plenty of cash for the year but when we look each quarter, we see we are not planning enough cash to cover the 1st Quarter. We recover in the 2nd quarter and have sufficient cash for the remaining quarters. But what can we do about 1st quarter? We can review the budgets and see if there is anything we can cut or modify. Or, Leed can arrange short term financing with the bank. Leed Company like to keep at a minimum of $10,000 as their ending cash balance each quarter. Leed has arranged a credit line with the bank to access funds on a short term basis. Leed will pay off any loan amount at the next possible quarter and the bank will charge 12% interest per year (3% interest per quarter). How will this change the cash budget if no changes are made to the previous budgets?

| Leed Company | ||||

| Cash Budget | ||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | |

| Beginning Cash Balance | $130,000 | $5,000 | $368,397 | $571,897 |

| Add: Cash Receipts (see Schedule of Cash Receipts) | $560,000 | $1,200,000 | $1,120,000 | $920,000 |

| Cash Available | $690,000 | $1,205,000 | $1,488,397 | $1,491,897 |

| Less: Cash Payments (see Schedule of Cash Payments) | $696,750 | $824,500 | $916,500 | $1,304,250 |

| Projected Ending Cash Balance | ($6,750) | $380,500 | $571,897 | $187,647 |

| Add: Short Term Financing Received | $11,750 | |||

| Less: Short Term Financing Payment | ($11,750) | |||

| Less: Short Term Financing Interest | ($353) | |||

| Budgeted Ending Cash Balance | $5,000 | $368,397 | $571,897 | $187,647 |

Notice how Leed borrowed $11,750 in the 1st Quarter to cover the $6,750 shortage + $5,000 minimum we want on hand. Leed plans to pay the loan off during the 2nd quarter by paying the full amount of $11,750 plus interest for 1 quarter (11,750 x 3% per quarter).

- The Cash Budget. Authored by: Education Unlocked. Located at: youtu.be/HT0c22HF5hA. License: All Rights Reserved. License Terms: Standard YouTube License

- The Cash Budget Part 1, Sales Budget and Collections Budget (Managerial Accounting Tutorial #39) . Authored by: Note Pirate. Located at: youtu.be/iYlBGkEBb_E. License: All Rights Reserved. License Terms: Standard YouTube License

- The Cash Budget Part 2, Inventory Purchases Budget (Managerial Accounting Tutorial #40) . Authored by: Note Pirate. Located at: youtu.be/tn1atrXrwn8. License: All Rights Reserved. License Terms: Standard YouTube License

- The Cash Budget Part 3, Operating Expenses Budget (Managerial Accounting Tutorial #41) . Authored by: Note Pirate. Located at: youtu.be/I96n57H2p54. License: All Rights Reserved. License Terms: Standard YouTube License