11.3: Interpreting the Statement of Cash Flows

- Page ID

- 98197

- LO2 – Prepare a statement of cash flows.

The general format for a SCF is shown in Figure 11.1. The SCF details the cash inflows and outflows that caused the beginning of the period cash account balance to change to its end of period balance.

| Name of Company | ||

| Statement of Cash Flows | ||

| For the Period Ended | ||

| Cash flows from operating activities: | ||

| [Each operating inflow/outflow is listed] | ||

|

Net cash inflow/outflow from operating activities |

$ | XX |

| Cash flows from investing activities: | ||

| [Each investing inflow/outflow is listed] | ||

|

Net cash inflow/outflow from investing activities |

XX | |

| Cash flows from financing activities: | ||

|

[Each financing inflow/outflow is listed] |

||

| Net cash inflow/outflow from financing activities | XX | |

| Net increase/decrease in cash | $ | XX |

| Cash at beginning of period | XX | |

| Cash at end of period | $ | XX |

Classifying Cash Flows—Operating Activities

Cash flow from operating activities represents cash flows generated from the principal activities that produce revenue for a corporation, such as selling products, and the related expenses reported on the income statement. Because of accrual accounting, the net income reported on the income statement includes noncash transactions. For example, revenue earned on account is included in accrual net income but it does not involve cash (debit accounts receivable and credit revenue). Therefore, the operating activities section of the SCF must convert accrual net income to a cash basis net income. There are two generally accepted methods for preparing the operating activities section of the SCF, namely the direct method and the indirect method. This chapter illustrates the indirect method because it is more commonly used in Canada. The direct method is addressed in a different textbook. Both methods result in the same cash flows from operating activities — it is the way in which the number is calculated that differs. The method used has an impact on only the operating activities section and not on the investing or financing activities sections.

In using the indirect method for preparing the operating activities section, the accrual net income is adjusted for changes in current assets (except cash), current liabilities (except dividends payable), depreciation expense, and gains/losses on the disposition of non-current assets. Figure 11.2 illustrates the effect of these items on the SCF.

| Cash flows from operating activities: | ||

| Net income/net loss | $ | XX |

| Adjustments to reconcile net income/loss to cash provided/used by operating activities: | ||

| Add: Decreases in current assets (except Cash) | XX | |

| Subtract: Increases in current assets (except Cash) | XX | |

| Add: Increases in current liabilities (except Dividends payable) | XX | |

| Subtract: Decreases in current liabilities (except Dividends payable) | XX | |

| Add: Depreciation expense | XX | |

| Add: Losses on disposal of non-current assets | XX | |

| Subtract: Gains on disposal of non-current assets | XX | |

| Net cash inflow/outflow from operating activities | $ | XX |

Increases in current liabilities are added back as an adjustment to net income because, for example, an increase in accounts payable indicates that a purchase/expense was made on account (debit expense and credit accounts payable) so it was subtracted in calculating accrual net income. However, since no cash was paid, this must be added back to accrual net income to adjust it to a cash basis. A decrease in accounts payable indicates that a payment was made to a creditor (debit accounts payable and credit cash) yet it is not part of accrual net income so the cash paid must be subtracted.

Depreciation expense is subtracted in calculating accrual net income. However, an analysis of the journal entry shows that no cash was involved (debit depreciation expense and credit accumulated depreciation), so it must be added back to adjust the accrual net income to a cash basis.

A loss on the disposal of a non-current asset is added back as an adjustment to net income because, in analyzing the journal entry when losses occur (e.g., debit cash, debit loss, credit land), the loss represents the difference between the cash proceeds and the book value of the non-current asset. Since a loss is subtracted on the income statement and does not represent a cash outflow, it is added back to adjust the accrual net income to a cash basis. The same logic applies for a gain on the disposal of a non-current asset.

Classifying Cash Flows—Investing Activities

Cash flows from investing activities involve increases and decreases in long-term asset accounts. These include outlays for the acquisition of property, plant, and equipment, as well as proceeds from their disposal. Figure 11.3 illustrates the effect of these items on the SCF.

| Cash flows from investing activities: | ||

| Cash proceeds from sale of non-current assets | XX | |

| Cash paid to purchase non-current assets | XX | |

| Net cash inflow/outflow from investing activities | XX |

Classifying Cash Flows—Financing Activities

Cash flows from financing activities result when the composition of the debt and equity capital structure of the entity changes. This category is generally limited to increases and decreases in long-term liability accounts and share capital accounts such as common and preferred shares. These include cash flows from the issue and repayment of debt, and the issue and repurchase of share capital. Dividend payments are generally considered to be financing activities, since these represent a return to shareholders on the original capital they invested. Figure 11.4 illustrates the effect of these items on the SCF.

| Cash flows from financing activities: | ||

| Cash proceeds from issuance of shares | XX | |

| Cash paid for repurchase of shares | XX | |

| Cash proceeds from borrowings | XX | |

| Cash repayments of borrowings | XX | |

| Cash paid for dividends | XX | |

| Net cash inflow/outflow from financing activities | XX |

Classifying Cash Flows—Noncash Investing and Noncash Financing Activities

There are some transactions that involve the direct exchange of non-current balance sheet items so that cash is not affected. For example, noncash investing and noncash financing activities would include the purchase of a non-current asset by issuing debt or share capital, the declaration and issuance of a share dividend, retirement of debt by issuing shares, or the exchange of noncash assets for other noncash assets. Although noncash investing and noncash financing activities do not appear on the SCF, the full disclosure principle requires that they be disclosed either in a note to the financial statements or in a schedule on the SCF.

Now, let us demonstrate the preparation of a SCF using the balance sheet, income statement, and statement of changes in equity of Example Corporation shown below.

| Example Corporation | ||||

| Balance Sheet | ||||

| At December 31 | ||||

| ($000s) | ||||

| 2023 | 2022 | |||

| Assets | ||||

| Current assets | ||||

|

Cash |

$ | 27 | $ | 150 |

|

Accounts receivable |

375 | 450 | ||

|

Merchandise inventory |

900 | 450 | ||

|

Prepaid expenses |

20 | 10 | ||

|

Total current assets |

1,322 | 1,060 | ||

| Property, plant, and equipment | ||||

|

Land |

70 | 70 | ||

|

Buildings |

1,340 | 620 | ||

|

Less: Accumulated depreciation - buildings |

(430) | (280) | ||

|

Machinery |

1,130 | 920 | ||

|

Less: Accumulated depreciation - machinery |

(250) | (240) | ||

|

Total property, plant, and equipment |

1,860 | 1,090 | ||

| Total assets | $ | 3,182 | $ | 2,150 |

| Liabilities | ||||

| Current liabilities | ||||

|

Accounts payable |

$ | 235 | $ | 145 |

|

Dividends payable |

25 | 30 | ||

|

Income taxes payable |

40 | 25 | ||

|

Total current liabilities |

300 | 200 | ||

| Long-term loan payable | 1,000 | 500 | ||

| Total liabilities | 1,300 | 700 | ||

| Equity | ||||

| Common shares | 1,210 | 800 | ||

| Retained earnings | 672 | 650 | ||

|

Total equity |

1,882 | 1,450 | ||

| Total liabilities and equity | $ | 3,182 | $ | 2,150 |

| Example Corporation | ||||

| Income Statement | ||||

| For the Year Ended December 31, 2023 | ||||

| ($000s) | ||||

| Sales | $ | 1,200 | ||

| Cost of goods sold | 674 | |||

| Gross profit | 526 | |||

| Operating expenses | ||||

| Selling, general, and administration | $ | 115 | ||

| Depreciation | 260 | 375 | ||

| Income from operations | 151 | |||

| Other revenues and expenses | ||||

| Interest expense | 26 | |||

| Loss on disposal of machinery | 10 | 36 | ||

| Income before income taxes | 115 | |||

| Income taxes | 35 | |||

| Net Income | $ | 80 | ||

| Example Corporation | ||||||

| Statement of Changes in Equity | ||||||

| For the Year Ended December 31, 2023 | ||||||

| ($000s) | ||||||

| Share Capital | Retained Earnings | Total Equity | ||||

| Opening balance | $ | 800 | $ | 650 | $ | 1,450 |

| Common shares issued | 410 | - | 410 | |||

| Net income | - | 80 | 80 | |||

| Dividends declared | - | (58) | (58) | |||

| Ending balance | $ | 1,210 | $ | 672 | $ | 1,882 |

The SCF can be prepared from an analysis of transactions recorded in the Cash account. Accountants summarize and classify these cash flows on the SCF for the three major activities noted earlier, namely operating, investing, and financing. To aid our analysis, the following list of additional information from the records of Example Corporation will be used.

Additional Information

- A building was purchased for $720 cash.

- Machinery was purchased for $350 cash.

- Machinery costing $140 with accumulated depreciation of $100 was sold for $30 cash.

- Total depreciation expense of $260 was recorded during the year; $150 on the building and $110 on the machinery.

- Example Corporation received $500 cash from issuing a long-term loan with the bank.

- Shares were issued for $410 cash.

- $58 of dividends were declared during the year.

Analysis of Cash Flows

There are different ways to analyze cash flows and then prepare the SCF; only one of those techniques will be illustrated here using the following steps.

- Set up a cash flow table.

- Calculate the changes in each balance sheet account.

- Calculate and analyze the changes in retained earnings and dividends payable (if there is a Dividends Payable account).

- Calculate and analyze the changes in the noncash current assets and current liabilities (excluding Dividends Payable account).

- Calculate and analyze changes in non-current asset accounts

- Calculate and analyze changes in Long-term Liability and Share Capital accounts.

- Reconcile the analysis.

- Prepare a statement of cash flows.

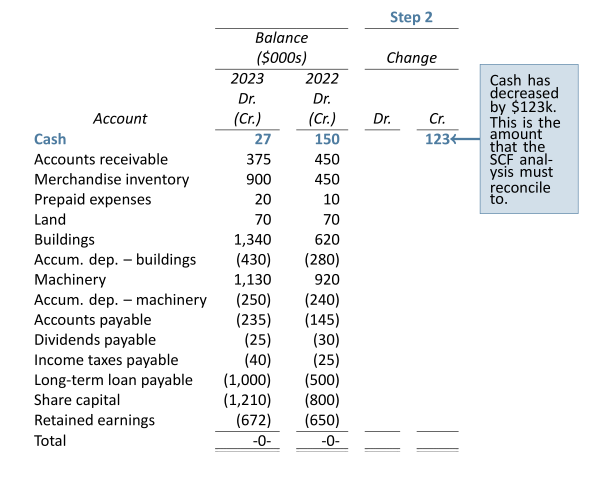

Step 1: Set up a cash flow table

Set up a table as shown below with a row for each account shown on the balance sheet. Enter amounts for each account for 2022 and 2023. Show credit balances in parentheses. Total both columns and ensure they equal zero. The table should appear as follows after this step has been completed:

| Balance | ||

| ($000s) | ||

| Account | 2023 Dr. (Cr.) | 2022 Dr. (Cr.) |

| Cash | 27 | 150 |

| Accounts receivable | 375 | 450 |

| Merchandise inventory | 900 | 450 |

| Prepaid expenses | 20 | 10 |

| Land | 70 | 70 |

| Buildings | 1,340 | 620 |

| Accum. dep.- buildings | (430) | (280) |

| Machinery | 1,130 | 920 |

| Accum. dep.- machinery | (250) | (240) |

| Accounts payable | (235) | (145) |

| Dividends payable | (25) | (30) |

| Income taxes payable | (40) | (25) |

| Long-term loan payable | (1,000) | (500) |

| Share capital | (1,210) | (800) |

| Retained earnings | (672) | (650) |

| Total | -0- | -0- |

Step 2: Calculate the change in cash

Add two columns to the cash flow table. Calculate the net debit or net credit change in cash and insert this change in the appropriate column. This step is shown below.

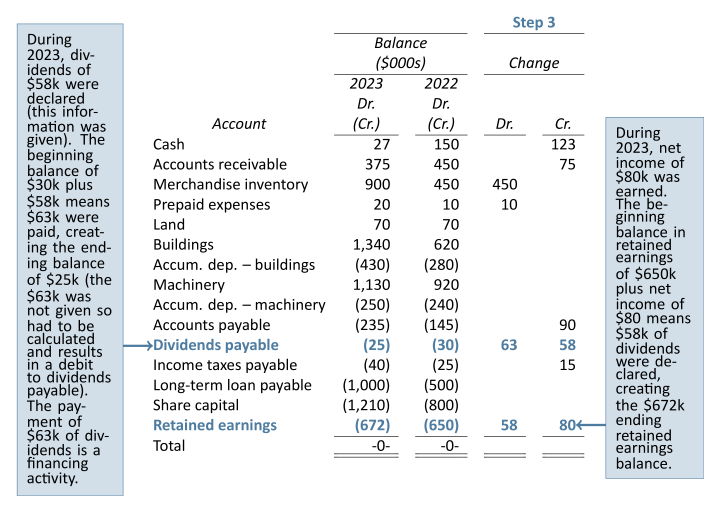

Step 3: Calculate and analyze the changes in retained earnings and dividends payable (if there is a Dividends Payable account)

When we calculate the changes for each of retained earnings and dividends payable, the net difference may not always reflect the causes for change in these accounts. For example, the net difference between the beginning and ending balances in retained earnings is an increase of $22 thousand. However, two things occurred to cause this net change: a net income of $80 thousand (a debit to income summary and a credit to retained earnings) and dividends of $58 thousand that were declared during the year per the additional information (a debit to retained earnings of $58k and a credit to dividends payable of $58k). The net income of $80 thousand is the starting position in the operating activities section of the SCF (see Figure 11.5).

The change in the dividends payable balance was also caused by two transactions — the dividend declaration of $58 thousand (a debit to retained earnings and a credit to dividends payable) and a $63 thousand payment of dividends (a debit to dividends payable and a credit to cash). The $63 thousand cash payment is subtracted in the financing activities section of the SCF (see Figure 11.5). Dividends payable can change because of two transactions, as in this example, or because of one transaction, which could be either a dividend declaration with no payment of cash, or a payment of the dividend payable and no dividend declaration. Step 3 as it applies to Example Corporation is detailed below.

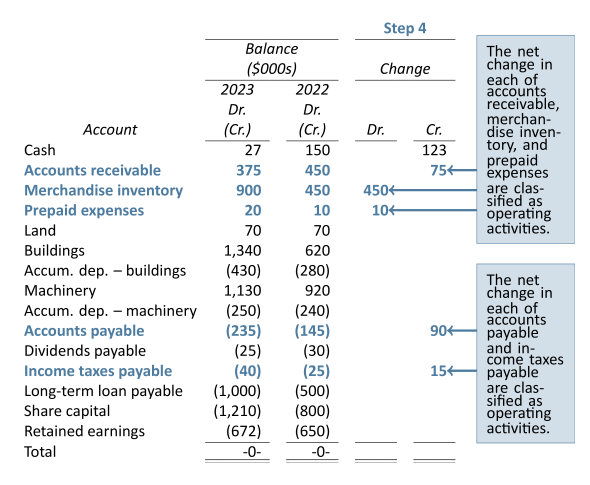

Step 4: Calculate and analyze the changes in the noncash current assets and current liabilities (excluding Dividends Payable account)

Calculate the net debit or net credit changes for each current asset and current liability account on the balance sheet and insert these changes in the appropriate column. Step 4 as it applies to Example Corporation is detailed below. The $75 thousand decrease in accounts receivable is added in the operating activities section of the SCF, the $450 thousand increase in merchandise inventory is subtracted, the $10 thousand increase in prepaid expenses is subtracted, the $90 thousand increase in accounts payable is added, and the $15 thousand increase in income taxes payable is added (see Figure 11.5).

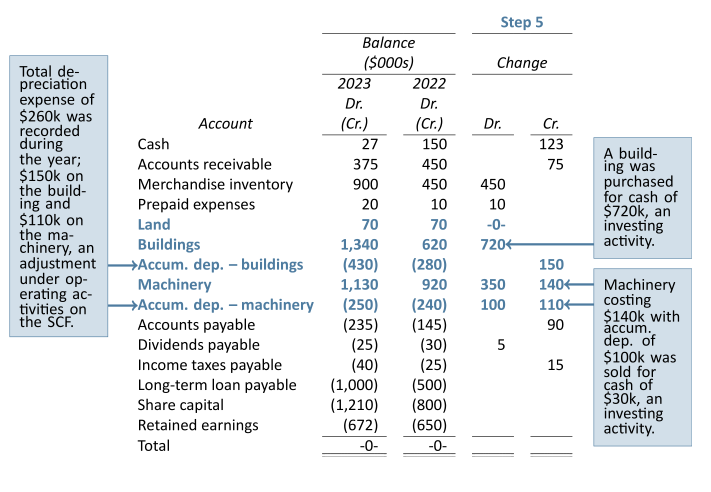

Step 5: Calculate and analyze changes in non-current asset accounts

Changes in non-current assets are classified as investing activities. There was no change in the Land account. We know from the additional information provided that buildings and machinery were purchased and that machinery was sold.

Buildings were purchased for $720 thousand (a debit to buildings and a credit to cash). The cash payment of $720 thousand is shown in the investing activities section (see Figure 11.5).

Accumulated depreciation–buildings is a non-current asset account and it increased by $150 thousand. This change was caused by a debit to depreciation expense and a credit to accumulated depreciation–building. We know from an earlier discussion that depreciation expense is an adjustment in the operating activities section of the SCF therefore the $150 thousand is added in the operating activities section (see Figure 11.5).

Two transactions caused machinery to change. First, the purchase of $350 thousand of machinery (debit machinery and credit cash); the $350 thousand cash payment is shown in the investing activities section (see Figure 11.5). Second, machinery costing $140 thousand with accumulated depreciation of $100 thousand was sold for cash of $30 thousand resulting in a loss of $10 thousand. The cash proceeds of $30 thousand is shown in the investing activities section of the SCF and the $10 thousand loss is added in the operating activities section (see Figure 11.5).

Accumulated depreciation–machinery not only decreased $100 thousand because of the sale of machinery but it increased by $110 thousand because of depreciation (debit depreciation expense and credit accumulated depreciation–machinery). The $110 thousand of depreciation expense is added in the operating activities section of the SCF (see Figure 11.5).

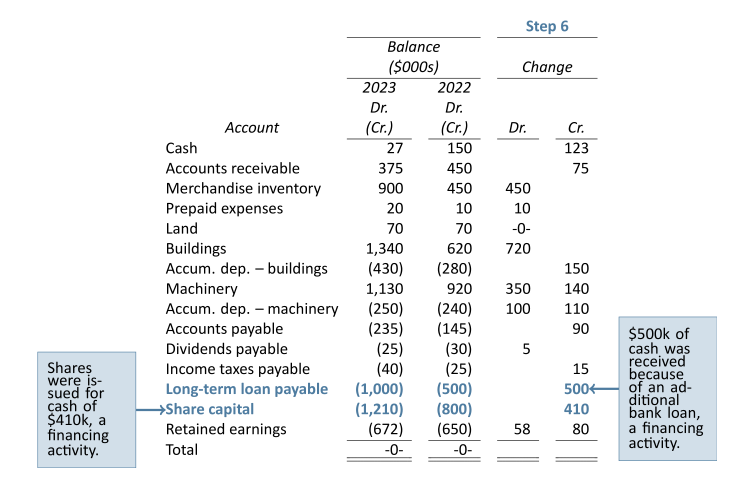

Step 6: Calculate and analyze changes in Long-term Liability and Share Capital accounts

Changes in Long-term Liability and Share Capital accounts result from financing activities. We know from the additional information provided earlier that Example Corporation received cash of $500k from a bank loan (debit cash and credit long-term loan payable) and issued shares for $410k cash (debit cash and credit share capital). The $500 thousand cash proceeds from the bank loan and $410 thousand cash proceeds from the issuance of shares are listed in the financing section of the SCF (see Figure 11.5).

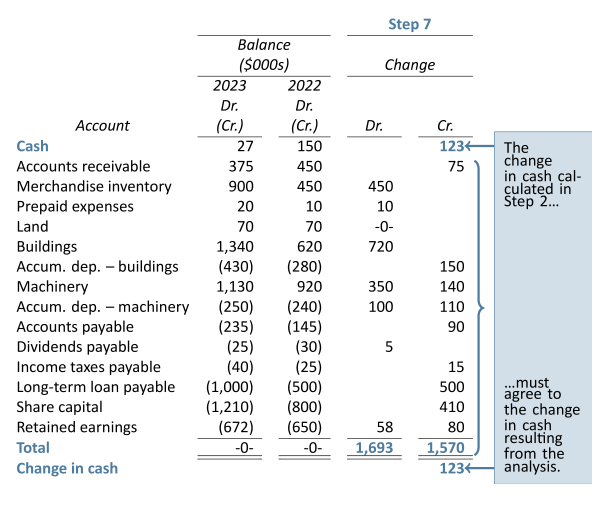

Step 7: Reconcile the analysis

The analysis is now complete. Add the debit and credit changes, excluding the change in cash. The total debits of $1,693 less the total credits of $1,570 equal a difference of $123 which reconciles to the decrease in cash calculated in Step 2.

The information in the completed analysis can be used to prepare the statement of cash flows shown in Figure 11.5.

| Example Corporation | |||

| Statement of Cash Flows | |||

| For the Year Ended December 31, 2023 | |||

| ($000s) | |||

| Cash flows from operating activities: | |||

| Net income | $ | 80 | |

| Adjustments to reconcile net income | |||

| cash provided by operating activities: | |||

| Decrease in accounts receivable | 75 | ||

| Increase in merchandise inventory | (450) | ||

| Increase in prepaid expenses | (10) | ||

| Increase in accounts payable | 90 | ||

| Increase in income taxes payable | 15 | ||

| Depreciation expense | 260 | ||

| Loss on disposal of machinery | 10 | ||

| Net cash inflow from operating activities | $ | 70 | |

| Cash flows from investing activities: | |||

| Proceeds from sale of machinery | 30 | ||

| Purchase of building | (720) | ||

| Purchase of machinery | (350) | ||

| Net cash outflow from investing activities | (1,040) | ||

| Cash flows from financing activities: | |||

| Payment of dividends | (63) | ||

| Proceeds from bank loan | 500 | ||

| Issuance of shares | 410 | ||

| Net cash inflow from financing activities | 847 | ||

| Net decrease in cash | $ | (123) | |

| Cash at beginning of year | 150 | ||

| Cash at end of year | $ | 27 | |