4.2: Income Statement

- Page ID

- 4260

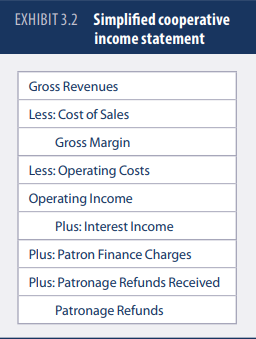

The income statement begins with gross receipts which, for a farm supply or consumer food cooperative or service cooperative, are the sum of all products or services sold by the cooperative multiplied by their respective prices. In the case of a marketing or pooling cooperative, this is the sum of all products bought from the members and sold at the competitive market price. For a processing cooperative, this is the total sales from, for example, selling corn-ethanol and its co-products or soybean meal and its co-products. Gross receipts was traditionally used because it denoted receipt of value of sales done with members. Many cooperatives have moved to a more traditional language, referring to these as gross revenues or total sales. Costs of Goods Sold or Costs of Sales are variable costs and subtracted from these gross receipts.

For a farm supply cooperative these variable expenses include the costs of buying raw material products such as crop nutrients, seed, and crop protectants; energy products such as refined fuels and propane; raw material inputs such as corn to manufacture animal nutrition products; and the technology and labor needed to provide services associated with these products. An electrical utility cooperative has similar costs in purchasing electricity and supplying that electricity, whereas a consumer food cooperative has variable costs in purchasing food products and merchandising that food to members. Note that the conversion of these raw material inputs into a product purchased by producers and consumers is a production function or technology.

The difference between the gross receipts and these variable costs is often called Gross Margin or Gross Profit Margin. Virtually all cooperatives develop a pricing strategy based on operating at a fixed margin per unit because they are “price takers,” so the Gross Margin is an important measure to understand, and it does not change regardless of changes in input or output prices, which change the value of total sales. Operating costs, which are fixed in nature, must be subtracted from this margin. These costs are typically selling and administrative costs, which are typically salaried employees(with benefits) whose wages cannot be attributed directly to the product or technology sold by the cooperative. These costs also include purchase of new assets such as equipment.

The difference between Gross Margin and Operating Expenses is Operating Income, which includes interest income received by the cooperative, finance charges from operating loans made to members (Patron Finance Charges), and any other expenses or revenues received by the cooperative. Cooperatives often do business with other cooperatives and receive Patronage Refunds as income. The difference between these items and Operating Income is called Patronage Refunds. Sometimes the phrase net savings, net margin, net proceeds, or net surplus is used to denote any income left over after the cooperative has received all of its revenues in that year and paid all of its costs in that year. The correct terminology, however, is Patronage Refunds, also called patronage dividends, which are amounts paid to patrons from the net income of the cooperative on the basis of quantity or value of business done with these members. These refunds can be made in cash or retained as equity in the cooperative.