13.2: Journal Entries for Partnerships

- Page ID

- 26260

Investing in a partnership

Partners (or owners) can invest cash or other assets in their business. They can even transfer a note or mortgage to the business if one is associated with an asset the owner is giving the business. Assets contributed to the business are recorded at the fair market value. Anytime a partner invests in the business the partner receives capital or ownership in the partnership. You will have one capital account and one withdrawal (or drawing) account for each partner.

To illustrate, Sam Sun and Ron Rain decided to form a partnership. Sam contributes $100,000 cash to the partnership. Ron is going to give $25,000 cash and an automobile with a market value of $30,000. Ron is also going to transfer the $20,000 note on the automobile to the business. The journal entries would be:

| Account | Debit | Credit |

| Cash | 100,000 | |

| S. Sun, Capital | 100,000 | |

| To record cash contribution by owner | ||

| Cash | 25,000 | |

| Automobile | 30,000 | |

| Note Payable | 20,000 | |

| R. Rain, Capital (25,000 + 30,000 – 20,000) | 35,000 | |

| To record assets and note contributed by owner |

The entries could be separated as illustrated or it could be combined into one entry with a debit to cash for $125,000 ($100,000 from Sam and $25,000 from Ron) and the other debits and credits remaining as illustrated. Either way is acceptable. Since the note will be paid by the partnership, it is recorded as a liability for the partnership and reduces the capital balance of Ron Rain.

Partners can take money out of the business whenever they want. Partners are typically not considered employees of the company and may not get paychecks. When the partners take money out of the business, it is recorded in the Withdrawals or Drawing account. Remember, this is a contra-equity account since the owners are reducing the value of their ownership by taking money out of the company.

To illustrate, Sam Sun wants to go on a beach vacation and decides to take $8,000 out of the business. Ron Rain wants to go to Scotland and will take $15,000 out of the business. The journal entries would be:

| Account | Debit | Credit |

| S. Sun, Withdrawal | 8,000 | |

| Cash | 8,000 | |

| To record cash withdrawn by owner | ||

| R. Rain, Withdrawal | 15,000 | |

| Cash | 15,000 | |

| To record cash withdrawn by owner |

Just as in the previous example, the entries could also be combined into one entry with the credit to cash $23,000 ($8,000 from Sam + $15,000 from Ron) and the debits as listed above instead.

Income Allocation

Once net income is calculated from the income statement (revenues – expenses), net income or loss is allocated or divided between the partners and closed to their individual capital accounts. The partners should agree upon an allocation method when they form the partnership. The partners can divide income or loss anyway they want but the 3 most common ways are:

- Agreed upon percentages: Each partner receives a previously agreed upon percentage. For example, Sam Sun will get 60% and Ron Rain will get 40%. To allocate income, net income or loss is multiplied by the percent agreed upon.

- Percentage of capital: Each partner receives a percentage of capital calculated as Partner Capital / Total capital for all partners. Using Sam and Ron, Sam has capital of $100,000 and Ron has capital of $35,000 for a total partnership capital of $135,000 (100,000 + 35,000). Sam’s percentage of capital would be 74% (100,000 / 135,000) and Ron’s percentage would be 26% (35,000 / 135,000). To allocate income, the percent of capital is multiplied by the net income or loss for the period.

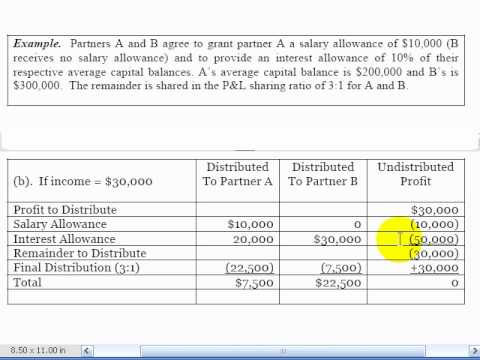

- Salaries, Interest, Agreed upon percent: Since owners are not employees and typically do not get paychecks, they should still be compensated for work they do for the business. In this method, we start with net income and give salaries out to the partners, then we calculate an interest amount based on their investment in the business, and any remainder is allocated using set percentages. This is by far the most confusing so a video example would be helpful.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=238

Note: The video shows a sharing ratio of 3:1. To use this in calculations, you will add the numbers presented together (3 + 1 = 4) and divide each number of the sharing ratio by this total to get a percentage. The sharing ratio of 3:1 means 75% ( 3/4) and 25% ( 1/4).

The journal entries to close net income or loss and allocate to the partners for each of the scenarios presented in the video would be (remember, revenues and expenses are closed into income summary first and then net income or loss is closed into the capital accounts):

| Account | Debit | Credit |

| Income Summary | 70,000 | |

| Partner A, Capital | 37,500 | |

| Partner B, Capital | 32,500 | |

| To record allocation of $70,000 net income to partners. | ||

| Income Summary | 30,000 | |

| Partner A, Capital | 7,500 | |

| Partner B, Capital | 22,500 | |

| To record allocation of $30,000 net income to partners. | ||

| Partner A, Capital | 22,500 | |

| Partner B, Capital | 12,500 | |

| Income Summary | 10,000 | |

| To record allocation of $10,000 net LOSS to partners. |

If the partners cannot or do not decide how income will be allocated, allocate it equally between the partners (for 4 partners divide net income by 4; for 3 partners divide net income by 3, etc.).

Liquidation of a Partnership

Sometimes things do not go as well as planned in a business and it may be necessary to go out of business. When a partnership goes out of business, the following items must be completed:

- All closing entries should be completed including allocating any net income or loss to the partners.

- Any non-cash assets should be sold for cash and any gain or loss from the sale would be allocated to the partners.

- Any liabilities should be paid.

- Any remaining cash is allocated to the partners based on the capital balance in each partner’s account (note: this is not an allocated figure but the actual capital balance for each partner after the other transactions).

Here is a good (but long) video demonstrating the liquidation process and the journal entries required.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=238

- Accounting Lecture 12 - Division of Partnership Profit and Loss. Authored by: Craig Pence. Located at: https://youtu.be/wODP0UekxhM. License: All Rights Reserved. License Terms: Standard YouTube License

- Chapter 12 Lecture 3 - Accounting for the Liquidation of a Partnership . Authored by: Doug Parker. Located at: https://youtu.be/rqFHf2uB6og. License: All Rights Reserved. License Terms: Standard YouTube License