1.7: The Accounting Equation

- Page ID

- 43060

The accounting equation is the basis for all transactions in accounting. It provides the foundation for the rules of debit and credit in the journalizing process, where for each transaction total debits must equal total credits. As a result, theaccounting equation must be in balance at all times for a business’ financial records to be correct. It involves the three types of accounts that do not appear on the income statement.

Assets = Liabilities + Stockholders’ Equity

Businesses own assets. These may be partially owned by the owners (stockholders) and partially owned by outsiders (debtors).

When you purchase an asset, there are two ways to pay for it—with your own money and with other people’s money. This concept is a simple description of the accounting equation.

When you buy a truck, you can pay cash for it, as shown in the following journal entry:

| Date | Account | Debit | Credit | |

| 1/1 | Truck | 30,000 | ||

| Cash | 30,000 | |||

If you pay in full, you own the entire vehicle and receive title to it.

Assets = Liabilities + Stockholders’ Equity

30,000 = 0 + 30,000

As an alternative, you may purchase the truck by making a down payment for part of its cost and taking out a loan for the remainder. This is summarized by the following journal entry.

| Date | Account | Debit | Credit | |

| 1/1 | Truck | 30,000 | ||

| Cash | 30,000 | |||

| Note Payable | 20,000 | |||

Assets = Liabilities + Stockholders’ Equity

30,000 = 20,000 + 10,000

This second scenario is a good illustration of the accounting equation using just one asset. The buyer receives the entire asset – the truck. The buyer must pay for this asset. They do so with two forms of payment: their own money (equity) and other people’s money (the loan). The combined total of their down payment and the loan equal the cost of the truck.

The asset is the truck, the liability is the loan, and the down payment is the owner’s equity.

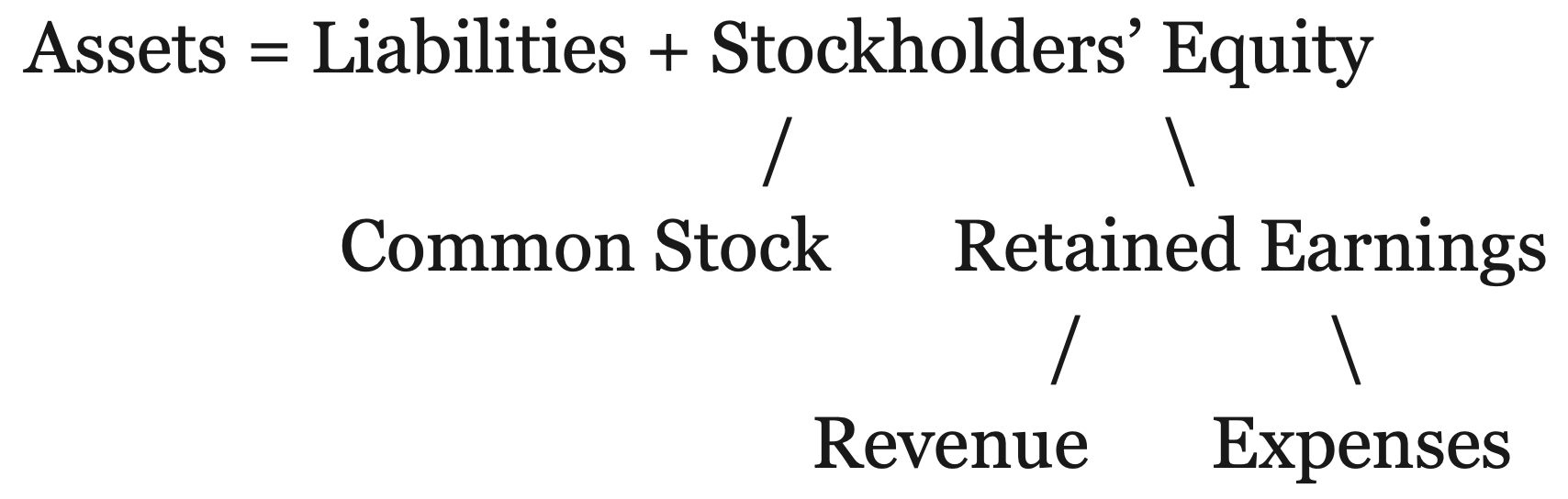

1.7.1 Accounting Equation Broken Out

Indirectly, revenue and expense accounts are part of this accounting equation since they impact the value of stockholders’ equity by affecting the value of Retained Earnings.

The Retained Earnings account normally has a credit balance. Closing entries move the credit balances of revenue accounts into Retained Earnings and cause that account to increase. Closing entries also transfer the debit balances of expense accounts into Retained Earnings, causing it to decrease.

Common Stock plus Retained Earnings equals total stockholders’ equity.

1.7.2 Accounting Transaction Grid

The following grid illustrates how familiar transactions for a new business fit into the accounting equation: ASSETS = LIABILITIES + STOCKHOLDERS’ EQUITY.

| Assets | = Liabilities | + Stockholders’ | Equity | Revenue | Expenses | |||

| Cash | Accounts Receivable | = Accounts Payable | + Common Stock | Retained Earnings | Fees Earned | Rent Expense | Supplies Expense | |

| Issued stock for cash, $1,000 | 1,000 | 1,000 | ||||||

| Paid cash for rent, $700 | (700) | (700) | ||||||

| Sold to customers for cash, $900 | 900 | 900 | ||||||

| Purchased supplies on account, $200 | 200 | (200) | ||||||

| Sold to customers on account, $500 | 500 | 500 | ||||||

| Paid cash on account, $200 | (200) | (200) | ||||||

| Purchased supplies on account, $100 | 100 | 400 | (100) | |||||

| Sold to customers on account, $400 | 400 | |||||||

| Received cash on account, $500 | 500 | (500) | ||||||

| Closed revenue account | 1,800 | (1,800) | ||||||

| Closed expense accounts | (1,000) | 700 | 300 | |||||

| Ending balances | 1,500 | 400 | 100 | 1,000 | 800 | 0 | 0 | 0 |

Each transaction in the first column impacts two accounts. For the asset, liability, and stockholders’ equity amounts, positive numbers represent increases and negative amounts indicate decreases. The ending balances prove that total assets of $1,900 (1,500 + 400) equal total liabilities and stockholders’ equity of $1,900 (100 +1,000 + 800).

Revenue and expense accounts were used temporarily and were ultimately closed to Retained Earnings. As a result, the income statement account balances were set to zero and the Retained Earnings balance increased by the net income amount of $800.

1.7.3 Retained Earnings Statement

The retained earnings statement is a report that shows the change in the Retained Earnings account balance from the beginning of the month to the end of the month due to net income (or loss) and any cash dividends declared during the accounting period.

| Retained earnings, June 1, 2018 | $30,000 | |

| Net income | $13,000 | |

| Less: Cash dividends | 3,000 | |

| Increase in retained earnings | 10,000 | |

| Retained earnings, June 30, 2018 | $40,000 |

Sample Retained Earnings Statement

- Start with Retained Earnings balance at the beginning of the month.

- Add net income form the current month’s income statement.

- Subtract from net income any dividends declared during the month.

- End with new Retained Earnings balance at the end of the month.

Profit is such an important concept in business that two financial statements are devoted to talking about it. The income statement reports net income for one period, such as a month or a year. The retained earnings statement deals with a company’s net income over the entire life of the business.

The retained earnings statement is a bridge between the income statement and the balance sheet. The net income amount that appears on the retained earnings statement comes from the income statement ($13,000 in the sample above). The ending retained earnings balance ($40,000 in the sample above) feeds to the stockholders’ equity section of the balance sheet.

The retained earnings statement includes elements similar to those in a monthly bank statement Both statements report a beginning balance, additions, subtractions, and an ending balance.

| Bank Statement (tracks your cash) |

Retained Earnings Statement (tracks a corporation’s accumulated profit) |

| Balance at the beginning of the month Deposits Withdrawls Balance at the end of the month |

Balance at the beginning of the month Net Income Dividends Balance at the end of the month |

1.7.4 Balance Sheet

The balance sheet is a report that summarizes a business’s financial position as of a specific date. It is the culmination of all the financial information about the business—everything else done in the accounting cycle leads up to it.

The balance sheet is an expanded version of the accounting equation: Assets = Liabilities + Stockholders’ Equity. The balance sheet lists and summarizes asset, liability, and stockholders’ equity accounts and their ledger balances as of a point in time. Assets are listed first. Liabilities and stockholders’ equity accounts follow, and these amounts are added together.

The only exception is that the amount reported on the balance sheet for Retained Earnings comes from the ending balance on the retained earnings statement rather than from its ledger. Note that Cash Dividends is not listed at all on the balance sheet.

BALANCE SHEET FORMATTING

Heading: Company Name, Name of Financial Statement, Date

Two columns: left for listing items to be subtotaled; right for results

Dollar signs go at the top number of a list to be calculated

Category headings for each account category

Single underline below a list of numbers to be totaled

Double underline below the final results (total assets AND Total labilities and stockholders’ equity)

Dollar sign on final result number

| Fees Earned | $30,000 | |

| Operating Expenses: | ||

| \(\ \quad \quad\)Salaries expense | $2,500 | |

| \(\ \quad \quad\)Wages expense | 2,200 | |

| \(\ \quad \quad\)Rent expense | 2,000 | |

| \(\ \quad \quad\)Insurance expense | 1,900 | |

| \(\ \quad \quad\)Supplies expense | 1,800 | |

| \(\ \quad \quad\)Advertising expense | 1,700 | |

| \(\ \quad \quad\)Maintenance expense | 1,600 | |

| \(\ \quad \quad\)Utilities expense | 1,400 | |

| \(\ \quad \quad\)Vehicle expense | 1,100 | |

| \(\ \quad \quad\)Miscellaneous expense | 800 | |

| Total operation expenses | 17,000 | |

| Net Income | 13,000 |

| Retained earnings, June 1, 2018 | $30,000 | ||

| Net income | 13,000 | ||

| Less: cash dividends | 3,000 | ||

| Increase in retained earnings | 10,000 | ||

| Retained earnings, June 30, 2018 | $40,000 |

Financial Reporting

The life of an ongoing business can be divided into artificial time periods for the purpose of providing periodic reports on its financial activities.

Financial Statements Connected

Three financial statements are prepared at the end of each accounting period. First,

the income statement shows net income for the month. Next, the statement of retained earnings shows the beginning and ending Retained Earnings balances and the reasons for any change in this balance. Finally, the balance sheet presents asset, liability, and stockholders’ equity account balances.

#1 The income statement is prepared first. It summarizes revenue and expenses for the month. Amounts come from the ledger balances. The result is either net income or net loss.

#2 The retained earnings statement is next. It adjusts the month’s beginning retained earnings balance by adding net income from the income statement and subtracting out dividends declared. The net income of $13,000 comes from the income statement. The result is a new retained earnings balance at the end of the month.

#3 The balance sheet is prepared last. It shows assets, liabilities, and stockholders’ equity as of the last day of the month. All amounts except retained earnings come from the ledger balances. The Retained Earnings amount comes from the ending amount on the retained earnings statement - in this case $40,000. The balance sheet is an exploded version of the accounting equation!

| Cash | $15,000 | |

| Accounts receivable | 10,000 | |

| Equipment | 5,000 | |

| Truck | 30,000 | |

| Total assets | $60,000 |

| Liabilities | ||

| Accounts payable | $5,000 | |

| Stockholders’ Equity | ||

| Common stock | $15,000 | |

| Retained earnings | 40,000 | |

| \(\ \quad \quad\)Total stockholders’ equity | 55,000 | |

| Total liabilities and stockholders’ equity | $60,000 | |