15.2: Financial and Nonfinancial Controls

- Page ID

- 47824

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)- Explain the use of budgets to both control and delegate authority.

- Explain the use of financial ratios (comparisons) as a control method.

- Explain the benefits of quality management.

- Explain the costs of quality management.

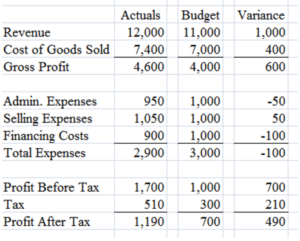

Budgetary Control

The standard financial reports are the statement of cash flows, the balance sheet, the income statement, financial ratios, and budgets. For most large companies, the first three are required by law. Stockholders need to know how their company is doing. Financial ratios help in investing decisions and in managing the company. They are common but not legally required. Budgets are internal plans, which the company does not typically disclose.

A budget sets a limit on spending and thus is a method of control used to help organizations achieve goals. The budget may be single number setting a manager’s spending limit or a plan with limits for detailed items. Departments and the whole organization will develop budgets both for planning and control.

To follow a budget requires discipline. When an expense or desirable pops up, managers must prioritize purchases to stay within budget. In this sense, budgets help control spending and ensure that goals are reached by allocating money to the places where it is needed. Without this planned allocation of resources, there is the risk of spending too much money in one or a few areas, thereby not having enough for other areas.

Budgets can also be used to delegate authority. When an executive assigns a task to a subordinate, the executive needs to release the funds in order for the employee to complete the task. In releasing the funds with an assigned budget, the executive delegates the authority to make decisions regarding the proper use of the funds. The executive can use the budget as a means of monitoring and measuring the performance of the subordinate. With this means of control, the executive may feel comfortable with delegating authority.

Financial Ratios

When people think of management, they often visualize a person giving orders, hiring employees, checking the work of employees, establishing policies, and administering discipline. However, watching the numbers is also an important activity in management. The numbers can be converted to financial ratios, which allow easy comparisons.

Managers use ratios to analyze elements such as debt, equity, efficiency, and activity. For example, a debt ratio compares an organization’s debt to its assets. It is calculated as total liabilities divided by total assets. The higher the ratio, the more leveraged the company is. If a company has a high debt ratio (relative to its industry), the company has to spend a significant portion of its cash flow on bills.

The key to understanding ratios is comparing them to relevant benchmarks. The debt ratio for a manufacturing company might typically be 50 percent, meaning debt funds half of the assets. In a bank the typical debt ratio is around 92 percent. The relevant benchmark for a bank is the banking industry average or another bank, not a manufacturer.

Analyzing financial ratios can help managers determine the financial health of the company. Knowing the state of the company in various areas (e.g., inventory, equity, and debt) allows managers to make the changes needed to course-correct and to reach goals.

Quality Management

Have you ever bought a product that was defective? Have you ever been served by a company representative in such a way that it made you want to tell people what a great company it is or give the company five-star ratings on social media? In both cases, quality management was behind the scenes of your customer experience.

Quality management involves controlling, monitoring, and modifying tasks to maintain a desired level of quality or excellence. At the core of quality management is customer satisfaction. Companies pursue the level of quality for their products and services that customers expect and desire. Managers strive to know what customers want, and they manage operations in such a way as to fulfill those desires. Total Quality Management (TQM) and Six Sigma are well-known programs for managing quality.

Benefits

Quality management helps companies please their customers. When customers are pleased, a company can thrive. A simple example of quality management is part inspection. When a part comes down the production line and is complete, an inspector, or quality-assurance technician, checks and tests the part to ensure that it meets quality standards. If it does not, the part is discarded. Thus, quality management helps to ensure that customers are not disappointed so that a company can maintain a good reputation, gain a competitive edge, and ultimately make a profit.

By reducing defects, companies save both time and money. There are fewer returns from customers, and customers are more loyal, reducing the need and cost of acquiring new customers. By catching mistakes early, the production process is not tied up with damaged materials. The final output of acceptable goods increases.

The Systems Sciences Institute at IBM has reported that the cost to fix an error found during beta testing was 15 times as much as one uncovered during design. If the same error was released, the cost to fix the error was up to 100 times more during the maintenance period.[1]

Costs

Regulations are a type of control that society puts on companies. For some large banks, the cost of complying with regulations averages about $12 billion per year.[2] That is a hefty control cost until you consider the cost of control failure. Financial losses in the Great Recession were $10 trillion to $12 trillion![3]

A focus on customers often drives managers to great lengths to please customers. In doing so, quality management can become expensive. Typically, companies need to purchase new software and equipment, hire and train employees, conduct studies, and consult with experts to improve the quality of its products and services. These activities add to the cost of doing business. Management must weigh the costs and benefits.

The following video explains the role TQM plays in an organization as a whole:

- Maurice Dawson, Darrell Burrell, Emad Rahim, and Stephen Brewster, “Integrating Software Assurance in the Software Development Life Cycle (SDLC),” Journal of Information Systems Technology & Planning, 3, no. 6 (2010): 49–53. https://www.researchgate.net/publication/255965523_Integrating_Software_Assurance_into_the_Software_Development_Life_Cycle_SDLC. ↵

- Saabira Chaudhuri, “The Cost of New Banking Regulation: $70.2 Billion,” Moneybeat (blog), Wall Street Journal, July 30, 2014, https://blogs.wsj.com/moneybeat/2014/07/30/the-cost-of-new-banking-regulation-70-2-billion/↵

- Eduardo Porter, “Recession’s True Cost Is Still Being Tallied,” Economic Scene, New York Times, January 21, 2014, https://www.nytimes.com/2014/01/22/business/economy/the-cost-of-the-financial-crisis-is-still-being-tallied.html↵

Contributors and Attributions

- Financial and Nonfinancial Controls. Authored by: Talia Lambarki and Lumen Learning. License: CC BY: Attribution

- Image: Budget. Authored by: Robert Carroll and Lumen Learning. License: CC BY: Attribution