4.9.7: Controlling

- Page ID

- 58989

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)What you’ll learn to do: explain why control is an essential part of effective management, and outline the steps of the control process

In this section you’ll learn about the control function of management and become familiar with the steps of the control process.

Learning Objectives

- Explain what SMART objectives are

- Outline the steps of the control process

Controlling

What Is Control?

Consider the two images in Figure \(\PageIndex{1}\). . . one with control and one without. Think of the two parking lots as two different organizations. What you can see is that one has management controls in place, and the other . . . well, you can tell how that’s working out. In the second photo no one is in charge of controlling the actions and activities of the employees within the company—it’s a free-for-all.

It might seem attractive, at first, to work for a company where people aren’t telling you what to do, how to do it, or when things are due. But it wouldn’t take too long, probably, for all that freedom to feel like chaos. In this next section we’ll focus on the control function of management to better understand how it helps people and organizations achieve goals and objectives.

In business or management context, control is the activity of observing a given organizational process, measuring performance against a previously established metric, and improving it where possible. Organizations are made up of operational processes and systems, each of which can be iterated upon and optimized. At the upper-managerial level, control revolves around setting strategic objectives for the short and long term, as well as measuring overall organizational success. Developing methods for optimizing operational processes is often done at the mid-managerial level. The mid-level manager measures success within his or her span of control—which could be a division, a region, or a particular product. The line manager is then responsible for controlling the actions of the workers to ensure that activities are carried out in a way that optimizes outcomes and outputs. He or she will measure the success of individual workers, work teams, or even a shift. What managers up and down the organizational chart have in common is that they all use the same process for carrying out the control function of management.

The process of control usually consists of the following four parts:

- setting standards,

- measuring performance against those standards,

- analyzing performance, and

- taking corrective action.

Take special note of the language that we use when we talk about the control function—process! Controlling the activities within an organization is a continuous process that resembles navigation. In order to reach a destination, a ship navigator sets a course and then constantly checks the headings—if the ship has drifted off course, the navigator makes the necessary corrections. This cycle of check-and-correct, check-and-correct happens over and over to keep the ship on course and get it to where it’s going. Similarly, the controlling function in business is a process of repeatedly checking and correcting until standards and objectives are met.

Another feature of the control process is that it’s designed to be proactive. The idea is for managers to intervene before costly or damaging problems occur, rather than waiting and hoping for the best. It’s better to take corrective action when you’re drifting off course than try to salvage your ship after you’ve crashed into a rock. The benefit to managers and organizations of a forward-looking, proactive approach is that it reduces customer complaints, employee frustration, and waste.

Setting Standards and Objectives

Organizational standards and objectives are important elements in any plan because they guide managerial decision making. Performance standards and objectives may be stated in monetary terms—such as revenue, costs, or profits—but they may also be set in other terms, such as units produced, number of defective products, levels of quality, or degree of customer satisfaction.

Peter Drucker suggests that operational objectives should be SMART, which means specific, measurable, achievable, realistic, and time constrained: [1]

- An operational objective should be specific, focused, well defined, and clear enough that employees know what is expected. A specific objective should identify the expected actions and outcomes. This helps employees stay on track and work toward appropriate goals.

- An operational objective should be measurable and quantifiable so people can assess whether it has been met or not. For example, “increase annual sales revenue by 10 percent” is a measurable objective.

- An objective needs to be achievable. It’s important for all the stakeholders—especially the employees doing the work—to agree that the objective can be met. Unachievable objectives can be damaging to employee trust and morale.

- An objective should be realistic as well as ambitious. It should take into account the available resources and time.

- Lastly, an objective should be time constrained. Having a deadline can help increase productivity and prevent the work from dragging on.

It’s important to get employee input during the process of developing operational objectives, as it may be challenging for employees to understand or accept them after they’re set. After determining appropriate operational objectives for each department, plans can be made to achieve them.

Measuring Performance

Performance measurement is the process of collecting, analyzing, and/or reporting information regarding the performance of an individual, group, organization, system, or component. The ways in which managers and organizations measure performance vary greatly—there is no single systemic approach that fits all companies or conditions. The most important element of measuring performance is to do them at regular intervals and/or when particular milestones are reached. The best processes for measuring performance provide information in time for day-to-day decisions.

The rubric for measuring organizational performance is called a performance metric. These metrics measure an organization’s behavior, activities, and performance. In order to be effective, the metric should relate to a range of stakeholder needs, including those of customers, shareholders, and employees. Metrics may be finance based or they may focus on some other measure of performance, such as customer service or customer perceptions of product value. For example, in call centers, performance metrics help capture internal productivity and the quality of service. Typical metrics might be calls answered, calls abandoned, average service time, and average wait time.

In general, performance metrics usually involves the following:

- Establishing critical processes/customer requirements

- Identifying specific, quantifiable outputs of work

- Establishing targets against which results can be scored

Analyzing Performance

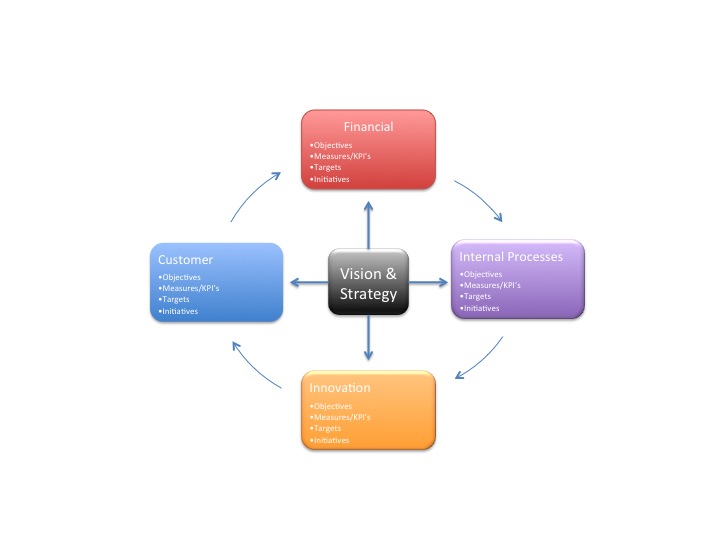

Once performance has been measured, managers must analyze the results and evaluate whether objectives have been met, efficiencies achieved, or goals obtained. The means by which performance is analyzed vary among organizations; however, one tool that has gained widespread adoption is the balanced scorecard. A balanced scorecard is a semi-standardized strategic management tool used to analyze and improve key performance indicators within an organization. The original design of this balanced scorecard has evolved over the last couple decades and now includes a number of other variables—mostly where performance intersects with corporate strategy. Corporate strategic objectives were added to allow for a more comprehensive strategic planning exercise. Today, this second-generation balanced scorecard is often referred to as a “strategy map,” but the conventional “balanced scorecard” is still used to refer to anything consistent with a pictographic strategic management tool.

The following four perspectives are represented in a balanced scorecard:

- Financial: includes measures focused on the question “How do we look to shareholders?”

- Customer: includes measures focused on the question “How do customers perceive us?”

- Internal business processes: includes measures focused on the question “What must we excel at?”

- Learning and growth: includes measures focused on the question “How can we continue to improve and create value?”

Managers generally use this tool to identify areas of the organization that need better alignment and control vis-à-vis the broader organizational vision and strategy. The balanced scorecard brings each of an organization’s moving parts into one view in order to improve synergy and continuity between functional areas.

Taking Corrective Action

Once the cause of nonperformance or underperformance has been identified, managers can take corrective action. Corrective action is essentially a planned response aimed at fixing a problem. At this stage of the controlling process, problem-solving is key.

The first step managers must take is to accurately identify the problem, which can sometimes be hard to distinguish from its symptoms or effects. Collecting information and measuring each process carefully are important prerequisites to pinpointing the problem and taking the proper corrective action. Attempts at corrective action are often unsuccessful because of failures in the problem-solving process, such as not having enough information to isolate the real problem, or the presence of a manager or decision maker who has a stake in the process and doesn’t want to admit that his department made a mistake. Another reason why the problem-solving process can run aground is if the manager or decision maker was nevery properly trained to analyze a problem.

Once the problem is identified, and a method of corrective action is determined, it needs to be implemented as quickly as possible. A map of checkpoints and deadlines, assigned to individuals in a clear and concise manner, facilitates prompt implementation. In many ways, this part of the control process is very much a process itself. Its steps can vary greatly depending on the issue being addressed, but in all cases it should be clear how the corrective actions will lead to the desired results.

Next, it’s important to schedule a review and evaluation of the solution. This way, if the corrective action doesn’t bring the desired results, further action can be taken swiftly—before the organization falls even further behind in meeting its goals. Organizations may also decide to discuss a problem and potential solutions with stakeholders. It’s useful to have some contingency plans in place, as employees, customers, or vendors may have unique perspectives on the problem. Gaining a broader view can sometimes help management arrive at a more effective solution.

A manager must use a wide range of skills to navigate the management process well. This journey begins with sound planning, based on a set of SMART goals and objectives. The manager leads both people and processes, using a blend of leadership and management styles appropriate to the situation. If the manager has done a good job of placing the right people in the right places, and has implemented sound standards and performance metrics, then she is well-positioned to take corrective action where needed. Regardless of whether the task is to get a customer’s order assembled and shipped on time or expand into a new market, the functions of the manager remain unchanged.