17.2: Cash Flows from Operating Activities- The Direct Method

- Page ID

- 4490

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Identify the two methods available for reporting cash flows from operating activities.

- Indicate the method of reporting cash flows from operating activities that is preferred by FASB as well as the one that is most commonly used.

- List the steps to be followed in determining cash flows from operating activities.

- List the income statement accounts that are removed entirely in computing cash flows from operating activities and explain that procedure when the direct method is applied.

- Identify common “connector accounts” that are used to convert accrual accounting figures to the change taking place in the cash balance as a result of these transactions.

- Compute the cash inflows and outflows from common revenues and expenses such as sales, cost of goods sold, rent expense, salary expense, and the like.

Question: The net cash inflow or outflow generated by operating activities is especially significant information to any person looking at an organization’s financial health and future prospects. According to FASB, that information can be presented within the statement of cash flows by either of two approaches: thedirect methodor theindirect method. The numerical amount of the change in cash resulting from the company’s daily operations is not impacted by this reporting choice. The increase or decrease in cash is a fact that will not vary based on the manner of presentation. Both methods arrive at the same total. The informational value to decision makers, though, is potentially affected by the approach selected.

FASB has indicated a preference for the direct method. In contrast, reporting companies (by an extremely wide margin) have continued to use the more traditional indirect method. Thus, both will be demonstrated here. The direct method seems a bit easier to explain and will be discussed first. How is information presented when the direct method is selected to disclose a company’s cash flows from operating activities?

Answer: The direct method starts with the income statement for the period. Then, each of the separate figures is converted into the amount of cash received or spent in carrying on operating activities. “Sales,” for example, is turned into “cash collected from customers.” “Salary expense” and “rent expense” are recomputed as “cash paid to employees” and “cash paid to rent facilities.”

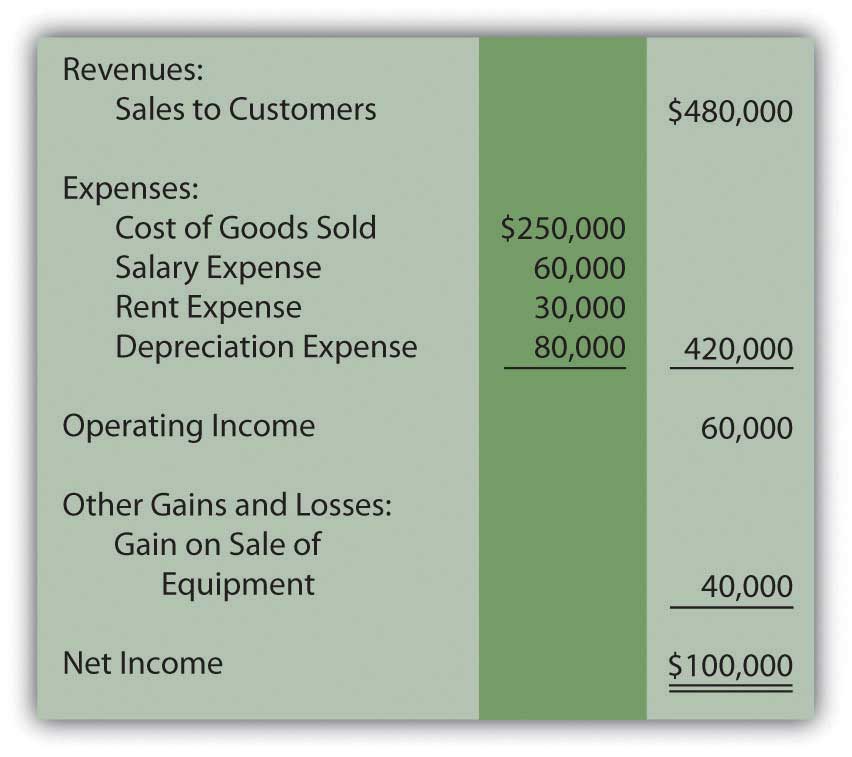

For illustration purposes, assume that that Liberto Company prepared the following income statement for the year ended December 31, Year One. This statement has been kept rather simple so that the conversion to cash flows from operating activities is not unnecessarily complex. For example, income tax expense has been omitted.

Figure 17.4 Liberto Company Income Statement Year Ended December 31, Year One