15.8: Crafting Your Balanced Scorecard

- Page ID

- 4860

Learning Objectives

- Understand the Balanced Scorecard concept.

- See how the Balanced Scorecard integrates nonfinancial and financial controls.

- Be able to outline a personal Balanced Scorecard.

An Introduction to the Balanced Scorecard

You have probably learned a bit about Balanced Scorecards already from this book or other sources. The Balanced Scorecard was originally introduced to integrate financial and nonfinancial controls in a way that provided a balanced understanding of the determinants of firm performance. It has since evolved into a strategic performance management tool of sorts because it helps managers identify and understand the way that operating controls are tied to strategic controls, and ultimately, firm performance. In this broader sense, a Balanced Scorecard is a control system that translates an organization’s vision, mission, and strategy into specific, quantifiable goals and to monitor the organization’s performance in terms of achieving these goals.

According to Robert S. Kaplan and David P. Norton, the Balanced Scorecard approach “examines performance in four areas. Financial analysis, the most traditionally used performance indicator, includes assessments of measures such as operating costs and return-on-investment. Customer analysis looks at customer satisfaction and retention. Internal analysis looks at production and innovation, measuring performance in terms of maximizing profit from current products and following indicators for future productivity. Finally, learning and growth analysis explores the effectiveness of management in terms of measures of employee satisfaction and retention and information system performance (Kaplan & Norton, 2001).”

Figure 15.10

Just as tasters can rate a wine on numerous dimensions, the Balanced Scorecard integrates a variety of measures of organizational quality and performance.

fs999 – Good Wine – CC BY-NC-ND 2.0.

Whereas the scorecard identifies financial and nonfinancial areas of performance, the second step in the scorecard process is the development of a strategy map. The idea is to identify key performance areas in learning and growth and show how these cascade forward into the internal, customer, and financial performance areas. Typically, this is an iterative process where managers test relationships among the different areas of performance. If the organization is a for-profit business like IBM, then managers would want to be able to show how and why the choice made in each area ultimately led to high profitability and stock prices.

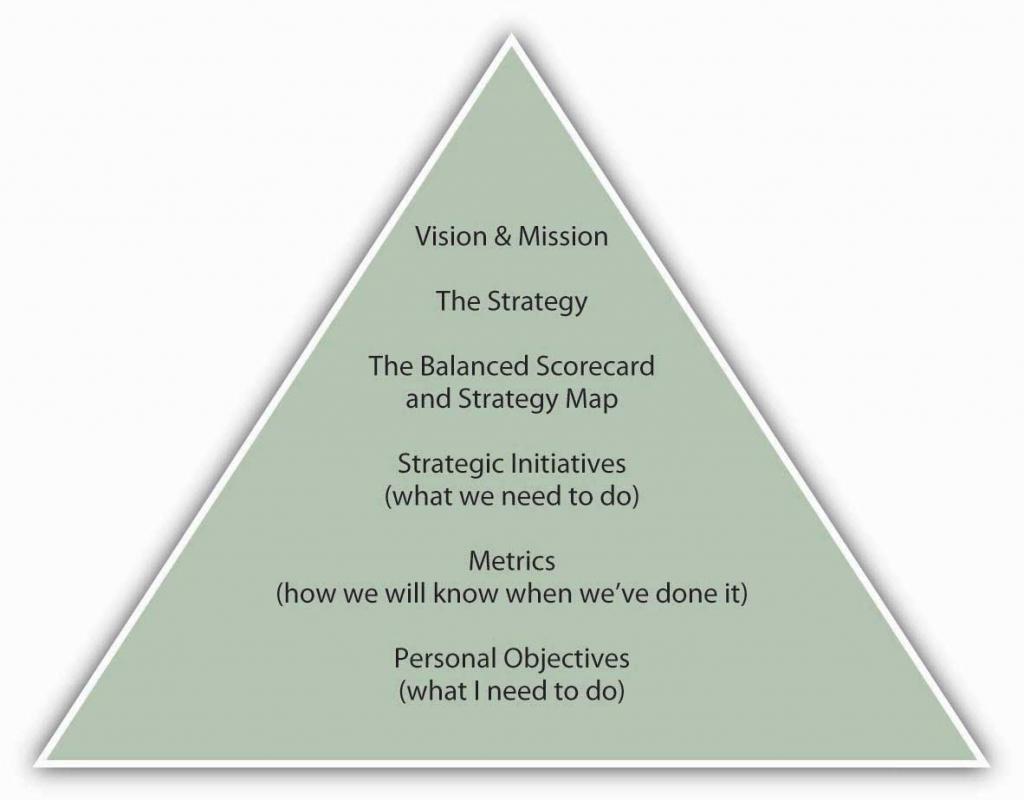

Figure 15.11 The Balanced Scorecard Hierarchy

With the scorecard and strategy map in hand, managers then break broad goals down successively into vision, strategies, strategic initiatives, and metrics. As an example, imagine that an organization has a goal of maintaining employee satisfaction in its vision and mission statements. This would be the organization’s vision in the domain of learning and growth, since employee satisfaction is indirectly related to financial performance. Strategies for achieving that learning and growth vision might include approaches such as increasing employee-management communication. Initiatives undertaken to implement the strategy could include, for example, regularly scheduled meetings with employees. Metrics could include quantifications of employee suggestions or employee surveys. Finally, managers would want to test their assumptions about the relationship between employee satisfaction and the downstream areas such as internal, customer, and financial performance. For example, satisfied employees may be more productive and less likely to quit (internal), which leads to better products or services and customer relations (customer), which leads to lower employee recruiting and training costs and greater sales and repeat sales (financial). This sequence of causal relationships is summarized in the following figure.

Figure 15.12 The Strategy Map: A Causal Relationship between Nonfinancial and Financial Controls