11.5: Appendix B- Statement of Cash Flows – Direct Method

- Page ID

- 98199

The Importance of Cash Flow – For Better, For Worse, For Richer, For Poorer...

A business is a lot like a marriage. It takes work to make it succeed. One of the keys to business success is managing and maintaining adequate cash flows. In the field of financial management, there is an old saying that revenue is vanity, profits are sanity, but cash is king. In other words, a firm's revenues and profits may look spectacular, but this does not guarantee there will be cash in the bank. Without cash, a business cannot pay its bills and it will ultimately not survive.

Let's take a look at the distinctions between revenue and profits, and cash, using a numeric example for a new business:

| Income Statement | Cash Flows | ||||

| Revenue* | $ | 1,000,000 | Revenue (cash received) | $ | 400,000 |

| Cost of goods sold** | (500,000) | Cost of goods sold (paid in cash) | (300,000) | ||

| Gross profit | 500,000 | Net cash | 100,000 | ||

| Operating expenses*** | 200,000 | Operating expenses (paid in cash) | 90,000 | ||

| Net income/net profit | $ | 300,000 | Net cash | $ | 10,000 |

* Sales of $400,000 were paid in cash

** Purchases of $300,000 were paid in cash

*** Operating expenses of $90,000 were cash paid

Revenue is reported in the income statement as $1 million which is a sizeable amount, but only $400,000 was cash paid by customers. (The rest is reported as accounts receivable.) Gross profit is reported in the income statement as $500,000. This is also a respectable number, but only $100,000 translates into a positive cash flow, because only some of the inventory purchases were paid in cash. (The rest of the inventory is reported as accounts payable.) The company must still pay some of its operating expenses, leaving only $10,000 cash in the bank.

When investors and creditors review the income statement, they will see $1 million in revenue with gross profits of one-half million or 50%, and a respectable net income of $300,000 or 30% of revenue. They could conclude that this looks pretty good for the first year of operations and incorrectly assume that the company now has $300,000 available to spend.

However, lurking deeper in the financial statements is the cash position of the company–the amount of cash left over from this operating cycle. Sadly, there is only $10,000 cash in the bank, so the company cannot even pay its remaining accounts payable in the short term. So, how can management keep track of its cash?

The statement of cash flows is the definitive financial statement to bridge the gaps between revenues and profits, and cash. Therefore, it is vital to understand the statement of cash flows.

As cash is generally viewed by many as the most critical asset to success, this appendix will focus on how to correctly prepare and interpret the statement of cash flows using the direct method.

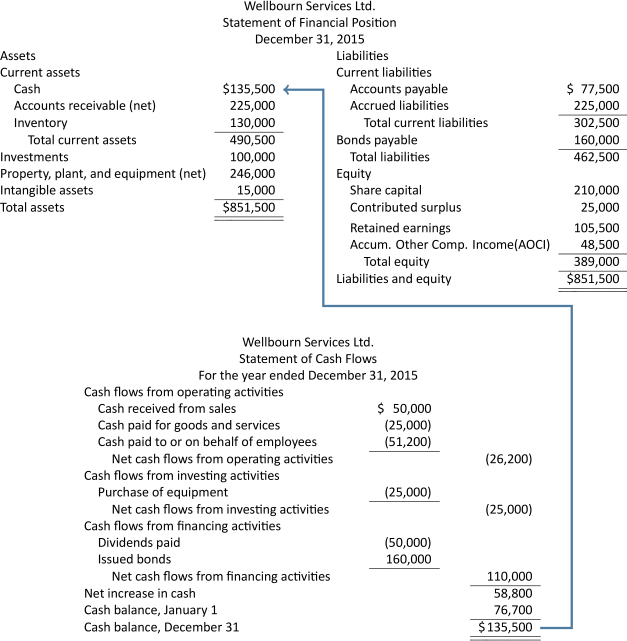

For example, below is the statement of cash flows using the direct method for the year ended December 31, 2015 for Wellbourn Services Ltd. at December 31, 2015.

Note how Wellbourn's ending cash balance of $135,500, from the statement of cash flows for the year ended December 31, matches the ending cash balance in the balance sheet on that date. This is a critical relationship between these two financial statements. The balance sheet provides information about a company's resources (assets) at a specific point in time, and whether these resources are financed mainly by debt (current and long-term liabilities) or equity (shareholders' equity). The statement of cash flows identifies how the company utilized its cash inflows and outflows over the reporting period and, ultimately, ends with its current cash and cash equivalents balance at the balance sheet date. As well, since the statement of cash flows is prepared on a cash basis, it excludes non-cash accruals like depreciation and interest, making the statement of cash flows harder to manipulate than the other financial statements.

Two methods are used to prepare a statement of cash flows, namely the indirect method and the direct method. The indirect method was discussed earlier in this chapter. Both methods organize the reported cash flows into three activities: operating, investing, and financing. The only difference when applying the direct method is in the operating activities section; the investing and financing sections are prepared exactly the same way for both methods.

For the direct method categories are based on the nature of the cash flows. With the indirect method the cash flows are based on the income statement and changes in each current asset and liability account, except cash. Below is a comparison of the two methods:

| Indirect Method | Direct Method | ||||

| Cash flows from operating activities: | Cash flows from operating activities: | ||||

| Net income | $$ | Cash received from sales | $$ | ||

| Adjust for non-cash items: | Cash paid for goods and services | ($$) | |||

| Depreciation | $$ | Cash paid to or on behalf of employees | ($$) | ||

| Gain on sale of asset | ($$) | Cash received for interest income | $$ | ||

| Increase in accounts receivable | ($$) | Cash paid for interest | ($$) | ||

| Decrease in inventory | $$ | Cash paid for income taxes | ($$) | ||

| Increase in accounts payable | $$ | Cash received for dividends | $$ | ||

| Net cash flows from operating activities | $$ | Net cash flows from operating activities | $$ | ||

The direct method is straightforward due to the grouping of information by nature. This also makes interpretation of the statement easier for stakeholders. However, companies record thousands of transactions every year and many of them do not involve cash. Since the accounting records are kept on an accrual basis, it can be a time-consuming and expensive task to separate and collect the cash-only data required for the direct method categories by nature. Also, reporting on sensitive information, such as cash receipts from customers and cash payments to suppliers, may not be in the best interest of the company in light of competitor companies using the information to their advantage. For these reasons, many companies prefer not to use the direct method, even though IFRS standards prefer its use over the indirect method. Also, the indirect method may be easier to prepare because it collects much of its data directly from the existing income statement and balance sheet. However, it is more difficult to understand because it uses the accounts-based categories as shown above.

11.5.1. Preparing a Statement of Cash Flows: Direct Method

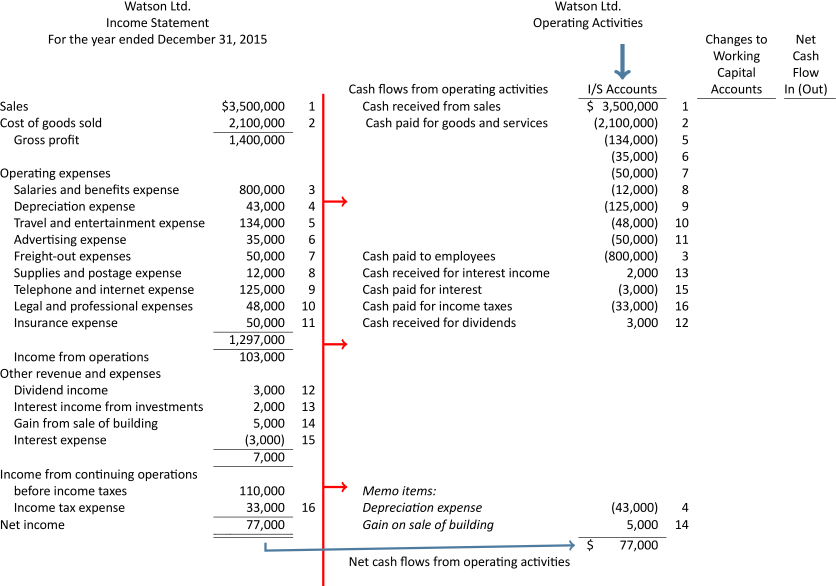

As with the indirect method, preparing a statement of cash flows using the direct method is made much easier if specific steps are followed in sequence. Below is a summary of those steps to complete the operating section of the statement of cash flows using the direct method for Watson Ltd:

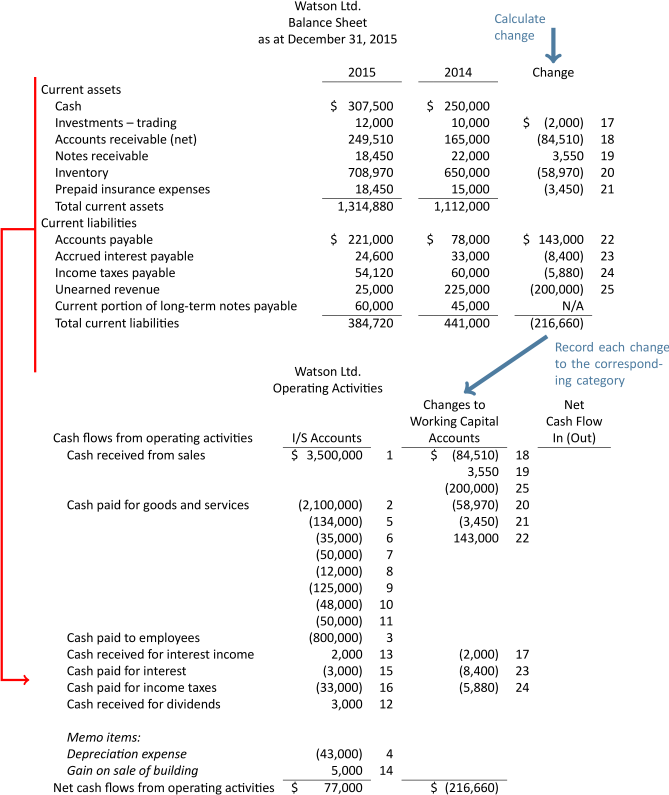

| Watson Ltd. | ||||

| Partial Balance Sheet | ||||

| As at December 31, 2015 | ||||

| 2015 | 2014 | |||

| Current assets | ||||

| Cash | $ | 307,500 | $ | 250,000 |

| Investments – trading | 12,000 | 10,000 | ||

| Accounts receivable (net) | 249,510 | 165,000 | ||

| Notes receivable | 18,450 | 22,000 | ||

| Inventory (LCNRV) | 708,970 | 650,000 | ||

| Prepaid insurance expenses | 18,450 | 15,000 | ||

| Total current assets | 1,314,880 | 1,112,000 | ||

| Current liabilities | ||||

| Accounts payable | $ | 221,000 | $ | 78,000 |

| Accrued interest payable | 24,600 | 33,000 | ||

| Income taxes payable | 54,120 | 60,000 | ||

| Unearned revenue | 25,000 | 225,000 | ||

| Current portion of long-term notes payable | 60,000 | 45,000 | ||

| Total current liabilities | 384,720 | 441,000 | ||

| Watson Ltd. | ||

| Income Statement | ||

| For the Year Ended December 31, 2015 | ||

| Sales | $ | 3,500,000 |

| Cost of goods sold | 2,100,000 | |

| Gross profit | 1,400,000 | |

| Operating expenses | ||

| Salaries and benefits expense | 800,000 | |

| Depreciation expense | 43,000 | |

| Travel and entertainment expense | 134,000 | |

| Advertising expense | 35,000 | |

| Freight-out expense | 50,000 | |

| Supplies and postage expense | 12,000 | |

| Telephone and internet expense | 125,000 | |

| Legal and professional expenses | 48,000 | |

| Insurance expense | 50,000 | |

| 1,297,000 | ||

| Income from operations | 103,000 | |

| Other revenue and expenses | ||

| Dividend income | 3,000 | |

| Interest income | 2,000 | |

| Gain from sale of building | 5,000 | |

| Interest expense | (3,000) | |

| 7,000 | ||

| Income from continuing operations before income tax | 110,000 | |

| Income tax expense | 33,000 | |

| Net income | $ | 77,000 |

Direct Method Steps:

Step 1. Record headings, categories, and three additional columns into an Operating Activities worksheet as shown below:

| Watson Ltd. | |||

| Operating Activities | |||

| Cash flows from operating activities | I/S Accounts | Changes to Working Capital Accounts | Net Cash Flow In (Out) |

| Cash received from sales | |||

| Cash paid for goods and services | |||

| Cash paid to employees | |||

| Cash received for interest income | |||

| Cash paid for interest | |||

| Cash paid for income taxes | |||

| Cash received for dividends | |||

| Net cash flows from operating activities | |||

Step 2. Record each income statement amount into the corresponding direct method category of the Operating Activities worksheet shown below (recall that non-cash items such as depreciation and gains or losses are excluded from a statement of cash flows so they are will be recorded as memo items only):

Step 3. Calculate the net change amount for each current asset (except cash), and each current liability from the balance sheet below. Record each change amount in the second column of the Operating Activities worksheet:

Note how items 13 and 17 on the operating activities statement cancel each other out. This is because the interest income was accrued and not actually received in cash. Also note that the current portion of long-term notes was excluded from the operating activities section. Recall from the earlier chapter material on the indirect method that this account is combined with its corresponding long-term note payable account in the financing section of the statement of cash flows.

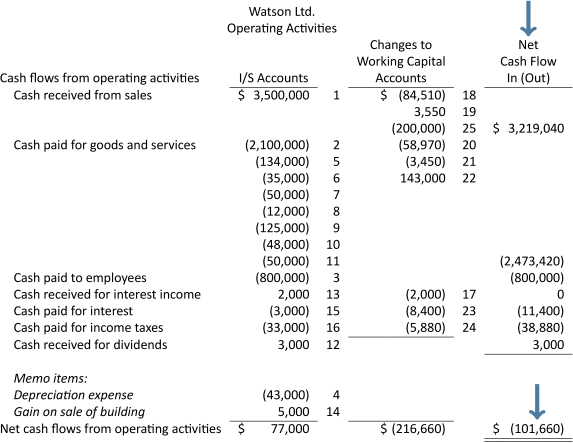

Step 4. Calculate the net cash flow total for each category and the net cashflow total for the operating activities section. Transfer the amounts to the statement of cash flows, operating activities section:

The completed portion of the statement of cash flows, operating section is shown below:

| Watson Ltd. | ||||

| Statement of Cash Flows – Operating Activities | ||||

| For the Year Ended December 31, 2015 | ||||

| Cash flows from operating activities: | ||||

| Cash received from sales | $ | 3,219,040 | ||

| Cash paid for goods and services | (2,473,420) | |||

| Cash paid to or on behalf of employees | (800,000) | |||

| Cash paid for interest | (11,400) | |||

| Cash paid for income taxes | (38,880) | |||

| Cash received for dividends | 3,000 | |||

| Net cash flows from operating activities | $ | (101,660) | ||