3.14.1: Financial Planning

- Page ID

- 58891

Learning Objectives

- Define personal finances and financial planning.

- Explain the financial planning life cycle.

- Discuss the advantages of a college education in meeting short- and long-term financial goals.

- Describe the steps you’d take to get a job offer and evaluate alternative job offers, taking benefits into account.

- Understand the ways to finance a college education.

Before we go any further, we need to nail down a couple of key concepts. First, just what, exactly, do we mean by personal finances? Finance itself concerns the flow of money from one place to another, and your personal finances concern your money and what you plan to do with it as it flows in and out of your possession. Essentially, then, personal finance is the application of financial principles to the monetary decisions that you make either for your individual benefit or for that of your family.

Second, as we suggested in Section 14—and as we’ll insist in the rest of it—monetary decisions work out much more beneficially when they’re planned rather than improvised. Thus our emphasis on financial planning—the ongoing process of managing your personal finances in order to meet goals that you’ve set for yourself or your family.

Financial planning requires you to address several questions, some of them relatively simple:

- What’s my annual income?

- How much debt do I have, and what are my monthly payments on that debt?

Others will require some investigation and calculation:

- What’s the value of my assets?

- How can I best budget my annual income?

Still others will require some forethought and forecasting:

- How much wealth can I expect to accumulate during my working lifetime?

- How much money will I need when I retire?

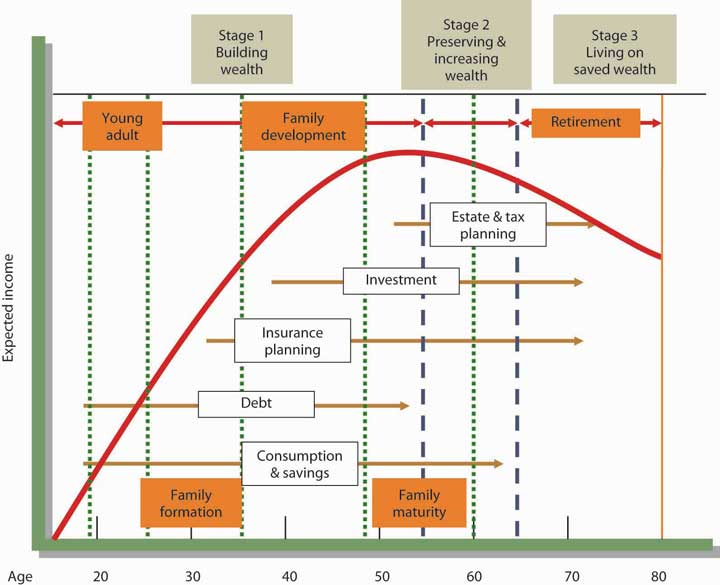

The Financial Planning Life Cycle

Another question that you might ask yourself—and certainly would do if you were a professional in financial planning—is something like, “How will my financial plans change over the course of my life?” Figure 14.3 “Financial Life Cycle” illustrates the financial life cycle of a typical individual—one whose financial outlook and likely outcomes are probably a lot like yours (Keown, 2007). As you can see, our diagram divides this individual’s life into three stages, each of which is characterized by different life events (such as beginning a family, buying a home, planning an estate, retiring). At each stage, too, there are recommended changes in the focus of the individual’s financial planning:

Figure 14.3 Financial Life Cycle

At each stage, of course, complications can set in—say, changes in such conditions as marital or employment status or in the overall economic outlook. Finally, as you can also see, your financial needs will probably peak somewhere in stage 2, at approximately age fifty-five, or ten years before typical retirement age.

- In stage 1, the focus is on building wealth.

- In stage 2, the focus shifts to the process of preserving and increasing the wealth that one has accumulated and continues to accumulate.

- In stage 3, the focus turns to the process of living on (and, if possible, continuing to grow) one’s saved wealth.

Choosing a Career

Until you’re eighteen or so, you probably won’t generate much income; for the most part, you’ll be living off your parents’ wealth. In our hypothetical life cycle, however, financial planning begins in the individual’s early twenties. If that seems like rushing things, consider a basic fact of life: this is the age at which you’ll be choosing your career—not only the sort of work you want to do during your prime income-generating years, but also the kind of lifestyle you want to live in the process (Keown, 2007).

What about college? Most readers of this book, of course, have decided to go to college. If you haven’t yet decided, you need to know that college is an extremely good investment of both money and time.

Table 14.1 “Education and Average Income”, for example, summarizes the findings of a study conducted by the U.S. Census Bureau (U.S. Census Bureau, 2008). A quick review shows that people who graduate from high school can expect to increase their average annual earnings by about 49 percent over those of people who don’t, and those who go on to finish college can expect to generate 82 percent more annual income than that. Over the course of the financial life cycle, families headed by those college graduates will earn about $1.6 million more than families headed by high school graduates who didn’t attend college. (With better access to health care—and, studies show, with better dietary and health practices—college graduates will also live longer. And so will their children.) (U.S. Census Bureau, 2008)

| Education | Average income | Percentage increase over next-highest level |

|---|---|---|

| High school dropout | $20,873 | — |

| High school diploma | $31,071 | 48.9% |

| College degree | $56,788 | 82.8% |

| Advanced higher-education degree | $82,320 | 45.0% |

And what about the debt that so many people accumulate to finish college? For every $1 that you spend on your college education, you can expect to earn about $35 during the course of your financial life cycle (Hansen, 2008). At that rate of return, you should be able to pay off your student loans (unless, of course, you fail to practice reasonable financial planning).

Naturally, there are exceptions to these average outcomes. You’ll find English-lit majors stocking shelves at 7-Eleven, and you’ll find college dropouts running multibillion-dollar enterprises. Microsoft cofounder Bill Gates dropped out of college after two years, as did his founding partner, Paul Allen. Current Microsoft CEO Steve Ballmer finished his undergraduate degree but quit his MBA program to join Microsoft (where he apparently fit in among the other dropouts in top management). It’s always good to remember, however, that though exceptions to rules (and average outcomes) occasionally modify the rules, they invariably fall far short of disproving them: in entrepreneurship as in most other walks of adult life, the better your education, the more promising your financial future. One expert in the field puts the case for the average person bluntly: educational credentials “are about being employable, becoming a legitimate candidate for a job with a future. They are about climbing out of the dead-end job market” (Ramsay, 2008).

Finally, does it make any difference what you study in college? To a perhaps surprising extent, not necessarily. Some career areas, such as engineering, architecture, teaching, and law, require targeted degrees, but the area of study designated on your degree often doesn’t matter much when you’re applying for a job. If, for instance, a job ad says, “Business, communications, or other degree required,” most applicants and hires will have those “other” degrees. When poring over résumés for a lot of jobs, potential employers look for the degree and simply note that a candidate has one; they often don’t need to focus on the particulars (Roth, 2008).

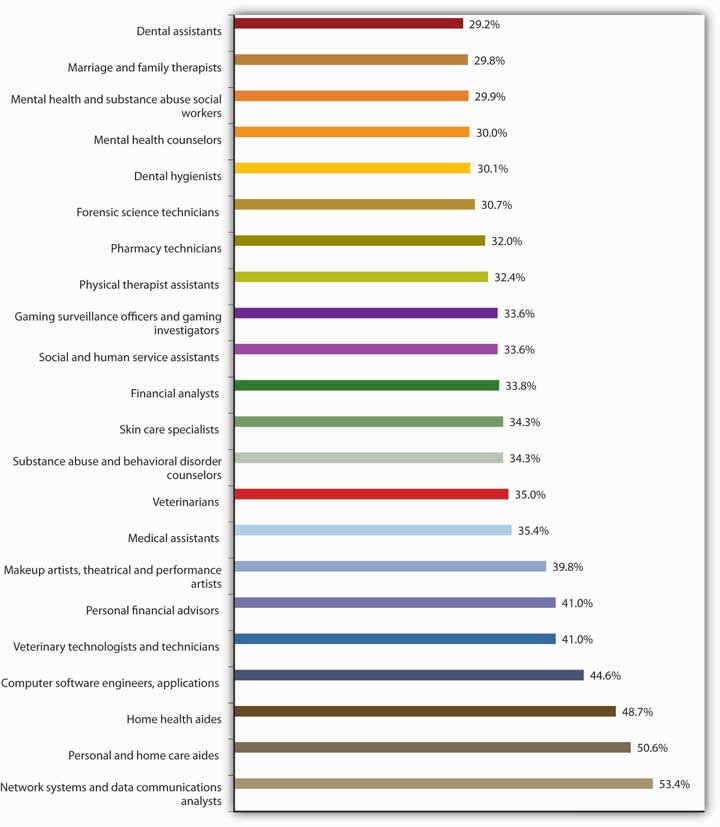

This is not to say, however, that all degrees promise equal job prospects. Figure 14.4 “Top 25 Fastest-Growing Jobs, 2006–2016”, for example, summarizes a U.S. Bureau of Labor Statistics projection of the thirty fast-growing occupations for the years 2006–2016. Veterinary technicians and makeup artists will be in demand as never before, but as you can see, occupational prospects are fairly diverse1.

Figure 14.4 Top 25 Fastest-Growing Jobs, 2006–2016

Nor, of course, do all degrees pay off equally. In Table 14.2 “College Majors and Average Annual Earnings”, we’ve extracted the findings of a study conducted by the National Science Foundation on the earnings of individuals with degrees in various undergraduate fields (Penrice, 1999; Harrington & Sum, 2011). Clearly, some degrees—notably in the engineering fields—promise much higher average earnings than others. Chemical engineers, for instance, can earn nearly twice as much as elementary school teachers, but there’s a catch: if you graduate with a degree in chemical engineering, your average annual salary will be about $67,000 if you can find a job related to that degree; if you can’t, you may have to settle for as much as 40 percent less (Penrice, 1999). (Supermodel Cindy Crawford cut short her studies in chemical engineering because there was more money to be made on the runway.)

| Major | Average Earnings with Bachelor’s Degree | Major | Average Earnings with Bachelor’s Degree |

|---|---|---|---|

| Chemical engineering | $67,425 | History | $45,926 |

| Aerospace engineering | $65,649 | Biology | $45,532 |

| Computer engineering | $62,527 | Nursing | $45,538 |

| Physics | $62,104 | Psychology | $43,963 |

| Electrical engineering | $61,534 | English | $43,614 |

| Mechanical engineering | $61,382 | Health technology | $42,524 |

| Industrial engineering | $61,030 | Criminal justice | $41,129 |

| Civil engineering | $58,993 | Physical education | $40,207 |

| Accounting | $56,637 | Secondary education | $39,976 |

| Finance | $55,104 | Fine arts | $38,857 |

| Computer science | $52,615 | Philosophy | $38,239 |

| Business management | $52,321 | Dramatic arts | $37,091 |

| Marketing | $51,107 | Music | $36,811 |

| Journalism | $46,835 | Elementary education | $34,564 |

| Information systems | $46,519 | Special education | $34,196 |

In short, when you’re planning what to do with the rest of your life, it’s a good idea to check into the fine points and realities, as well as the statistical data. If you talk to career counselors and people in the workforce, you might be surprised by what you learn about the relationship between certain college majors and various occupations. Onetime Hewlett-Packard CEO Carly Fiorina majored in medieval history and philosophy.