7.6: Manufacturing Budgets

- Page ID

- 26084

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)In a manufacturing company, you will have a budget for all of your manufacturing costs including Direct Materials, Direct Labor and Overhead. Each cost will have their own budget. You will need the information from the Sales and Production budgets to complete these 3 budgets.

Materials Budget

The materials budget (or materials purchases budget) is used to plan how much raw materials we need to have available to meet budgeted production. This budget is prepare similarly to the production budget as the company must decide how much raw materials inventory they want to have on hand at the end of each quarter. This is typically determined as a percent of next quarter’s material needs. In a materials budget, we will deal with units first and then add the budgeted cost near the end. We also need to know how many direct materials are needed for each unit.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=158

For Leed Company, our budgeted cost is $2 per pound. We need 5 pounds of materials for each unit. We want to maintain 25% of next quarter’s production needs in ending inventory. Beginning raw materials inventory was 20,000 pounds (at $2 per pound) and we are expecting ending raw materials inventory to be 30,000 pounds.

| Leed Company | |||||

| Materials Purchases Budget | |||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | YEAR | |

| Units to be produced (from production budget) | 21,000 | 32,000 | 22,000 | 21,000 | 96,000 |

| x lbs. of materials required per unit | x 5 lb. | x 5 lb. | x 5 lb. | x 5 lb | |

| Pounds of materials required for production | 105,000 | 160,000 | 110,000 | 105,000 | 480,000 |

| Add: Desired Ending Inventory | 40,000 | 27,500 | 26,250 | 30,000 | 30,000 |

| Total Material Needed | 145,000 | 187,500 | 136,250 | 135,000 | 510,000 |

| Less: Beginning Inventory | (20,000) | (40,000) | (27,500) | (26,250) | (20,000) |

| Material to be Purchased (in lbs) | 125,000 | 147,500 | 108,750 | 108,750 | 460,000 |

| x $2 cost per pound | x $ 2 | x $ 2 | x $ 2 | x $ 2 | |

| Total Material to be Purchased (in $) | $250,000 | $295,000 | $217,500 | $217,500 | $980,000 |

Just like with the production budget, please note the following items:

- Ending inventory is calculated as NEXT quarter’s production needs x 25% for all but quarter 4.

- Quarter 4 ending inventory is the same as the ending inventory for the year and was given in the example.

- Beginning inventory refers to the previous quarters ending inventory for all quarters except quarter 1. For quarter 1, beginning raw materials was given in the problem and should also be the beginning inventory for the YEAR. If beginning inventory is not provided, assume the company followed the same inventory policy last year and multiply Quarter 1 pounds of materials needed x percent provided for ending inventory.

- Quarter 2 beginning is quarter 1 ending inventory. Quarter 3 beginning is quarter 2 ending inventory and quarter 4 beginning is quarter 3 ending inventory.

The total material to be purchased will be used later in the cash disbursement section of the CASH budget.

Direct Labor Budget

The direct labor budget is a very easy one. We need to know the units required from the production budget. Next, we need to know how many direct labor hours it takes to complete one unit and the cost per labor hour. Using this information, we can determine how many direct labor hours are required to meet the budgeted level of production. We will take the production units x direct labor per unit to get the number of direct labor hours. Finally, we will take the direct labor hours x the rate per hour.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=158

For Leed Company, each unit requires 0.5 hours of direct labor and the hourly rate is $12 per hour. The direct labor budget would be:

| Leed Company | |||||

| Direct Labor Budget | |||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | YEAR | |

| Units to be produced | 21,000 | 32,000 | 22,000 | 21,000 | 96,000 |

| x 0.5 DL hour per unit | x 0.5 hr | x 0.5 hr | x 0.5 hr | x 0.5 hr | |

| Direct Labor Hours Required | 10,500 | 16,000 | 11,000 | 10,500 | 48,000 |

| x $12 per hour | x $12 | x $12 | x $12 | x $12 | |

| Budgeted direct labor dollars | $126,000 | $192,000 | $132,000 | $126,000 | $576,000 |

The budgeted direct labor dollar amount will be used later in the cash disbursement section of the CASH budget.

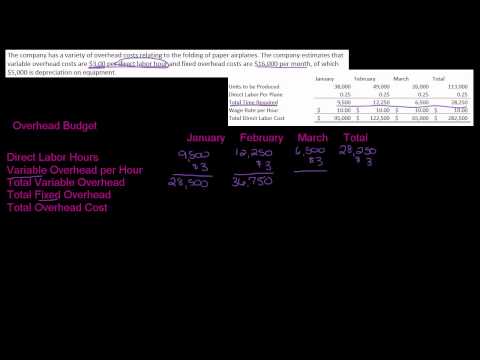

Manufacturing Overhead Budget

The final budget for manufacturing is the manufacturing overhead budget. The manufacturing overhead budget is prepare depending on how the company allocates overhead. The company can choose to allocate overhead using one predetermined overhead rate, departmental rates or using activity-based costing. Further, the company can choose to separate the fixed and variable overhead costs and assign costs to overhead using only the variable overhead.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=158

Leed Company has decided to allocate variable overhead on the basis of $1.50 per direct labor hour and fixed overhead is $75,000 per quarter. Depreciation on the factory machinery of $10,000 per quarter is included in the fixed overhead.

| Leed Company | |||||

| Mfg. Overhead Budget | |||||

| Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | YEAR | |

| Budgeted direct labor hours (from direct labor budget) | 10,500 | 16,000 | 11,000 | 10,500 | 48,000 |

| x Variable OH per unit | x $1.50 | x $1.50 | x $1.50 | x $1.50 | |

| Variable Overhead Cost | $15,750 | $24,000 | $16,500 | $15,750 | $72,000 |

| Fixed Overhead Cost | 75,000 | 75,000 | 75,000 | 75,000 | 300,000 |

| Total Overhead Cost | $90,750 | $99,000 | $91,500 | $90,750 | $372,000 |

| Less: Depreciation on Factory Machinery | (10,000) | (10,000) | (10,000) | (10,000) | (40,000) |

| Total Cash payments for mfg overhead | $80,750 | $89,000 | $81,500 | $80,750 | $332,000 |

We will use the information from the overhead budget in the cash disbursement section of the cash budget.

- Direct Materials Budget, Part 1. Authored by: Kristin Ingram. Located at: youtu.be/jgN_E4qlkI4. License: All Rights Reserved. License Terms: Standard YouTube License

- Direct labor Budget. Authored by: Kristin Ingram. Located at: youtu.be/sqUuV_Y5TYM. License: All Rights Reserved. License Terms: Standard YouTube License

- Overhead budget. Authored by: Kristin Ingram. Located at: youtu.be/nb9SoL8M5AU. License: All Rights Reserved. License Terms: Standard YouTube License