16.7: Limited Liability Entities

- Page ID

- 49139

A limited liability company (LLC) is a “hybrid” form of business organization that offer the limited liability feature of corporations but the tax benefits of partnerships. Owners of LLCs are called members. Just like a sole proprietorship, it is possible to create an LLC with only one member. LLC members can be individuals or other LLCs, corporations, or partnerships. LLC members can participate in day-to-day management of the business.

Members are not personally liable for the debts of the business. Like shareholders of a corporation, members of an LLC risk only their financial investment in the company.

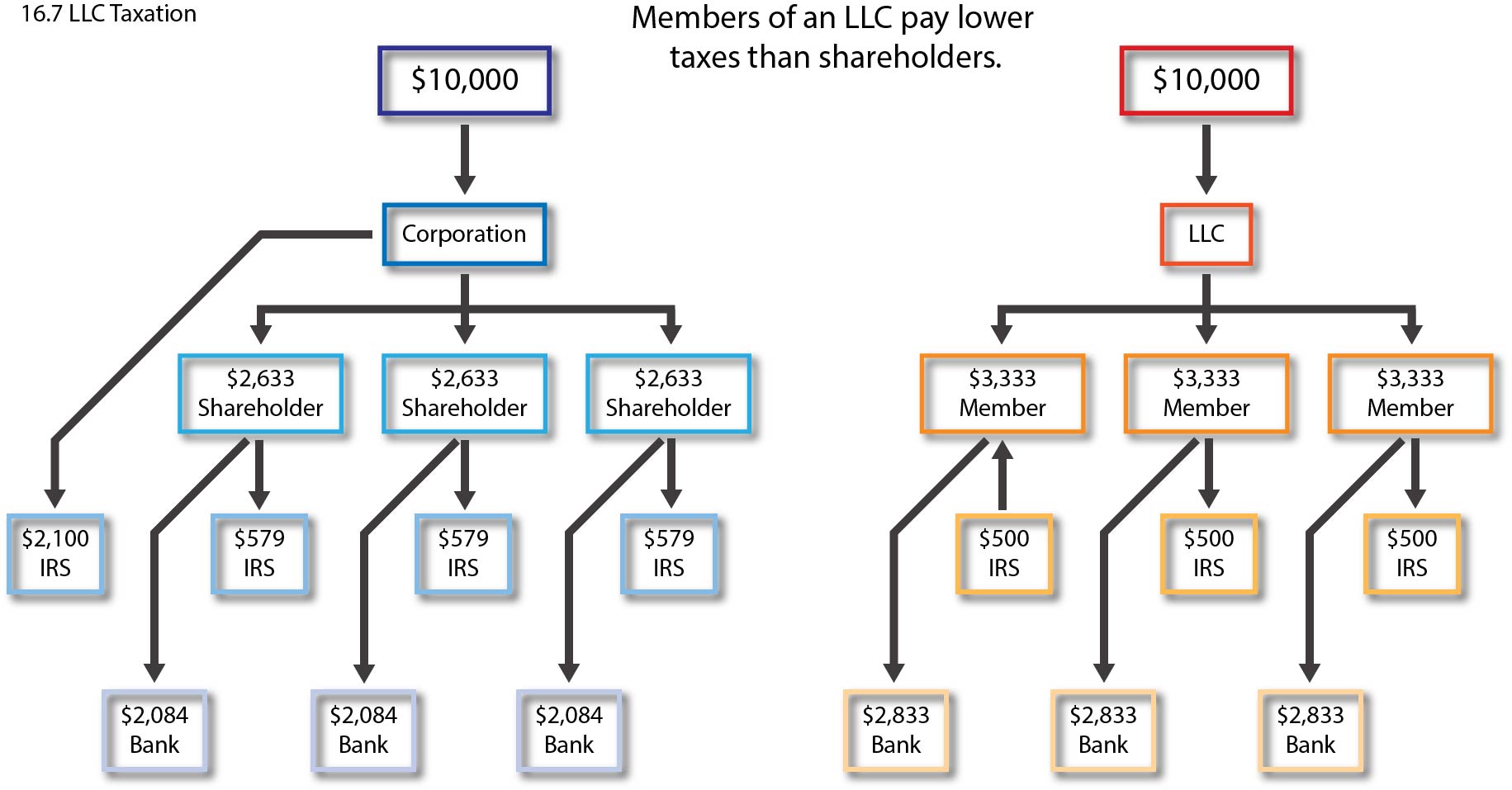

Taxation of LLCs is very flexible. Every year the LLC can choose how it will be taxed. It may want to be taxed as a corporation, for example, and pay corporate income tax on net income. Or it may choose instead to have income “flow through” the corporate form to the member-shareholders, who then pay personal income tax just as in a partnership. Sophisticated tax planning becomes possible with LLCs because tax treatment can vary by year.

Figure 16.1 LLC Taxation

LLCs are formed by filing the articles of organization with the state agency charged with chartering business entities, typically the Secretary of State. Starting an LLC is often easier than starting a corporation. Typical LLC statutes require only the name of the LLC and the contact information for the LLC’s legal agent. Unlike corporations, there is no requirement for an LLC to issue stock certificates, maintain annual filings, elect a board of directors, hold shareholder meetings, appoint officers, or engage in any regular maintenance of the entity. Most states require LLCs to have the letters “LLC” or words “Limited Liability Company” in the official business name.

Although the articles of organization are all that is necessary to start an LLC, it is advisable for the LLC members to enter into a written LLC operating agreement. The operating agreement typically sets forth how the business will be managed and operated. It may also contain a buy/sell agreement just like a partnership agreement. The operating agreement allows members to run their LLCs any way they wish.

Since LLCs are a separate legal entity from their members, members must take care to interact with LLCs at arm’s length, because the risk of piercing the veil exists with LLCs as much as it does with corporations. Fundraising for an LLC can be as difficult as it is for a sole proprietorship, especially in the early stages of an LLC’s business operations. Most lenders require LLC members to personally guarantee any loans the LLC may take out. Finally, LLCs are not the right form for taking a company public and selling stock. Fortunately, it is not difficult to convert an LLC into a corporation, so many start-up business begin as LLCs and eventually convert into corporations prior to their initial public offering (IPO).

| Advantages of LLCs | Disadvantages of LLCs |

|

|

Limited Liability Partnerships

A related entity to the LLC is the limited liability partnership, or LLP. Be careful not to confuse limited liability partnerships with limited partnerships. LLPs are just like LLCs but are designed for professionals who do business as partners. They allow the partnership to pass through income for tax purposes, but retain limited liability for all partners. LLPs are especially popular with doctors, architects, accountants, and lawyers. Most of the major accounting firms have now converted their corporate forms into LLPs.

Professional Corporations

Professional Corporations (PCs) are mostly a legacy form of organization. In other words, before LLCs and LLPs were an option, PCs were the only option available to professionals who wanted limited liability. Some states still require doctors, lawyers, and accountants to organize as a PC.

If a member of a PC commits malpractice, the PC’s assets are at risk along with the personal assets of the member who committed malpractice. However, the personal assets of the non-involved members are not at risk. PCs do not shield individuals from their own malpractice but they offer limited liability to innocent members.

PCs are a separate taxable entity but they are not flow-through entities like partnerships. As a result, taxation of PCs is complicated and a major drawback of this form of business entity.

| Type of Business Organization | Ease of Formation | Funding | Personal Liability for Owners | Taxes | Ease of Transferring Ownership | Perpetual Existence | Dissolution |

| Sole Proprietorship | Very easy | Same as owner | Yes | Flow-through | Must sell entire business | No | When & how owner decides |

| General Partnership | Easy | Partners contribute capital | Yes | Flow-through | Hard | No | Upon death, bankruptcy, agreement, or termination of partnership |

| Limited Partnership | Easy | Partners contribute capital | General partner is personally liable; limited liability for limited partners | Flow-through | Hard | No | Upon death, bankruptcy, agreement, or termination of partnership |

| Corporations | Difficult | Sell stock to raise capital | No | Subject to double taxation | Easy | Yes | By resolution of board of directors, bankruptcy, or court order |

| S Corporations | Difficult | Sell stock to raise capital | No | Taxed only on dividends | Transfer restrictions | Yes | By resolution of board of directors, bankruptcy, or court order |

| Limited Liability Companies (LLCs) | Medium | Members make capital contributions | No | Flow-through | Depends on operating agreement | Varies by state; yes in most states | Upon death, bankruptcy, agreement, or court order |

| Limited Liability Partnerships (LLPs) | Difficult | Members make capital contributions | Non-acting partners have limited liability; state law varies regarding liability of acting partners vs. partnership | Flow-through | Depends on the partnership agreement | Depends on partnership agreement | Upon death, bankruptcy, agreement, or termination of partnership |

| Professional Corporations | Difficult | Members make capital contributions | No | Complex tax issues | Transfer restricted to members of the same profession | Yes, as long as it has shareholders | Upon death, bankruptcy, agreement, or court order |