2.5: Adjusting Entries—Accruals

- Page ID

- 43067

Accrue means “to grow over time” or “accumulate.” Accruals are adjusting entries that record transactions in progress that otherwise would not be recorded because they are not yet complete. Because they are still in progress, but no journal entry has been made yet. Adjusting entries are made to ensure that the part that has occurred during a particular month appears on that same month’s financial statements.

2.5.1 Accrued Expenses

Accrued expenses require adjusting entries. In this case someone is already performing a service for you but you have not paid them or recorded any journal entry yet. The transaction is in progress, and the expense is building up (like a “tab”), but nothing has been written down yet. This may occur with employee wages, property taxes, and interest—what you owe is growing over time, but you typically don’t record a journal entry until you incur the full expense. However, if the end of an accounting period arrives before you record any of these growing expenses, you will make an adjusting entry to include the part of the expense that belongs in that period and on that period’s financial statements. For the adjusting entry, you debit the appropriate expense account for the amount you owe through the end of the accounting period so this expense appears on your income statement. You credit an appropriate payable, or liability account, to indicate on your balance sheet that you owe this amount.

These are the three adjusting entries for accrued expenses we will cover.

| Date | Account | Debit | Credit | ||

| 6/30 | Wages Expense | 100 | ▲ Wages Expense is an expense account that is increasing. | ||

| Wages Payable | 100 | ▲ Wages Payable is a liability account that is increasing. | |||

| 6/30 | Taxes Expense | 100 | ▲ Taxes Expense is an expense account that is increasing. | ||

| Taxes Payable | 100 | ▲ Taxes Payable is a liability account that is increasing. | |||

| 6/30 | Interest Expense | 100 | ▲ Interest Expense is an expense account that is increasing. | ||

| Interest Payable | 100 | ▲ Interest Payable is a liability account that is increasing. |

Wages - Accrued Expense

Wages are payments to employees for work they perform on an hourly basis.

General journal entry: A company pays employees $1,000 every Friday for a five-day work week.

| Date | Account | Debit | Credit | ||

| 6/5 | Wages Expense | 1,000 | ▲ Wages Expense is an expense account that is increasing. | ||

| Cash | 1,000 | ▼ Cash is an asset account that is decreasing. |

Here is the Wages Expense ledger where transaction above is posted. Assume the transaction above was recorded four times for each Friday in June. The $4,000 balance in the Wages Expense account will appear on the income statement at the end of the month.

| Date | Item | Debit | Credit | Debit | Credit |

| 6/5 | 1,000 | 1,000 | |||

| 6/12 | 1,000 | 2,000 | |||

| 6/19 | 1,000 | 3,000 | |||

| 6/26 | 1,000 | 4,000 | |||

An expense is a cost of doing business, and it cost $4,000 in wages this month to run the business.

Adjusting journal entry: Assume that June 30, the last day of the month, is a Tuesday. The Friday after, when the company will pay employees next, is July 3. Employees earn $1,000 per week, or $200 per day. Therefore, for this week, $400 of the $1,000 for the week should be a June expense and the other $600 should be a July expense.

An adjusting entry is required on June 30 so that the wages expense incurred on June 29 and June 30 appears on the June income statement. This entry splits the wages expense for that week: two days belong in June, and the other three days belong in July. Wages Expense is debited on 6/30, but Cash cannot be credited since 6/30 is a Tuesday and employees will not be paid until Friday. New liability account: Wages Payable.

| Date | Account | Debit | Credit | ||

| 6/30 | Wages Expense | 400 | ▲ Wages Expense is an expense account that is increasing. | ||

| Wages Payable | 400 | ▲ Wages Payable is a liability account that is increasing. |

Here are the Wages Payable and Wages Expense ledgers AFTER the adjusting entry has been posted.

| Wages Payable | Wages Expense | |||||||||||

| Date | Item | Debit | Credit | Debit | Credit | Date | Item | Debit | Credit | Debit | Credit | |

| 6/30 | 400 | 400 | 6/5 | 1,000 | 1,000 | |||||||

| 6/12 | 1,000 | 2,000 | ||||||||||

| 6/19 | 1,000 | 3,000 | ||||||||||

| 6/26 | 1,000 | 4,000 | ||||||||||

| 6/30 | 400 | 4,400 | ||||||||||

The adjusting entry for an accrued expense updates the Wages Expense and Wages Payable balances so they are accurate at the end of the month. The adjusting entry is journalized and posted BEFORE financial statements areprepared so that the company’s income statement and balance sheet show the correct, up-to-date amounts.

Summary

The company had already accumulated $4,000 in Wages Expense during June -- $1,000 for each of four weeks. For the two additional work days in June, the 29th and 30th, the company accrued $400 additional in Wages Expense. To add this additional amount so it appears on the June income statement, Wages Expense was debited. Wages Payable was credited and will appear on the balance sheet to show that this $400 is owed to employees for unpaid work in June.

IMPORTANT: If this journal entry had been omitted, many errors on the financial statements would result.

- The Wages Expense amount on the income statement would have been too low ($4,000 instead of $4,400).

2.Net income on the income statement would have been too high (An additional $400 of Wages Expense should have been deducted from revenues but was not).

- The Wages Payable amount on the balance sheet would have been too low ($0 instead of $400).

- The total liabilities amount on the balance sheet would have been too low because Wages Payable, one liability, was too low.

- The total stockholders’ equity amount on the balance sheet would be too high because a net income amount that was too high would have been closed out to Retained Earnings.

| Date | Account | Debit | Credit | ||

| 7/3 | Wages Expense | 600 | ▲ Wages Expense is an expense account that is increasing. | ||

| Wages Payable | 400 | ▼ Wages Payable is a liability account that is decreasing. | |||

| Cash | 1,000 | ▼ Cash is an asset account that is decreasing. |

Here are the Wages Payable and Wages Expense ledgers AFTER the closing entry (not shown) and the 7/3 entry have been posted.

| Wages Payable | Wages Expense | |||||||||||

| Date | Item | Debit | Credit | Debit | Credit | Date | Item | Debit | Credit | Debit | Credit | |

| 6/30 | 400 | 400 | 6/5 | 1,000 | 1,000 | |||||||

| 7/3 | 400 | 0 | 6/12 | 1,000 | 2,000 | |||||||

| 6/19 | 1,000 | 3,000 | ||||||||||

| 6/26 | 1,000 | 4,000 | ||||||||||

| 6/30 | 400 | 4,400 | ||||||||||

| 6/30 | 4,400 | 0 | ||||||||||

| 7/3 | 600 | 600 | ||||||||||

The $1,000 wages for the week beginning June 29th is split over two months in the Wages Expense accounts: $400 in June, and $600 in July.

Wages Payable has a zero balance on 7/3 since nothing is owed to employees for the week now that they have been paid the $1,000 in cash.

Taxes - Accrued Expense

Property taxes are paid to the county in which a business operates and are levied on real estate and other assets a business owns. Typically the business operates for a year and pays its annual property taxes at the end of that year. At the beginning of the year, the company does have an estimate of what its total property tax bill will be at the end of the year.

Assume that a company’s annual (January 1 to December 31) property taxes are estimated to be $6,000.

If the company prepares 12 monthly financial statements during the year, 1/12 of this estimate, or $500, should be included on each month’s statements since this expense is accruing over time. New liability account: Taxes Payable.

No journal entry is made at the beginning of each month. At the end of each month, $500 of taxes expense has accumulated/accrued for the month. At the end of January, no property tax will be paid since payment for the entire year is due at the end of the year. However, $500 is now owed.

| Date | Account | Debit | Credit | ||

| 1/31 | Taxes Expense | 500 | ▲ Taxes Expense is an expense account that is increasing. | ||

| Taxes Payable | 500 | ▲ Taxes Payable is a liability account that is increasing. |

Here are the Taxes Payable and Taxes Expense ledgers AFTER the adjusting entry has been posted.

| Date | Item | Debit | Credit | Debit | Credit | Date | Item | Debit | Credit | Debit | Credit | |

| 1/31 | 500 | 500 | 1/31 | 500 | 500 | |||||||

This recognizes that 1/12 of the annual property tax amount is now owed at the end of January and includes 1/12 of this annual expense amount on January’s income statement.

The same adjusting entry above will be made at the end of the month for 12 months to bring the Taxes Payable amount up by $500 each month. Here is an example of the Taxes Payable account balance at the end of December.

When the bill is paid on 12/31, Taxes Payable is debited and Cash is credited for $6,000. The Taxes Payable balance becomes zero since the annual taxes have been paid.

| Date | Item | Debit | Credit | Debit | Credit |

| 1/31 | 500 | 500 | |||

| 2/28 | 500 | 1,000 | |||

| 3/31 | 500 | 1,500 | |||

| 4/30 | 500 | 2,000 | |||

| 5/31 | 500 | 2,500 | |||

| 6/30 | 500 | 3,000 | |||

| 7/31 | 500 | 3,500 | |||

| 8/31 | 500 | 4,000 | |||

| 9/30 | 500 | 4,500 | |||

| 10/31 | 500 | 5,000 | |||

| 11/30 | 500 | 5,500 | |||

| 12/31 | 500 | 6,000 | |||

| 12/31 | 6,000 | 0 |

The adjusting entry for an accrued expense updates the Taxes Expense and Taxes Payable balances so they are accurate at the end of the month. The adjusting entry is journalized and posted BEFORE financial statements areprepared so that the company’s income statement and balance sheet show the correct, up-to-date amounts.

Summary

Some expenses accrue over time and are paid at the end of a year. When this is the case, an estimated amount is applied to each month in the year so that each month reports a proportionate share of the annual cost.

IMPORTANT: If this journal entry had been omitted, many errors on the financial statements would result.

- The Taxes Expense amount on the income statement would have been too low ($0 instead of $500).

- Net income on the income statement would have been too high (Taxes Expense should have been deducted from revenues but was not).

- The Taxes Payable amount on the balance sheet would have been too low ($0 instead of $500).

- The total liabilities amount on the balance sheet would have been too low because Taxes Payable, one liability, was too low.

- The total stockholders’ equity amount on the balance sheet would be too high because a net income amount that was too high would have been closed out to Retained Earnings.

2.5.2 Accrued Revenue

Accrued revenues require adjusting entries. “Accrued” means “accumulated over time.” In this case a customer will only pay you well after you complete a job that extends more than one accounting period. At the end of each accounting period, you record the part of the job that you did complete as a sale. This involves a debit to Accounts Receivable to acknowledge that the customer owes you for what you have completed and a credit to Fees Earned to record the revenue earned thus far.

Fees Earned - Accrued Revenue

Revenue is earned as a job is performed. Sometimes an entire job is not completed within the accounting period, and the company will not bill the customer until the job is completed. The earnings from the part of the job that has been completed must be reported on the month’s income statement for this accrued revenue, and an adjusting entry is required.

Assume that a company begins a job for a customer on June 1. It will take two full months to complete the job. When it is complete, the company will then bill the customer for the full price of $4,000.

No journal entry is made at the beginning of June when the job is started. At the end of each month, the amount that has been earned during the month must be reported on the income statement. If the company earned $2,500 of the $4,000 in June, it must journalize this amount in an adjusting entry.

| Date | Account | Debit | Credit | ||

| 6/30 | Accounts Receivable | 2,500 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Fees Earned | 2,500 | ▲ Fees Earned is a revenue account that is increasing. |

Here are the Accounts Receivable and Fees Earned ledgers AFTER the adjusting entry has been posted.

| Accounts Receivable | Fees Earned | |||||||||||

| Date | Item | Debit | Credit | Debit | Credit | Date | Item | Debit | Credit | Debit | Credit | |

| 6/1 | 500 | 500 | 6/1 | 500 | 500 | |||||||

| 6/10 | 700 | 1,200 | 6/10 | 700 | 1,200 | |||||||

| 6/15 | 500 | 700 | 6/15 | 800 | 2,000 | |||||||

| 6/20 | 1,000 | 1,700 | 6/20 | 1,000 | 3,000 | |||||||

| 6/25 | 700 | 1,000 | 6/25 | 600 | 3,600 | |||||||

| 6/30 | 2,500 | 3,500 | 6/30 | 2,500 | 6,100 | |||||||

Before the adjusting entry, Accounts Receivable had a debit balance of $1,000 and Fees Earned had a credit balance of $3,600. These balances were the result of other transactions during the month. When the accrued revenue from the additional unfinished job is added, Accounts Receivable has a debit balance of $3,500 and Fees Earned had a credit balance of $5,100 on 6/30. These final amounts are what appears on the financial statements.

The adjusting entry for accrued revenue updates the Accounts Receivable and Fees Earned balances so they are accurate at the end of the month. The adjusting entry is journalized and posted BEFORE financial statements areprepared so that the company’s income statement and balance sheet show the correct, up-to-date amounts.

Summary

Some revenue accrues over time and is earned over more than one accounting period. When this is the case, the amount earned must be split over the months involved in completing the job based on when the work is done.

IMPORTANT: If this journal entry had been omitted, many errors on the financial statements would result.

- The Fees Earned amount on the income statement would have been too low ($3,600 instead of $5,100).

- Net income on the income statement would have been too low (The additional Fees Earned should have been included but was not).

- The Accounts Receivable amount on the balance sheet would have been too low ($1,000 instead of $3,500).

- The total assets amount on the balance sheet would have been too low because Accounts Receivable, one asset, was too low.

- The total stockholders’ equity amount on the balance sheet would be too low because a net income amount that was too low would have been closed out to Retained Earnings.

Accounts Summary Table - The following table summarizes the rules of debit and credit and other facts about all of the accounts that you know so far, including those needed for adjusting entries.

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Asset |

Cash |

debit | credit | debit |

Balance |

NO |

| Contra Asset | Accumulated Depreciation | credit | debit | credit | Balance Sheet | NO |

| Liability |

Accounts Payable |

credit | debit | credit |

Balance |

NO |

| Stockholders’ Equity |

Common Stock |

credit | debit | credit | Balance Sheet | NO |

| Revenue |

Fees Earned |

credit | debit | credit | Income Statement | YES |

| Expense |

Wages Expense |

debit | credit | debit | Income Statement | YES |

| ACCT 2101 Topics—Adjusting entries | Fact | Journal Entry | Calculate Amount | Format |

| Concept of adjusting entries | x | |||

| Deferred expenses | x | |||

| Journalize adjustment for prepaid supplies (deferred expense) | x | x | ||

| Journalize adjustment for prepaid rent (deferred expense) | x | x | ||

| Journalize adjustment for prepaid insurance (deferred expense) | x | x | ||

| Journalize adjustment for prepaid taxes (deferred expense) | x | x | ||

| Concept of depreciation | x | |||

| Journalize adjustment for depreciation (deferred expense) | x | x | ||

| Book value | x | |||

| Deferred revenue | x | |||

| Journalize adjustment for deferred revenue | x | x | ||

| Accrued expenses | x | |||

| Accrued expenses | x | |||

| Journalize adjustment for accrued wages (accrued expense) | x | x | ||

| Journalize adjustment for accrued taxes (accrued expense) | x | x | ||

| Journalize adjustment for accrued interest (accrued expense) | x | x | ||

| Accrued revenue | x | |||

| Journalize adjustment for accrued revenue | x | x | ||

| Effect of omitting adjusting entries on the financial statements | x | |||

| Financial statements | x | x | ||

| Journalize closing entries | x | |||

| Post closing entries | x |

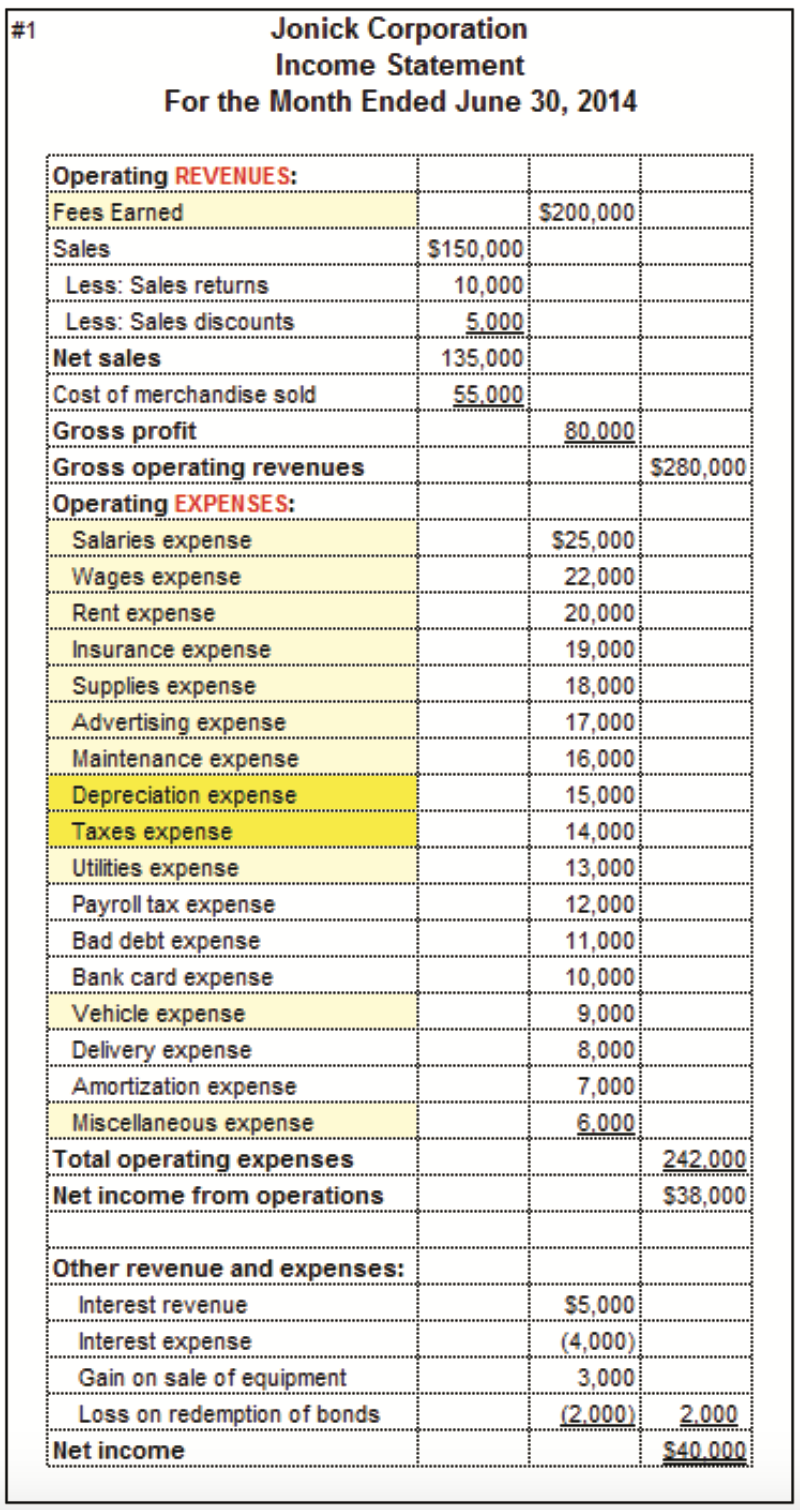

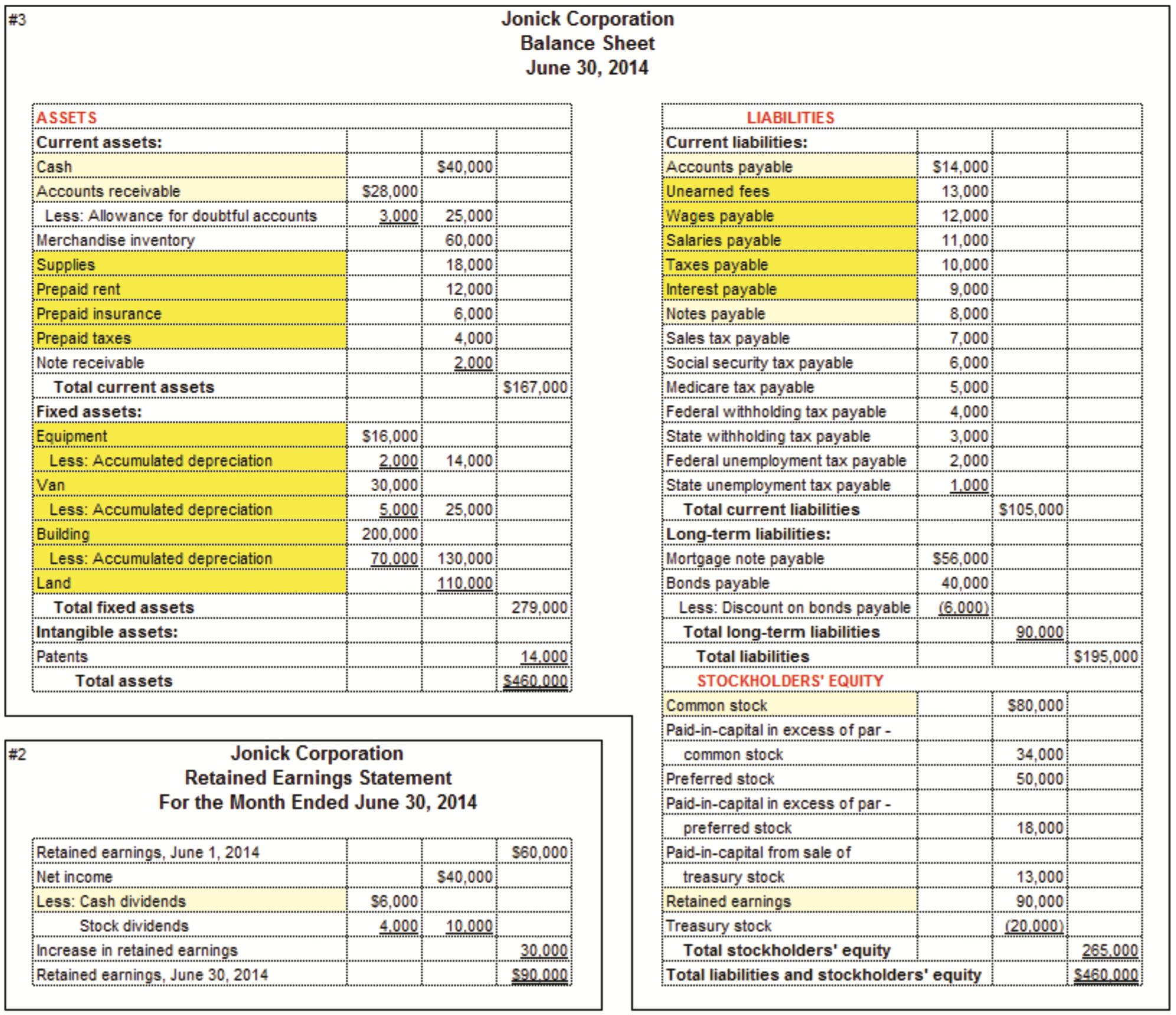

The accounts that are highlighted in bright yellow are the new accounts you just learned. Those highlighted in pale yellow are the ones you learned previously.