6.4.1: Chapter Introduction

- Page ID

- 59259

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)In August 2008, CEO Mike Lenahan was finding growth to be challenging for his firm Resource Recovery Corporation (RRC). RRC is a small competitor in the recycling industry, geographically constrained with a pool of about 30 customers, all of whom are foundries. Foundries use tons of sand weekly for moldings and then need to dispose of it. RRC was created in the interest of reducing disposal cost and identifying reuses of the spent sand and other materials. The company had very close relationships with this customer base, in part because in 1991, about 15 of these 30 foundries had actually banded together to form RRC, as a low-cost competitive alternative to the large recycling firms, including Waste Management. These large competitors had more recently constrained RRC’s growth.

As part of a 3-Circle project, Mike’s executive team undertook interviews with customers to learn more about how they valued their service versus the service of competitors. Issues of cost levels, aspects of the firm’s recycling methods, speed of service, reliability, and size of the company all came up in the discussions with customers. Many of the customer assessments were positive on these dimensions. When it came to size of the company, RRC executives felt that their small size was a significant advantage to them in the eyes of the customer. Mike and his team believed that small meant fast on the feet and responsive, a major advantage over very large competitors slowed down by corporate hierarchy. However, when they explored the deeper meaning of “firm size” to customers, they were stunned. Instead of seeing RRC’s firm size as a strength, customers saw it as a weakness. When Mike and his team dug into this assessment, they found customers to be concerned about the long-term viability of a small firm in an industry in which four large competitors have over half of the market share. In other words, the sentiment they heard was “we know you’re good and we love your cost model, but we don’t know if you are going to be around in five years.”

RRC quickly responded to these concerns and, within a month, increased its sales at a level that represented 10% of the company’s annual sales. This was accomplished by conducting a strategic review of all the capabilities, resources, and assets the firm had access to that signaled longer-term stability. They had recently firmed up a variety of resource commitments and external partnerships and had asset investments and customer relationships that reflected a clear external commitment to the firm into the future. The RRC team then developed a sales strategy that focused customers’ attention on the strength of these resource commitments and relationships, and returned to these customers. On top of an already compelling cost model, this allowed the team to land an account that had been sitting on the fence for some time, and provided a robust piece of revenue that has helped stabilize the firm in more recent recessionary times.

Mike Lenahan runs a smart company that is very close to its customers. Yet in these relationships—and unbeknownst to RRC—customers’ persistent belief that “small equals unstable” had existed for some time, limiting their sales growth. Is it uncommon for executives to feel confident that they know customers but to then get blindsided by unexpected customer assessments? In 3-Circle projects with over 200 executives, we have found the majority indicating surprise at the insights obtained. Most managers initially believe that they have a reasonable, intuitive understanding of the value customers seek. Yet with deeper discussions with customers, they very frequently discover insights that materially improve growth strategies.

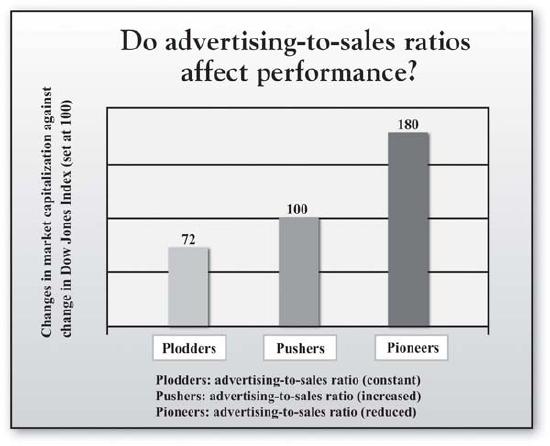

But can we get a broader sense of the payoffs from deeper understanding of customer value? In an important research study that provides the foundation for his Momentum Effect model of growth, Jean-Claude Larreche of INSEAD examined the financial results for 367 of the largest worldwide companies for the 20-year period from 1985 through 2004. Some of the most interesting discoveries from the research focused upon the 119 leading consumer goods firms.Larreche (2008a, 2008b). Consumer firms are the focus here because they were the largest category of firms in Larreche’s study. Larreche sorted these consumer firms into three groups: those firms that increased, those that decreased, and those that held constant advertising expenditures over that time period (where advertising spending was measured by the advertising-to-sales ratio, or A/S). Consistent with a traditional view, more intensive advertising was found to produce positive financial results, as measured by improvement of firm value. The group that increased its A/S ratio over time (labeled pushers by Larreche) experienced improvement in market capitalization that was 28% higher than the firms who held their A/S ratios roughly constant (labeled plodders). Improvement in market capitalization over time for the pushers matched the average change in the Dow Jones index for the same time period, indicating that “marketing as pushing” is a reasonably successful strategy. Figure \(\PageIndex{1}\) shows the results for these two groups as the first two bars, indicating that increasing advertising intensity leads to greater stock market value.

However, note that there is a third group that Larreche identified: the firms that actually reduced their advertising spending over time. Based on the apparent positive effect of greater advertising intensity for pushers, we might expect that this third group would significantly underperform over time. Yet they not only beat the Plodders by 108%, they also substantially outperformed the pushers (by 80%)! This stunning result has a simple interpretation. It is not that these firms found advertising ineffective, reduced it, and subsequently increased performance. Instead, it is that there is another element of strategy to consider: the excellence of their products and services. This third group—labeled the pioneers—includes firms that design products and services with such compelling and unique value that they create their own sales momentum. In short, demand for these firms’ products and services is less a function of advertising and communications and more a function of how well they deliver the value that customers seek. In essence, these firms allow their actual offerings to do the talking.

So where do these more compelling offerings come from? Whether the firm is Apple, Starbucks, Southwest Airlines, FedEx, or Mike Lenahan’s Resource Recovery Corporation, the compelling offerings come from a deeper understanding of customer value than competitors have. This chapter defines and explores customer value. We first consider the fundamental dimensions of customer value and then consider how studying these dimensions can help in understanding competitive dynamics and growth strategy. We further consider that there are important growth opportunities in thinking more broadly and deeply about customer value than competitors do. The last section of the chapter overviews an approach to engaging the study of customer value.