9.1: Price Defined - Three different Perspective

- Page ID

- 21385

Although making the pricing decision is usually a marketing decision, making it correctly requires an understanding of both the customer and society's view of price as well. In some respects, price setting is the most important decision made by a business. A price set too low may result in a deficiency in revenues and the demise of the business. A price set too high may result in poor response from customers and, unsurprisingly, the demise of the business. The consequences of a poor pricing decision, therefore, can be dire. We begin our discussion of pricing by considering the perspective of the customer.

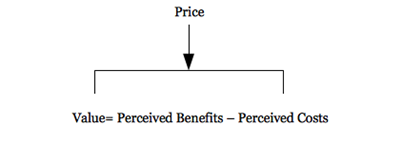

Exhibit 28: The customer's view of price

Exhibit 28: The customer's view of price

The customer's view of price

As discussed in an earlier chapter, a customer can be either the ultimate user of the finished product or a business that purchases components of the finished product. It is the customer that seeks to satisfy a need or set of needs through the purchase of a particular product or set of products. Consequently, the customer uses several criteria to determine how much they are willing to expend in order to satisfy these needs. Ideally, the customer would like to pay as little as possible to satisfy these needs. This perspective is summarized in Exhibit 28.

Therefore, for the business to increase value (i.e. create the competitive advantage), it can either increase the perceived benefits or reduce the perceived costs. Both of these elements should be considered elements of price. To a certain extent, perceived benefits are the mirror image of perceived costs. For example, paying a premium price (e.g. USD 650 for a piece of Lalique crystal) is compensated for by having this exquisite work of art displayed in one's home. Other possible perceived benefits directly related to the price-value equation are status, convenience, the deal, brand, quality, choice, and so forth. Many of these benefits tend to overlap. For instance, a Mercedes Benz E750 is a very high-status brand name and possesses superb quality. This makes it worth the USD 100,000 price tag. Further, if one can negotiate a deal reducing the price by USD 15,000, that would be his incentive to purchase. Likewise, someone living in an isolated mountain community is willing to pay substantially more for groceries at a local store rather than drive 78 miles (25.53 kilometers) to the nearest Safeway. That person is also willing to sacrifice choice for greater convenience. Increasing these perceived benefits is represented by a recently coined term, value-added. Thus, providing value-added elements to the product has become a popular strategic alternative. Computer manufacturers now compete on value-added components such as free delivery setup, training, a 24-hour help line, trade-in, and upgrades.

Perceived costs include the actual dollar amount printed on the product, plus a host of additional factors. As noted, these perceived costs are the mirror-opposite of the benefits. When finding a gas station that is selling its highest grade for USD 0.06 less per gallon, the customer must consider the 16 mile (25.75 kilometer) drive to get there, the long line, the fact that the middle grade is not available, and heavy traffic. Therefore, inconvenience, limited choice, and poor service are possible perceived costs. Other common perceived costs include risk of making a mistake, related costs, lost opportunity, and unexpected consequences, to name but a few. A new cruise traveler discovers he or she really does not enjoy that venue for several reasons–e.g. he or she is given a bill for incidentals when she leaves the ship, has used up her vacation time and money, and receives unwanted materials from this company for years to come.

In the end, viewing price from the customer's perspective pays off in many ways. Most notably, it helps define value–the most important basis for creating a competitive advantage.

Price from a societal perspective

Price, at least in dollars and cents, has been the historical view of value. Derived from a bartering system (exchanging goods of equal value), the monetary system of each society provides a more convenient way to purchase goods and accumulate wealth. Price has also become a variable society employs to control its economic health. Price can be inclusive or exclusive. In many countries, such as Russia, China, and South Africa, high prices for products such as food, health care, housing, and automobiles, means that most of the population is excluded from purchase. In contrast, countries such as Denmark, Germany, and Great Britain charge little for health care and consequently make it available to all.

There are two different ways to look at the role price plays in a society: rational man and irrational man. The former is the primary assumption underlying economic theory, and suggests that the results of price manipulation are predictable. The latter role for price acknowledges that man's response to price is sometimes unpredictable and pretesting price manipulation is a necessary task. Let us discuss each briefly.

Rational man pricing: an economic perspective

Basically, economics assumes that the consumer is a rational decision maker and has perfect information. Therefore, if a price for a particular product goes up and the customer is aware of all relevant information, demand will be reduced for that product. Should price decline, demand would increase. That is, the quantity demanded typically rises causing a downward sloping demand curve.

A demand curve shows the quantity demanded at various price levels (see Exhibit 29). As a seller changes the price requested to a lower level, the product or service may become an attractive use of financial resources to a larger number of buyers, thus expanding the total market for the item. This total market demand by all buyers for a product type (not just for the company's own brand name) is called primary demand. Additionally, a lower price may cause buyers to shift purchases from competitors, assuming that the competitors do not meet the lower price. If primary demand does not expand and competitors meet the lower price the result will be lower total revenue for all sellers.

Since, in the US, we operate as a free market economy, there are few instances when someone outside the organization controls a product's price. Even commodity-like products such as air travel, gasoline, and telecommunications, now determine their own prices. Because large companies have economists on staff and buy into the assumptions of economic theory as it relates to price, the classic price-demand relationship dictates the economic health of most societies. The Chairman of the US Federal Reserve determines interest rates charged by banks as well as the money supply, thereby directly affecting price (especially of stocks and bonds). He is considered by many to be the most influential person in the world.

Irrational man pricing: freedom rules

There are simply too many examples to the contrary to believe that the economic assumptions posited under the rational man model are valid. Prices go up and people buy more. Prices go down and people become suspicious and buy less. Sometimes we simply behave in an irrational manner. Clearly, as noted in our earlier discussion on consumers, there are other factors operating in the marketplace. The ability of paying a price few others can afford may be irrational, but it provides important personal status. There are even people who refuse to buy anything on sale. Or, others who buy everything on sale. Often businesses are willing to hire a USD 10,000 consultant, who does no more than a USD 5,000 consultant, simply to show the world they are successful.

In many societies, an additional irrational phenomenon may exist–support of those that cannot pay. In the US, there are literally thousands of not-for-profit organizations that provide goods and services to individuals for very little cost or free. There are also government agencies that do even more. Imagine what giving away surplus food to the needy does to the believers of the economic model.

Pricing planners must be aware of both the rational as well as the irrational model, since, at some level, both are likely operating in a society. Choosing one over the other is neither wise nor necessary.

The marketer's view of price

Price is important to marketers, because it represents marketers' assessment of the value customers see in the product or service and are willing to pay for a product or service. A number of factors have changed the way marketers undertake the pricing of their products and services.1

• Foreign competition has put considerable pressure on US firms' pricing strategies. Many foreign-made products are high in quality and compete in US markets on the basis of lower price for good value.

• Competitors often try to gain market share by reducing their prices. The price reduction is intended to increase demand from customers who are judged to be sensitive to changes in price.

• New products are far more prevalent today than in the past. Pricing a new product can represent a challenge, as there is often no historical basis for pricing new products. If a new product is priced incorrectly, the marketplace will react unfavorably and the "wrong" price can do long-term damage to a product's chances for marketplace success.

• Technology has led to existing products having shorter marketplace lives. New products are introduced to the market more frequently, reducing the "shelf life" of existing products. As a result, marketers face pressures to price products to recover costs more quickly. Prices must be set for early successes including fast sales growth, quick market penetration, and fast recovery of research and development costs.