13.3: Changes to the Partners

- Page ID

- 26261

Partner Withdrawal

In your partnership, you may decide to add new partners. Or, you may decide you or one of your partners need to leave the partnership. Worst case scenario is the death of one of your partners. What do you do?

For withdrawal of a partnership, either from death or choice, there are a several scenarios:

- The individual partners pay, with their own cash and not the partnership cash, the leaving partner for a share of the leaving partner’s capital account.

- The partnership pays the leaving partner for the value of his or her capital account + a cash bonus.

- The leaving partner pays a bonus to the remaining partners by not taking the full amount of the his or her capital balance. Any remaining balance would be allocated between the remaining partners.

This video will demonstrate the process for both scenarios and the journal entries for the first scenario.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=240

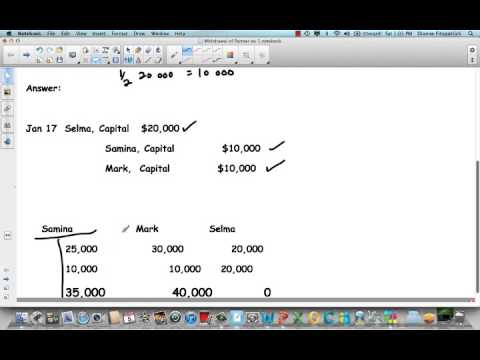

When a bonus is paid to the retiring partner using partnership cash, the capital account of the retiring partner is debited and any bonus amount is allocated to the remaining partner accounts according to their agreed upon profit and loss sharing percentages.

In the video, a partner was leaving and received a $2,000 bonus or $12,000 total cash from the partnership since his capital balance was $10,000 (let’s call him S. Leavy). Two partners remain (we will call them I. Staying and M. Too) and share profits equally. The journal entry to withdrawal of S. Leavy from the partnership is:

| Account | Debit | Credit |

| S. Leavy, Capital | 10,000 | |

| I. Staying, Capital ($2000 bonus / 2) | 1,000 | |

| M. Too, Capital ($2000 bonus / 2) | 1,000 | |

| Cash | 12,000 | |

| To record bonus paid to retiring partner (S.Leavy) |

The last scenario in the video, a partner was leaving but decided not to take the full amount of his capital balance. S. Leavy had a capital balance of $12,000 and wants to leave the partnership by receiving $8,000 cash. Two partners remain (we will call them I. Staying and M. Too) and share profits equally. The journal entry to withdrawal of S. Leavy from the partnership is:

| Account | Debit | Credit |

| S. Leavy, Capital | 12,000 | |

| Cash | 8,000 | |

| I. Staying, Capital ($4000 bonus / 2) | 2,000 | |

| M. Too, Capital ($4000 bonus / 2) | 2,000 | |

| To record bonus paid by retiring partner (S.Leavy) |

Partner Admission

A partner can be added to an existing partnership in four ways, including:

- New partner can purchase part of the interest of another partner.

- New partner can invest cash or other assets in the business.

- New partner can pay a bonus to existing partners by paying more than interest percentage received.

- New partner can receive a bonus from partnership by paying less than the interest percentage received.

We will look at each one individually including journal entries and effect on owner’s capital.

1. New partner can purchase part of the interest of another partner.

Sam Sun and Roni Rain are partners. Sam has a capital balance of $100,000 and Roni $90,000. Chloe Cloud wants to join the partnership. Roni Rain has agreed to sell Chloe 1/3 of her interest in the partnership for $40,000 cash. The cash will be paid directly to Roni and not to the partnership. This will not change total partnership equity but instead 1/3 of Roni Rain’s capital balance will be transferred to Chloe Cloud in the following entry:

| Debit | Credit | |

| R. Rain, Capital | 30,000 | |

| C. Cloud, Capital | 30,000 | |

| To record admittance of C. Cloud. |

Total partnership equity remains at $190,000 with Sam Sun having $100,000, Roni Rain $60,000 (90,000 original – 30,000 to Chloe), Chloe Cloud $30,000.

2. New partner can invest cash or other assets in the business.

In this scenario, the new partner will provide cash or other assets directly to the partnership to become an owner. Since the partnership is receiving the cash or other assets, we will record those at fair market values and there will be no change to the existing partners.

Chloe Cloud invests $50,000 cash to be come a new partner with Sam Sun and Roni Rain. Since the cash is received by the partnership, we will record this and give Chloe cloud her capital balance. The entry to record this would be:

| Debit | Credit | |

| Cash | 50,000 | |

| C. Cloud, Capital | 50,000 | |

| To record admittance of C. Cloud for cash. |

Assuming the same beginning facts as example 1, the new partnership equity would be $240,000 (Sam Sun $100,000; Roni Rain $90,000; Chloe Cloud $50,000).

3. New partner can pay a bonus to existing partners by paying more than interest percentage received. This occurs when the partnership has a current market value greater than the current partner’s equity.

Assume Sun and Rain partnership equity is $190,000 total. Chloe Cloud will pay the partnership $85,000 cash to get a 30% interest in the business. First, we need to calculate the new value of the partnership. The new value will be existing capital $190,000 + $85,000 new partner cash for $275,000. Second, we calculate the value of a 30% interest by multiplying new capital total by 30 % (275,000 x 30% = $82,500). Third, we compare the cash paid by new partner $85,000 – to value of 30% interest $82,500 to get the bonus to the other partners of $2,500. Finally, we will divide the bonus between the partners using profit and loss sharing agreements but for ease let us assume it is divided equally ($2,500 / 2 partners = $1,250 each). We will increase each of the old partner’s capital accounts by the bonus amount. The journal entry would be:

| Debit | Credit | |

| Cash (paid by Cloud) | 85,000 | |

| C. Cloud, Capital (30% interest) | 82,500 | |

| S. Sun, Capital ($2,500 bonus / 2) | 1,250 | |

| R. Rain, Capital ($2,500 bonus / 2) | 1,250 | |

| To record admission and bonus to C. Cloud |

The new partnership equity would be $275,000 with Cloud added and Sun and Rain will have increased their capital by $1,250 each. Capital balances are: Sun $101,250; Rain $91,250; and Cloud $82,500.

4. New partner can receive a bonus from partnership by paying less than the interest percentage received. This can occur when the new partner has a special skill or expertise needed by the partnership or the partnership just needs the cash!

Assume Sun and Rain partnership equity is $190,000 total. Chloe Cloud will pay the partnership $42,000 cash to get a 20% interest in the business. First, we need to calculate the new value of the partnership. The new value will be existing capital $190,000 + $42,000 new partner cash for $232,000. Second, we calculate the value of a 20% interest by multiplying new capital total by 20 % (232,000 x 20% = $46,400). Third, we compare the value of the 20% interest $46,400 – cash paid by new partner $42,000to get the bonus to the new partner of $4,400. Finally, we will divide the bonus between the partners using profit and loss sharing agreements but for ease let us assume it is divided equally ($4,400/ 2 partners = $2,200 each). This bonus would reduce each of the old partner’s capital balances. The journal entry would be:

| Debit | Credit | |

| Cash (paid by Cloud) | 42,000 | |

| S. Sun, Capital ($4,400 / 2) | 2,200 | |

| R. Rain, Capital ($4,400 / 2) | 2,200 | |

| C. Cloud, Capital | 82,500 | |

| To record admission and bonus to C. Cloud |

The new partnership equity would be $232,000 with Cloud added but Sun and Rain decreased their capital by $2,200 each. Capital balances are: Sun $97,800; Rain $87,800; and Cloud $46,400.

http://www.openassessments.org/assessments/1207

- BAT C13 V4 Withdrawal of partner.mp4 . Authored by: Dianne Fitzpatrick. Located at: https://youtu.be/I92UrTGT6gQ. License: All Rights Reserved. License Terms: Standard YouTube License