11.4: Appendix A- Putting It All Together- Corporate Financial Statements

- Page ID

- 98198

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

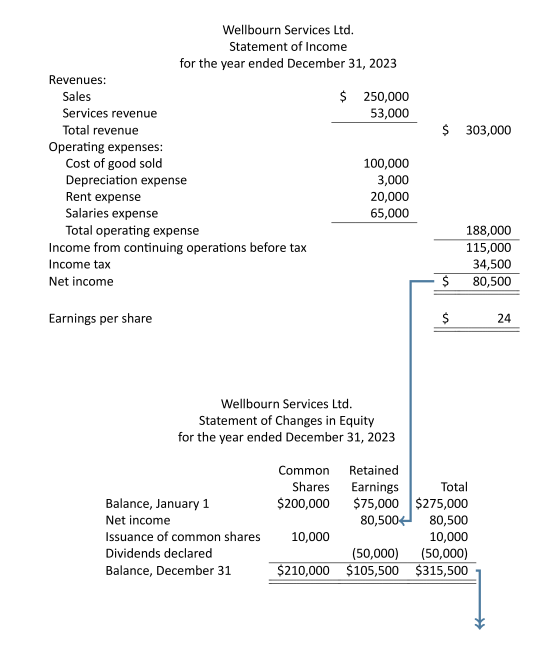

The core financial statements connect to complete an overall picture of the company's operations and its current financial state. It is important to understand how these reports connect; therefore, a review of some simplified financial statements for Wellbourn Services Ltd. is presented below.

As can be seen from the flow of the numbers above, the net income from the statement of income is closed to retained earnings.

The statement of changes in equity total column flows to the equity section of the balance sheet. Finally, the statement of cash flows (SCF) ending cash balance must be equal to the cash ending balance reported in the balance sheet, which completes the loop of interconnecting accounts and amounts.

Statement of Income with Discontinued Operations

Single-step and Multiple-step Statement of Income

Companies can choose whichever format best suits their reporting needs. Smaller companies tend to use the simpler single-step format, while larger companies tend to use the multiple-step format.

The Wellbourn Services Ltd. statement of income, shown earlier, is an example of a typical single-step income statement. For this type of statement, revenue and expenses are each reported in the two sections for continuing operations. Discontinued operations are separately reported below the continuing operations. The separate disclosure and format for the discontinued operations section is a reporting requirement and is discussed and illustrated below. The single-step format makes the statement simple to complete and keeps sensitive information out of the hands of competitive companies, but provides little in the way of analytical detail.

The multiple-step income statement format provides much more detail. Below is an example of a multiple-step statement of income for Toulon Ltd. for the year ended December 31, 2023.

The multiple-step format with its section subtotals makes performance analysis and ratio calculations such as gross profit margins easier to complete and makes it easier to assess the company's future earnings potential. The multiple-step format also enables investors and creditors to evaluate company performance results from continuing and ongoing operations having a high predictive value separately, compared to non-operating or unusual items having little predictive value.

Operating Expenses

As discussed in an earlier chapter, expenses from operations can be reported by their nature and, optionally, by function. Expenses by nature relate to the type of expense or the source of expense such as salaries, insurance, advertising, travel and entertainment, supplies expense, depreciation and amortization, and utilities expense, to name a few. The statement for Toulon Ltd. is an example of reporting expenses by nature.

Expenses by function relate to how various expenses are incurred within the various departments and activities of a company such as selling and administrative expenses.

The sum of all the revenues, expenses, gains, and losses to this point represents the income or loss from continuing operations. This is a key component used in performance analysis.

Income Tax Allocations

This is the process of allocating income tax expense to various categories within the statement of income such as income from continuing operations before taxes and discontinued operations. The purpose of these allocations is to make the information within the statements more informative and complete. For example, Toulon's statement of income for the year ending December 31, 2023, allocates tax at a rate of 30% to the following:

- Income from continuing operations of $850,000 (

)

) - Loss from disposal of discontinued operations of $63,000

Discontinued operations

Sometimes companies will sell or shut down certain business operations because the operating segment is no longer profitable, or they may wish to focus their resources on other business operations. Examples are a major business line or geographical area. If the discontinued operation has not yet been sold, then there must be a formal plan in place to dispose of the component within one year and to report it as a discontinued operation.

The items reported in this section of the statement of income are to be reported net of tax, with the tax amount disclosed.

Earnings per Share

Basic earnings per share represent the amount of income attributable to each outstanding common share, as shown in the calculation below:

![]()

The earnings per share amounts are not required for private companies. This is because ownership of privately owned companies is often held by only a few investors, compared to publicly-traded companies where shares are held by many investors.

Basic earnings per share are to be reported on the face of the statement of income as follows:

- Basic EPS from continuing operations

- Basic EPS from discontinued operations, if any

If the outstanding common shares for Toulon was 121,500, the EPS from continuing operations would be $16.32 (![]() ) and $(1.21) from discontinued operations (

) and $(1.21) from discontinued operations (![]() ), as reported in their statement above. There is also a requirement to report diluted EPS but this is beyond the scope of this course.

), as reported in their statement above. There is also a requirement to report diluted EPS but this is beyond the scope of this course.