Chapter 13: Icebergs and Escapes

- Page ID

- 163071

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Chapter 13

Icebergs and Escapes

Image retrieved from StockSnap

| Learning Objectives |

|---|

|

After completing this chapter, you will be able to:

|

Most resources on small business management focus, quite correctly, on the challenges and rewards of starting and growing a business. But experienced owners know that running a business well also means anticipating what can go wrong, the icebergs lurking below the surface that can sink an otherwise healthy operation. Disasters happen. Markets shift. Health fails. Circumstances change. Sometimes things go so well that the owner is simply ready for the next chapter.

This chapter addresses both sides of that reality. The first half covers disaster preparedness: how to plan before a crisis strikes, and where to turn for help if it does. The second half covers the exit: the circumstances that lead owners to leave their businesses, and the strategies available for doing so on their own terms. Neither topic is comfortable to think about. Both are essential.

A natural or man-made disaster is the visible tip of the iceberg. The full complexity of what lies below: the operational disruptions, the financial exposure, the human cost, the decisions that must be made under pressure, is what requires planning well in advance. Small and medium-sized businesses are particularly vulnerable when disaster strikes. They typically have less financial cushion, fewer redundancies in staffing and operations, and less capacity to sustain losses while rebuilding.

The statistics are sobering. According to data cited by the Congressional Research Service, 40% of businesses never reopen following a disaster, and another 25% of those that do reopen close within one year. The SBA estimates that 90% of businesses fail within two years of being struck by a disaster (Lawhorn & Lindsay, 2023).

Disasters fall into two broad categories. Natural disasters include severe storms, flooding, wildfires, hurricanes, tornadoes, earthquakes, and public health emergencies such as the COVID-19 pandemic, which was declared a federal disaster in all 50 states and caused widespread small business closures. Every region of the United States faces some exposure: not all businesses face the same risks, but fires, severe weather, and flooding can affect almost any location. Man-made disasters are events caused by deliberate or negligent human actions, including arson, structural failure, cybersecurity breaches, civil disorder, and industrial incidents. According to survey data cited by Cadden and Lueder (2012), man-made disasters affect approximately 10% of small businesses, while natural disasters have affected more than 30%.

The lesson from these numbers is not that disaster is inevitable: it is that the probability is high enough, and the consequences severe enough, that planning is not optional. A business that has planned for disaster can resume operations in days. A business that has not may never reopen.

| Key Takeaways |

|---|

|

Anticipating what can go wrong is not pessimism: it is one of the most productive things a small business owner can do. When NASA engineers spent years running simulations of everything that could go wrong during the Apollo missions, the astronauts sometimes complained that the scenarios were unrealistic and unlikely. But when a genuine near-catastrophe struck Apollo 13, the training and planning those simulations had produced made an improvised solution possible. The best time to think through disaster response is before a disaster occurs.

The Federal Emergency Management Agency (FEMA) and the Department of Homeland Security have developed a business disaster preparedness framework through Ready.gov, endorsed by the National Fire Protection Association’s Emergency Preparedness Business Continuity Standard (NFPA 1600). This framework organizes disaster planning into three areas, illustrated in the figure below.

Figure 13.1 The three areas of small business disaster planning. Source: Cadden & Lueder, Small Business Management in the 21st Century (CC BY-NC-SA 3.0); adapted from Ready.gov

The foundation of disaster planning is an honest risk assessment: what types of disasters are most likely given the business’s location and industry, and what is the business’s specific vulnerability to each? Fires are the most common disaster affecting businesses in the United States. Flooding, severe storms, and cyber incidents are close behind for many regions and industries. Once risks are identified, planning can be targeted.

A business continuity plan is the documented strategy for keeping the business operational, or restoring operations quickly, in the event of a disruption. It is sometimes described as the least expensive insurance a small business can have, because it costs virtually nothing to produce but can mean the difference between recovery and closure. Key elements include:

- Identifying the personnel without whom the business cannot function, and designating backups for each critical role.

- Documenting external contacts: suppliers, shippers, utilities, the business’s bank, legal counsel, and IT support, so they can be reached quickly in a crisis.

- Identifying which employees can work remotely and ensuring they have the access and tools to do so.

- Planning for payroll continuity, so employees can be paid even if normal operations are disrupted.

- Creating a complete inventory of critical equipment and ensuring it is documented with enough detail to support insurance claims and replacement decisions.

- Backing up all critical data and documents to a secure offsite location. The SBA recommends storing vital records at least 50 miles from the primary business site. Cloud-based storage services make this straightforward and affordable for businesses of any size.

- Identifying a contingency operating location: a place where the business could function if the primary site is unavailable. Many hotels offer business facilities; having a backup plan for the backup plan is also worthwhile.

- Keeping the plan current. Circumstances change: staff turns over, suppliers change, technology evolves. The plan should be reviewed and updated regularly.

A disaster plan that lives in the owner’s head or in a drawer is not a plan: it is a document. The people who will need to execute it in a crisis must know it exists, understand their role in it, and be able to reach the right contacts under pressure.

This means involving employees at all levels in creating and maintaining the plan, not just distributing it after the fact. It means establishing clear procedures for communicating with staff before, during, and after a disaster, including accommodations for employees with disabilities, hearing impairments, or language barriers. It means assigning specific employees responsibility for notifying specific contacts (suppliers, customers, creditors, public officials) so that communication happens systematically rather than haphazardly.

A written crisis communication plan should specify who is responsible for communicating with each stakeholder group, what information will be shared, and through what channels. Keeping customers informed about whether and when they can expect products or services is especially important: uncertainty drives customers to competitors faster than almost anything else.

Disasters also carry psychological weight. Owners and key employees may experience fear, stress, anxiety, and difficulty making decisions in the aftermath of a serious event. The plan should acknowledge this reality: allowing time for family needs, establishing an open-door policy for employees seeking support, working to reestablish routines as quickly as possible, and ensuring that the owner’s own health and wellbeing are not neglected. Leaders under extreme stress make poor decisions, and poor decisions in the aftermath of a disaster can compound the damage significantly.

The third area of disaster planning focuses on protecting the physical and digital assets of the business before disaster strikes.

Insurance is the most direct form of financial protection. Standard property insurance typically does not cover flooding: a business in a flood-prone area needs separate flood coverage. Business interruption insurance is particularly important for small businesses: it covers ongoing expenses (rent, utilities, loan payments, payroll) and lost income during the period when the business cannot operate normally. Premiums are typically based on the company’s revenue, and the coverage can be the difference between surviving a closure and not surviving it. Meeting with an insurance agent who understands the specific needs of the business, and reviewing that coverage at least annually, is a basic management responsibility, not an afterthought.

Physical security measures appropriate to the business include smoke detectors and fire extinguishers, emergency route maps posted in multiple locations, alarm systems, and procedures for identifying and handling suspicious packages or mail. The specific measures that make sense depend on the industry, location, and nature of the operation.

Cybersecurity deserves its own attention. Small businesses are disproportionately targeted in cyberattacks precisely because they tend to have weaker security than large corporations while still holding valuable customer data, financial records, and operational information. The SBA’s cybersecurity resources (available at sba.gov/business-guide/manage-your-business/stay-safe-cybersecurity-threats) provide practical, no-cost guidance tailored to small businesses. At a minimum, every small business should use current antivirus software, enforce strong password policies, back up data regularly to a secure location, and train employees to recognize phishing emails and suspicious links. Cybersecurity insurance is increasingly available and affordable, covering costs related to data breaches, notification requirements, and business interruption from cyber incidents.

| Think about it |

|---|

|

You own a small Las Vegas event catering company with six full-time employees. You store client contracts, payment records, and event schedules on a shared drive on one computer in your office. Your insurance covers the building and equipment but you have never reviewed the policy in detail. A fire overnight destroys your office and everything in it. Walk through what the next 72 hours look like for your business. What could you have done in advance to change that picture? Which element of disaster planning: continuity plan, communication plan, or protecting the investment, would have the most immediate impact? |

| Key Takeaways |

|---|

|

Even the best-prepared business may face losses that exceed its insurance coverage or its own financial reserves. Several federal and state programs exist to help small businesses recover. Knowing what is available, and what is not guaranteed, is part of responsible planning.

The Small Business Administration (SBA) offers low-interest disaster loans to small businesses that have sustained losses in a federally declared disaster area. There are two primary types.

Physical Disaster Loans are available to businesses that have sustained physical damage to real estate, equipment, inventory, or other business assets. As of 2025, eligible businesses may borrow up to $2 million to repair or replace disaster-damaged property. The loan amount may be increased by up to 20% of verified losses to protect against future disasters of the same type. Losses not covered by insurance are eligible.

Economic Injury Disaster Loans are available to businesses that were not physically damaged but have suffered significant economic losses because of a disaster: expenses and financial obligations the business would have met if the disaster had not occurred. These loans are also available up to $2 million (SBA.gov, 2025).

For both loan types, the interest rate for businesses without credit available elsewhere is capped at 4%. For businesses that have access to credit from other sources, the rate is capped at 8%. Repayment terms extend up to 30 years depending on the borrower’s ability to repay, and interest does not begin to accrue until 12 months after the first disbursement. The SBA determines eligibility and sets loan amounts based on each applicant’s financial condition (SBA.gov, 2025).

Disaster loan funding is subject to congressional appropriations. In October 2024, the SBA’s disaster loan program exhausted its funding for the first time in program history following unprecedented demand from Hurricanes Helene and Milton. Congress restored funding in December 2024. This experience underscores why insurance coverage should be the first line of defense: government programs are a safety net, but they are not guaranteed to be immediately available.

Local, county, regional, and state governments may also offer small business disaster relief loans. Checking with Nevada’s Department of Business and Industry (business.nv.gov) and Clark County’s Office of Community and Economic Development is a useful first step for Las Vegas-area businesses seeking local assistance.

When the federal government declares a major disaster area, the IRS may offer tax relief to affected businesses, including extensions on filing deadlines and payment due dates. IRS disaster relief provisions vary by event and declaration. Checking the IRS website (irs.gov) for the specific declaration affecting your area is the most reliable way to identify what relief is available. Documenting all losses carefully, with photographs, receipts, and records, before cleanup begins will support both insurance claims and any IRS casualty loss deductions.

SCORE (Service Corps of Retired Executives) is a nonprofit organization that provides free, confidential business counseling through a network of experienced volunteers nationwide. SCORE counselors can help business owners navigate disaster recovery decisions: whether to rebuild, how to approach lenders and insurers, and how to think through what comes next. SCORE services are available at score.org and through local chapters in every major city.

DisasterAssistance.gov is a federal one-stop portal providing information on assistance programs from more than a dozen government agencies. Owners can apply for SBA loans through the portal, check application status, and find referrals to programs that do not have online applications. It is the most direct starting point for federal disaster recovery resources.

| Key Takeaways |

|---|

|

Running a small business is demanding, and there are many circumstances, both chosen and forced, in which the wisest decision is to leave. Recognizing those circumstances, and having thought through them in advance, is part of running a business well.

There are many reasons an owner might choose to exit a business. The most straightforward is timing: the owner has built something of value and wants to realize that value before retirement or while the business is at its peak. Someone has approached them with a compelling offer. Investors are pressing for a return. No family member wants to take over. Or the work that was once energizing has become a grind: the entrepreneurial spirit is gone, the passion has shifted, and the owner is no longer having fun.

These are legitimate and common reasons to exit, and they are not signs of failure. John Bello and Tom Schwalm, founders of SoBe Beverages, built their company from zero to $300 million in revenue and sold it to PepsiCo in 2000 for $370 million, in part because the business was growing into something they no longer wanted it to be, and the market conditions were favorable for a sale. Recognizing that moment, and acting on it deliberately rather than reactively, is the mark of a skilled operator, not a quitter.

Other signals that an exit may be worth considering include spending increasing time managing small problems rather than driving the business forward; taking a consistently negative view of the team’s decisions and future prospects; or realizing that continuing the business is threatening the owner’s health, marriage, or family relationships in ways no longer worth the reward.

Not all exits are voluntary. Several circumstances can force an owner out of a business regardless of their preferences.

The founder’s dilemma refers to the fundamental tension between controlling a business and maximizing its financial value. Owners who want to make substantial money from a business typically must give up equity to attract investors, and giving up equity means relinquishing control. Owners who insist on retaining control must rely on their own capital, which limits growth. In foundational research on new ventures, Wasserman (2008) found that within three years, 50% of founders are no longer the CEO of their own company, and fewer than 25% led their company’s initial public offering. While the startup landscape has evolved since this research, the underlying tension between control and growth capital remains a defining challenge for founders. The message is clear: for founders who prioritize wealth maximization, relinquishing some control is almost always part of the path.

Bankruptcy may force an exit when debts substantially exceed assets and the business cannot be made viable. Inadequate management experience, a deteriorating market, employee theft, fraud, or an uninsured liability judgment can all contribute. Serious illness creates uncertainty about the business’s future that can affect employees, customers, and suppliers, and if no successor is ready, the disruption can be fatal to the operation. Industry collapse: the death of demand for a product or service due to technological disruption, market shifts, or economic dislocation, can force even well-run businesses into closure.

Owners can also be the source of the problem. Micromanaging that suppresses employee initiative, spending on the wrong priorities, chasing every potential customer instead of serving the right ones, inattention to financial management, or a leadership style that drives away good people are all patterns that can slowly sink a business from the inside.

Whether an exit is voluntary or forced, the decision should not be made in isolation. Consulting with a partner, spouse, accountant, attorney, and a SCORE counselor provides different perspectives and different expertise. The financial, legal, tax, and emotional dimensions of an exit are all distinct, and all require attention. The decision itself, ultimately, belongs to the owner. What should not happen is making it without preparation or without an exit strategy.

| Key Takeaways |

|---|

|

An exit strategy is a plan for how an owner will eventually leave the business, and under what terms. It is, as Cadden and Lueder (2012) describe it, likely the most emotional topic a small business owner will face and the hardest decision to make. That is precisely why it should be thought through before the moment arrives, not during it.

An exit strategy should be developed early, reviewed periodically, and updated as circumstances change. It shapes how the business is built: the ownership structure, the financial records kept, the relationships cultivated with potential buyers or successors, and the decisions made along the way that determine what the business is worth when it is time to leave. The exit strategy also affects what the owner walks away with, whether that is money, management continuity, preservation of the brand, or a clean break.

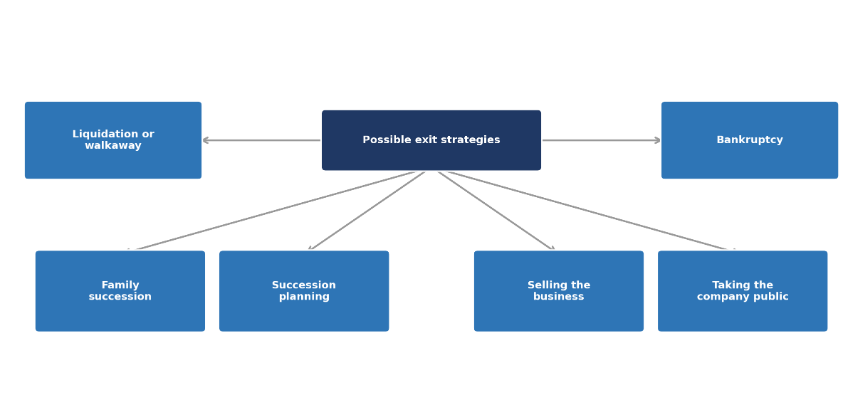

Figure 13.2 Possible exit strategies for small business owners. Source: Cadden & Lueder, Small Business Management in the 21st Century (CC BY-NC-SA 3.0)

The simplest exit is closing the business: selling off assets, paying creditors, and walking away. If all debts are settled, this is called a walkaway. If assets are insufficient to cover debts, liquidation proceeds under a legal framework. Liquidation is common for businesses that have limited value as going concerns: a sole proprietorship built around the owner’s specific skills, a business in a declining industry, or a business that simply did not build the kind of customer base or brand equity that would attract a buyer.

A clean walkaway: bills paid, leases terminated, employees placed, taxes settled, contracts concluded, is the most orderly version of this exit. It is also rarely how it actually unfolds, which is why planning matters. Goodwill, the intangible value built through brand reputation, customer relationships, intellectual property, and market position, is destroyed when a business simply closes rather than being sold. Owners who liquidate without exploring a sale first often leave significant value on the table.

Passing the business to a family member is a goal many small business owners hold, and for good reasons: it preserves the owner’s legacy, keeps the business in the family, and allows the owner to remain involved if desired. But family succession is also the most complex and emotionally fraught exit strategy, and it has a poor track record. Research suggests that very few family businesses survive beyond the first generation, and fewer still into the third (Cadden & Lueder, 2012).

Family succession requires careful planning well in advance of the transition. The plan should identify the successor clearly, provide for their development and preparation, and establish a timeline and process for the transfer of responsibility and authority. A sudden handover is almost always a mistake. The successor’s qualifications, commitment, and relationships with employees and customers all affect whether the business survives the transition.

Succession planning is a formal, documented plan for transferring leadership or ownership of a business to a chosen successor. While family succession is one form of planned transition, succession planning applies more broadly to any situation in which an owner deliberately prepares someone to take over the business. That successor might be a key employee, a trusted member of the management team, a longtime business partner, or an outside candidate brought in specifically for the role.

The essential elements are the same regardless of who the successor is: identify the successor clearly, provide for their development and preparation, and establish a timeline and process for the transfer of responsibility and authority. A well-executed succession plan protects the business, its employees, and its customers through a leadership transition that might otherwise be disruptive. A sudden handover, whether to a family member or to anyone else, is almost always a mistake.

Succession planning is distinct from selling the business in that ownership and leadership may transfer without a traditional market transaction. The owner may transfer equity gradually over time, sell at a negotiated price to a trusted successor, or transfer ownership through an estate plan. The financial and legal dimensions require the same professional guidance as any exit strategy.

Selling the business is the most common substantive exit for small businesses and, done well, often the most financially rewarding. It is also the most complex. An owner can sell a business only once, so the timing, the pricing, the process, and the choice of buyer all matter enormously. Advisors familiar with business valuation and small business sales: a business broker, an accountant, and an attorney at minimum, are not optional; they are essential.

Before pursuing a sale, an owner should honestly assess whether the business is actually sellable: Does it have a history of profitability? A loyal customer base? A strong reputation? A competitive advantage that will survive the ownership change? A skilled and stable team? A business that lacks most of these qualities will generate limited buyer interest, and the seller’s asking price will reflect that reality.

There are several ways to structure a sale:

- Acquisition: another business buys the operation, as PepsiCo acquired SoBe. Acquisitions are common when the business has strategic value to a larger player: a complementary product line, a geographic footprint, an established brand, or an existing customer relationship the acquirer wants. In an acquisition, the negotiated price is not constrained by public market valuations, so a business with genuine strategic value may command a premium well above its book value.

- Friendly buyout: ownership transfers to family members, employees, managers, customers, or friends. The buyer typically knows the business well, reducing due diligence friction, and is more likely to preserve what the seller values about the business. The risk is that personal relationships can cloud the seller’s judgment in negotiations, leading to below-market pricing or overlooked liabilities.

- Open market sale: listing the business for sale through a business broker or online business marketplace is the most common approach. Platforms such as BizBuySell.com reach broad audiences of qualified buyers. The challenge is that an estimated 75% of businesses listed for sale do not sell, often because the asking price is unrealistic, the financial records are inadequate, or the business lacks the attributes that make it attractive to buyers (Cadden & Lueder, 2012). Preparing for an open market sale typically takes three to four years of deliberate effort.

Bankruptcy is a legal process for closing or reorganizing a business when debts substantially exceed assets and the business cannot meet its financial obligations. It is an exit of last resort, not a planning strategy. Chapter 7 bankruptcy involves liquidating the business: a trustee sells assets, uses proceeds to satisfy debts, and discharges what cannot be paid. Chapter 11 bankruptcy allows a business to continue operating under court supervision while reorganizing its finances, though the owner loses management control and the outcome is rarely favorable.

Before concluding that bankruptcy is unavoidable, owners should explore alternatives: negotiating directly with creditors to restructure payment terms, identifying and eliminating unprofitable operations to improve cash flow, or pursuing a turnaround, combining debt renegotiation and operational improvements simultaneously. An attorney experienced in small business financial distress should be consulted before any bankruptcy filing.

An initial public offering (IPO), transferring private equity into publicly traded shares, is a legitimate exit strategy in a narrow set of circumstances. For the vast majority of small businesses, it is not realistic. IPOs are rare: even in active years, fewer than 200 U.S. companies complete one. The process is costly, requiring specialized legal, accounting, and investment banking expertise that can run into hundreds of thousands of dollars in preparation costs alone. Once public, the company is subject to continuous regulatory reporting requirements and the scrutiny of public market analysts. For a small business that has built significant value and has the growth profile to attract public investors, an IPO may be worth exploring. For most, the time and resources required are better directed elsewhere.

| Think about it |

|---|

|

A Henderson couple has owned and operated a successful nail salon for twelve years. They have a loyal clientele, three experienced employees, a well-known local reputation, and a prime retail location. The couple is planning to retire in the next five years. They have never thought formally about an exit strategy. Using the framework from this chapter, which exit strategy or strategies would you recommend they explore? What steps should they take now, five years before their intended exit, to maximize the value of what they have built? |

| Key Takeaways |

|---|

|

Watch and reflect |

|---|

|

Source: U.S. Small Business Administration | YouTube YouTube Clickable Link(opens in new window)Length: 5:08 This video is produced by the U.S. Small Business Administration. Jacqueline Bernetta Tate Smith, owner of The Coffee Shoppe in historic downtown Selma, Alabama, describes what happened when a tornado struck her city in January 2023, devastating the community and cutting off the customer base her business depended on. She explains how an SBA Disaster Loan helped her survive the aftermath and keep her employees working. The Coffee Shoppe is more than a business in Selma. It is a community anchor, and Jackie’s story is a reminder of what is at stake when a small business faces a disaster it did not see coming. After watching, consider the following reflection questions:

|

Use the following questions to test your comprehension of this chapter.

- Research cited in this chapter indicates that 40% of businesses never reopen after a disaster, and the SBA estimates that 90% fail within two years of being struck by one. Given everything you know about Las Vegas and Southern Nevada’s climate and risk profile, what types of disasters are most relevant for small businesses in this region? What elements of a disaster plan would be highest priority for a small restaurant in downtown Las Vegas?

- Business interruption insurance is described as particularly important for small businesses. A local Henderson salon owner says she can’t afford the premium. How would you help her think through that decision? What is the real cost of not having it?

- SBA disaster loans are capped at interest rates of 4% for businesses without credit available elsewhere and up to 8% for those with credit elsewhere, with terms up to 30 years. What are the advantages of these terms compared to commercial borrowing? What are the limitations of relying on SBA disaster loans as your primary recovery strategy?

- The founder’s dilemma describes the tension between controlling a business and maximizing its financial value. Research suggests that 50% of founders are no longer CEO within three years. Is this a failure or a success? How should a founder think about this trade-off when making decisions about investors and equity?

- Rank the exit strategies described in Section 13.5 from most to least desirable for the typical small Las Vegas business owner. Explain your ranking. Under what specific circumstances would your ranking change?

Acquisition — The purchase of one business by another. A common exit strategy when a small business has strategic value to a larger company.

Bankruptcy — A legal process for closing or reorganizing a business when debts substantially exceed assets. Chapter 7 involves liquidation; Chapter 11 allows continued operation under court supervision.

Business continuity plan — A documented strategy for maintaining or restoring business operations following a disruptive event, including identification of key personnel, critical assets, data backup, and contingency locations.

Business interruption insurance — Insurance that covers ongoing expenses and lost income during a period when a business cannot operate normally due to a covered disaster or other disruption.

Employee Stock Ownership Plan (ESOP) — A structure that allows employees to purchase an ownership stake in the business, sometimes used as a mechanism for selling to employees.

Exit strategy — A plan for how an owner will leave a business, under what terms, and with what outcome. Should be developed early and updated as circumstances change.

Founder’s dilemma — The fundamental tension between controlling a business and maximizing its financial value. Retaining control typically limits growth capital; attracting investors typically requires relinquishing control.

Friendly buyout — A transfer of business ownership to family members, employees, managers, customers, or friends. Still a sale, but typically structured differently than an open market transaction.

Goodwill — The intangible value of a business built through brand reputation, customer relationships, intellectual property, and market position. Destroyed when a business closes rather than being sold.

Initial public offering (IPO) — The transfer of private equity in a company into publicly traded shares on a stock exchange. Rare, expensive, and appropriate only for a narrow set of businesses.

Liquidation — The sale of all business assets, typically to pay creditors. If all debts are paid, the process may also be called a walkaway.

Man-made disasters — Disastrous events caused directly and principally by deliberate or negligent human actions, including arson, structural failure, cybersecurity breaches, and civil disorder.

Succession planning — A formal, documented plan for transferring business leadership or ownership to a chosen successor, whether a family member, key employee, or other individual. Ideally developed years before the intended transition.

Walkaway — The clean closure of a business in which all debts are paid, contracts are concluded, and employees are placed before the business ceases operations.

Cadden, D. & Lueder, S. (2012). Small business management in the 21st century. LibreTexts-Saylor Foundation. (Licensed CC BY-NC-SA 3.0)

Lawhorn, J. M., & Lindsay, B. R. (2023, July 17). Federal disaster assistance for businesses: Summaries and policy options (CRS Report No. R47631). Congressional Research Service.

Nevada Department of Business and Industry. (n.d.). Grants and incentives.

Ready.gov. (n.d.). Plan for and protect your business. U.S. Department of Homeland Security.

SCORE. (n.d.). About SCORE.

U.S. Small Business Administration. (2025). Disaster assistance for businesses.

Wasserman, N. (2008, February). The founder’s dilemma. Harvard Business Review.