4.4.2: Market

- Page ID

- 58943

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)What you’ll learn to do: explain what money is and what makes it useful

When we think of money, the paper bills in our wallet or the coins that are in our pockets come to mind. But money is much more than that, and how we define money determines where and how we use it to obtain the goods and services that businesses offer the consumer. In this section we’ll look at what money is, why it’s useful, and what may be the future of money.

Learning Objectives

- Discuss the advantages of using money versus barter

- Discuss alternatives to traditional currency used today

What Is Money?

Money is really anything that people use to pay for goods and services and to pay people for their work. Historically, money has taken different forms in different cultures—everything from salt, stones, and beads to gold, silver, and copper coins and, more recently, virtual currency has been used. Regardless of the form it takes, money needs to be widely accepted by both buyers and sellers in order to be useful.

Money is really anything that people use to pay for goods and services and to pay people for their work. Historically, money has taken different forms in different cultures—everything from salt, stones, and beads to gold, silver, and copper coins and, more recently, virtual currency has been used. Regardless of the form it takes, money needs to be widely accepted by both buyers and sellers in order to be useful.

Barter and the Double Coincidence of Wants

To understand the usefulness of money, we must consider what the world would be like without money. How would people exchange goods and services? Economies without money typically engage in the barter system. Barter—literally trading one good or service for another—is highly inefficient for trying to coordinate the trades in a modern advanced economy. In an economy without money, an exchange between two people would involve a double coincidence of wants, a situation in which two people each want some good or service that the other person can provide. For example, if a hairstylist wants a pair of shoes, she must find a shoemaker who has a pair of shoes in the correct size and who is willing to exchange the shoes for a certain number of hairdos. Such a trade is likely to be difficult to arrange. Think about the complexity of such trades in a modern economy, with its extensive division of labor that involves thousands upon thousands of different jobs and goods.

Another problem with the barter system is that it doesn’t allow people to easily enter into future contracts for the purchase of many goods and services. For example, if the goods are perishable, it may be difficult to exchange them for other goods in the future. Imagine a farmer wanting to buy a tractor in six months using a fresh crop of strawberries. Also, while the barter system might work all right in small economies, it will keep those economies from growing. The time that individuals might otherwise spend producing goods and services and enjoying leisure time is spent bartering.

Functions of Money

Money solves the problems created by the barter system. First, money serves as a medium of exchange, which means that money acts as an intermediary between the buyer and the seller. Instead of exchanging hairdos for shoes, the hairstylist now exchanges hairdos for money. This money is then used to buy shoes. To serve as a medium of exchange, money must be very widely accepted as a method of payment in the markets for goods, labor, and financial capital.

In addition, money needs to have the following properties:

- It must be divisible—that is, easily divided into usable quantities or fractions. A $5 bill, for example, is equal to five $1 bills. If something costs $3, you don’t have to tear up a $5 bill; you can pay with three $1 bills.

- It must be portable—easy to carry; it can’t be too heavy or bulky.

- It must be durable. It can’t fall apart or wear out after a few uses.

- It must be difficult to counterfeit. It won’t have much value if people can make their own.

Second, money must serve as a store of value. Consider the barter between the hairstylist and shoemaker again. The shoemaker risks having his shoes go out of style, especially if he keeps them in a warehouse for future use—their value will decrease with each season. Shoes are not a good store of value. Holding money is a much easier way of storing value. You know that you don’t need to spend it immediately, because it will still hold its value the next day or the next year. This function of money doesn’t require that money is a perfect store of value. In an economy with inflation, money loses some buying power each year, but it remains money.

Third, money serves as a unit of account, which means that it’s the ruler by which other values are measured. For example, a hairstylist may charge $30 to style someone’s hair. That $30 can buy two shirts (but probably not a pair of shoes). Money acts as a common denominator, an accounting method that simplifies thinking about trade-offs.

So money serves all of these functions—it’s a medium of exchange, store of value, and unit of account.

Uninscribed electrum coin from Lydia, 6th century BCE.

Commodity versus Fiat Money

Commodity money consists of objects that have value in themselves as well as value in their use as money. Gold, for example, has been used throughout the ages as money, although today it is not used as money but rather is valued for its other attributes. Gold is a good conductor of electricity and is used in the electronics and aerospace industry. Gold is also used in the manufacturing of energy efficient reflective glass for skyscrapers and is used in the medical industry as well. Of course, gold also has value because of its beauty and malleability in the creation of jewelry.

As commodity money, gold has historically served its purpose as a medium of exchange, a store of value, and as a unit of account. Commodity-backed currencies are dollar bills or other currencies with values backed up by gold or another commodity held at a bank. During much of its history, the money supply in the United States was backed by gold and silver. Interestingly, antique dollars dated as late as 1957 have “Silver Certificate” printed above the portrait of George Washington, as shown below. This meant that the holder could take the bill to the appropriate bank and exchange it for a dollar’s worth of silver.

A Silver Certificate and a Modern U.S. Bill. Until 1958, silver certificates were commodity-backed money—backed by silver, as indicated by the words “Silver Certificate” printed on the bill. Today, U.S. bills are backed by the Federal Reserve, but as fiat money.

As economies grew and became more global in nature, the use of commodity monies became more cumbersome. Countries moved toward the use of fiat money. Fiat money is legal tender whose value is backed by the government that issued it. The United States’ paper money—like the dollar bill, for instance—carries this statement: “This note is legal tender for all debts, public and private.” In other words, by government decree, if you owe a debt, then legally speaking, you can pay that debt with the U.S. currency, even though it’s not backed by a commodity. The only backing of our money is widespread faith and trust that the currency has value—and nothing more.

The following video discusses some additional characteristics of money:

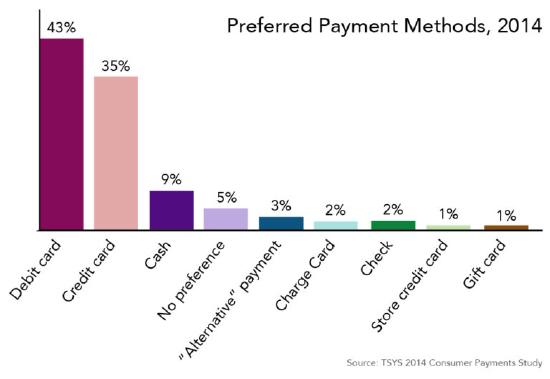

Alternatives to Traditional Currency

Whoever said that “cash is king” hasn’t been paying attention to how consumers choose to pay for their purchases, particularly in developed economies. Take a look at the following chart:

Is a cashless future in the cards? A 2013 MasterCard report found that, in 2011, cashless payments made up 66 percent of global spending. Consumers in Belgium, France, and Canada used cash the least in 2011, as cashless payments made up 93 percent, 92 percent, and 90 percent of payments respectively. In the United States, 80 percent of payments were cashless in 2011.

Consumers expect to make fewer cash payments in the future, while also cutting back on credit- and debit-card use in favor of other forms of payments. In an Accenture survey, 66 percent of North Americans said they used cash daily or weekly in 2014 while only 54 percent expected to do so by 2020.

Money is an abstraction built on trust. As such, alternatives to the most tangible form of money—currency or cash—and its replacement with cashless payments have become possible. In this new emerging landscape, no transaction requires money in the form of notes and coins, and value can be exchanged through the transfer of information between transacting parties. There have been multiple waves of such alternatives.

Established alternatives to cash include checks, credit cards, debit cards, and prepaid debit cards. More recently, innovative options have sprung up that not only threaten to imperil the ubiquity of cash but also upend the traditional payment ecosystem. These include smartphone-enabled credit-card acquirers, such as Square, and Automated Clearing House or ACH acquirers, such as PayPal and Dwolla. And then there are even more ambitious alternatives to cash that have been proposed, such as Bitcoin, a Web-based cryptocurrency.

Unlike traditional money, such alternatives do not derive their value from government fiat—i.e., the government has not established their legitimacy or value. Each of these alternatives has an evolved network within which it is uniformly accepted as a means of payment; the more established alternatives, of course, have the widest networks.[1]

We will examine this trend further by taking a look at Bitcoin and Mobile Commerce.

Bitcoin

Today, there are more than seven hundred digital currencies in existence. Entering the marketplace is undertaken by so many due to the low cost of entry and the profit opportunity. In 2014, the European Banking Authority defined virtual currency as “a digital representation of value that is neither issued by a central bank nor a public authority, nor necessarily attached to a fiat currency, but is accepted by natural or legal persons as a means of payment and can be transferred, stored, or traded electronically.” The first and most widely known instance of such digital, virtual, or cryptocurrency is Bitcoin.

Today, there are more than seven hundred digital currencies in existence. Entering the marketplace is undertaken by so many due to the low cost of entry and the profit opportunity. In 2014, the European Banking Authority defined virtual currency as “a digital representation of value that is neither issued by a central bank nor a public authority, nor necessarily attached to a fiat currency, but is accepted by natural or legal persons as a means of payment and can be transferred, stored, or traded electronically.” The first and most widely known instance of such digital, virtual, or cryptocurrency is Bitcoin.

Bitcoin Background

Bitcoin, a peer-to-peer digital currency or cryptocurrency, operates without the involvement of traditional financial institutions, and it provides a direct digital alternative to physical currencies. Bitcoin transactions take place online directly between the buyer and seller, with each transaction having a unique encryption. Transactions are recorded on a decentralized public ledger available for network users to verify valid transactions. Special users on the network (“miners”) oversee this verification process. After verifying a block of transactions, miners are paid with twenty-five newly generated Bitcoins and the transactions are processed and approved; this is how the total number of Bitcoins grows. The number in circulation as of January 2015 was approximately 13.7 million, with the maximum set at 21 million. As of April 2015, their total value was $3 to $4 billion.

Governments worldwide generally do not yet see it and other digital currencies as a destabilizing “threat,” and some scholars have argued that it may best be seen as a speculative investment. Bitcoin has certainly had its ups and downs: As of April 1, 2015, its value stood at $242 per Bitcoin, after a January 14 low of $177 and a March 11 high of $296. The currency has also had a long run of troubles with hackers and fraud, most spectacularly in 2014 when the exchange Mt. Gox declared bankruptcy after Bitcoins worth $460 million at the time were apparently stolen. Bitcoin’s decentralized model and degree of anonymity have also raised concerns over its use in illegal money transfers, fueling potential illicit commerce across the “dark Web” and on sites such as Silk Road.

The organization Bitcoin.org, meanwhile, touts the currency’s potential for opening up a “whole new platform for innovation”:

Advantages and Disadvantages

A 2015 Congressional Research Service (CRS) report, “Bitcoin: Questions, Answers and Analysis of Legal Issues, explores the following technical, functional, and legal issues associated with Bitcoin—and, by extension, all virtual currencies.

Bitcoin advantages:

- Lower transaction costs: Because Bitcoin operates without a third-party intermediary, merchants are able to avoid the fees traditionally charged by payment systems such as credit cards.

- The possibility of increased privacy: Bitcoin provides a heightened degree of privacy for purchases and transactions, though by the system’s nature, a complete list of all transactions is forever recorded to each user’s encrypted identity.

- Protection from inflation: Since Bitcoin’s circulation is not linked to currency or government regulation, it is not subject to standard inflation. However, it more than makes up for this in volatility.

Bitcoin disadvantages:

- Severe price volatility: The value of a Bitcoin is determined by supply and demand and, as a result, can fluctuate rapidly. The value was as high as $1,100 in December 2013, then hit a low of $177 in January 2015. This extreme fluctuation is more characteristic of a commodity than a currency.

- Not legal tender: Debtors are not required to accept it, and without any formal backing other than the computer program to which it is linked, Bitcoin can be seen as an “unattractive vehicle” for holding and accumulating wealth.

- Uncertain security against theft and fraud: While the counterfeiting of Bitcoins is allegedly impossible, the system has at times found itself vulnerable to large security breaches and cyberattacks. Most recently, Bitstamp, a large European Bitcoin exchange, lost 19,000 Bitcoins (valued at about $5 million) in a digital security breach. This follows the massive problems with Mt. Gox in 2014 and the collapse of other exchanges in 2011.

- Vulnerability of Bitcoin “wallets”: Purchased or mined Bitcoins are stored in a digital wallet on the user’s computer or mobile device, and digital keys can be lost, damaged, or stolen. Paper or offline storage is an option, but it’s not always practiced.

Federal banking regulators have yet to issue guidance or regulations governing how banks are to deal with Bitcoins. In a February 2014 statement, Federal Reserve chair Janet Yellen said: “Bitcoin is a payment innovation that’s taking place outside the banking industry. . . . There’s no intersection at all, in any way, between Bitcoin and banks that the Federal Reserve has the ability to supervise and regulate.” Some state financial authorities have taken steps to devise regulations, with New York’s Department of Financial Services (NYDFS) in the lead.

The responsibility to oversee digital currency falls upon Congress. As of now, Congressional actions remain in the exploratory phase. The tax code lacks clarity on how such currency should be treated: Is it digital currency, property, barter, or foreign currency? Early concerns have focused more on tackling consumer-protection issues than tax ambiguities, and as a result, the Consumer Financial Protection Bureau has become involved regarding questions related to Bitcoin.

The following video explains further some of the gray areas in which this virtual currency is operating.

Whether it’s Bitcoin or another cryptocurrency, the fact that more than seven hundred of these unregulated digital currencies have emerged in just the last two years is just one more indication that consumers may be breaking off their longstanding love affair with traditional cash.

Mobile Commerce and Mobile Payment Systems

The term mobile commerce was first coined in 1997 by Kevin Duffey at the launch of the Global Mobile Commerce Forum to mean “the delivery of electronic commerce capabilities directly into the consumer’s hand, anywhere, via wireless technology.” Many think of mobile commerce as “a retail outlet in your customer’s pocket.”

Mobile commerce is worth US$230 billion annually, with Asia representing almost half of the market, and it’s expected to reach US$700 billion in 2017. According to BI Intelligence, in January 2013, 29 percent of mobile users have now made a purchase with their phones. Walmart estimated that 40 percent of all visits to their Internet shopping site in December 2012 was from a mobile device. Bank of America projected that $67.1 billion in purchases would be made from mobile devices by European and U.S. shoppers in 2015.

Mobile Payment

Mobile payment, also referred to as mobile money, mobile money transfer, and mobile wallet, generally refers to payment services operated under financial regulation and performed from or via a mobile device. Instead of paying with cash, check, or credit cards, a consumer can use a mobile phone to pay for a wide range of services and digital or hard goods. Although the concept of using non-coin-based currency systems has a long history, only recently has the technology to support such systems become widely available.

Mobile payment is being adopted all over the world in different ways. In 2008, the combined market for all types of mobile payments was projected to reach more than $600 billion globally by 2013, which would be double the figure as of February, 2011. The mobile payment market for goods and services, excluding contactless Near Field Communication or NFC transactions and money transfers, exceeded $300 billion globally in 2013. Investment on mobile money services is expected to grow by 22.2 percent during the next two years across the globe. It will result in revenue share of mobile money reaching up to 9 percent by 2018. Asia and Africa will observe significant growth for mobile money, with technological innovation and focus on interoperability emerging as prominent trends by 2018.

In developing countries, mobile payment solutions have been deployed as a means of extending financial services to communities known as the “unbanked” or “underbanked,” which are estimated to represent as much as 50 percent of the world’s adult population, according to Financial Access’s 2009 Report “Half the World is Unbanked.”

Forms of Mobile Payment

Apple Pay is a mobile payment service that lets certain Apple mobile devices make payments at retail and online checkout. It digitizes and replaces the credit or debit magnetic stripe card transaction at credit card terminals. The service lets Apple devices wirelessly communicate with point of sale systems using a near field communication (NFC) antenna, a “dedicated chip that stores encrypted payment information” (known as the Secure Element), and Apple’s Touch ID and Passbook.

The service keeps customer payment information private from the retailer, and creates a “dynamic security code [ . . .] generated for each transaction.” Apple added that they would not track usage, which would stay between the customers, the vendors, and the banks. Users can also remotely halt the service on a lost phone via the Find My iPhone service.

Google Wallet is a mobile payment system developed by Google that allows its users to store debit cards, credit cards, loyalty cards, and gift cards among other things, as well as redeeming sales promotions on their mobile phone. Google Wallet can use near field communication (NFC) to “make secure payments fast and convenient by simply tapping the phone on any PayPass-enabled terminal at checkout.”

Where this new technology will lead the world economy and what its impact on the existing monetary system will be remain to be seen, but we are certain it will continue to evolve rapidly!

- Chakravorti, B., & Mazzotta, B. (2013, September). The Cost of Cash in the United States. Retrieved September 8, 2016, from fletcher.tufts.edu/CostofCash...icrosites/Cost of Cash/CostofCashStudyFinal.pdf ↵