4.8: Accounting systems: From manual to computerize

- Page ID

- 48942

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)The manual accounting system with only one general journal and one general ledger has been in use for hundreds of years and is still used by some very small companies. Gradually, some manual systems evolved to include multiple journals and ledgers for increased efficiency. For instance, a manual system with multiple journals and ledgers often includes: a sales journal to record all credit sales, a purchases journal to record all credit purchases, a cash receipts journal to record all cash receipts, and a cash disbursements journal to record all cash payments. Still recorded in the general journal are adjusting and closing entries and any other entries that do not fit in one of the special journals. Besides the general ledger, such a system normally has subsidiary ledgers for accounts receivable and accounts payable showing how much each customer owes and how much is owed to each supplier. The general ledger shows the total amount of accounts receivable and accounts payable, but the details in the subsidiary ledgers allow companies to send bills to customers and pay bills to suppliers.

Another innovation in manual systems was the "one write" or pegboard system. By creating one document and aligning other records under it on a pegboard, companies could record transactions more efficiently. These systems permit the writing of a check and the simultaneous recording of the check in the cash disbursements journal. Even though some of these systems are still in use today, computers make them obsolete.

During the 1950s, companies also used bookkeeping machines to supplement manual systems. These machines recorded recurring transactions such as sales on account. They posted transactions to the general ledger and subsidiary ledger accounts and computed new balances. With the development of computers, bookkeeping machines became obsolete. They were quite expensive, and computers easily outperformed them. In the mid-1950s, large companies began using mainframe computers. Early accounting applications were in payroll, accounts receivable, accounts payable, and inventory. Within a few years, programs existed for all phases of accounting, including manufacturing operations and the total integration of other accounting programs with the general ledger. Until the 1980s, small and medium-sized companies either continued with a manual system, rented time on another company's computer, or hired a service bureau to perform at least some accounting functions.

|

|

MICROTRAIN COMPANY |

|

|

|

|

Trial Balance |

|

|

|

|

2010 December 31 |

|

|

|

Acct. |

|

|

|

|

No. |

Account Title |

Debits |

Credits |

|

100 |

Cash |

$ 8,250 |

|

|

103 |

Accounts Receivable |

6,200 |

|

|

107 |

Supplies on Hand |

900 |

|

|

108 |

Prepaid Insurance |

2,200 |

|

|

112 |

Prepaid Rent |

800 |

|

|

121 |

Interest Receivable |

600 |

|

|

150 |

Trucks |

40,000 |

|

|

151 |

Accumulated Depreciation—Trucks |

|

$ 750 |

|

200 |

Accounts Payable |

|

730 |

|

206 |

Salaries Payable |

|

180 |

|

216 |

Unearned Service Fees |

|

3,000 |

|

300 |

Capital Stock |

|

50,000 |

|

310 |

Retained Earnings |

|

4,290 |

|

|

|

$ 58,950 |

$ 58,950 |

Exhibit 24: Post closing trial balance

An accounting perspective:

Business insight

Imagine a company with an Accounts Receivable account and an Accounts Payable account in its general ledger and no Accounts Receivable Subsidiary Ledger or Accounts Payable Subsidiary Ledger. How would this company know to whom to send bills and in what amounts? Also, how would employees know for which suppliers to write checks and in what amounts? Such subsidiary records are necessary either on paper or in a computer file.

Here is how the general ledger and subsidiary ledgers might look:

|

|

Subsidiary Accounts Receivable Ledger |

|

General Ledger |

|

|

Subsidiary Accounts Payable Ledger |

|

|

JOHN JONES |

ACCOUNTS RECEIVABLE |

|

BELL CORPORATION |

||||

|

|

200 1 |

900 |

|

|

100 |

||

|

|

SYLVIA SMITH |

|

|

|

GRANGER CORPORATION |

||

|

|

300 1 |

|

ACCOUNTS PAYABLE |

|

|

600 |

|

|

|

|

|

1,000 |

|

|

||

|

JAMES WELLS |

|

|

|

|

WONG CORPORATION |

||

|

400 1 |

|

|

|

|

300 |

||

When a sale on account is made to John Jones, the debit is posted to both the control account, Accounts Receivable, in the General Ledger and the subsidiary account, John Jones, in the Subsidiary Accounts Receivable Ledger. Likewise, when a purchase on account is made from Bell Corporation, the credit is posted to both the control account, Accounts Payable, in the General Ledger and to the subsidiary account, Bell Corporation, in the Subsidiary Accounts Payable Ledger. At the end of the accounting period, the balances in each of the control accounts in the General Ledger must agree with the totals of the accounts in their respective subsidiary ledgers as shown above. A given company could have hundreds or even thousands of accounts in their subsidiary ledgers that show the detail not supplied by the totals in the control accounts.

A broader perspective:

Skills for the long haul

The decision has been made: You [Tracy] have opted to start your career by joining an international accounting firm. But you can not help wondering if you have the right skills both for short and long-term success in public accounting.

Most students understand that accounting knowledge, organizational ability and interpersonal skills are critical to success in public accounting. But it is important for the beginner to realize that different skills are emphasized at different points in a public accountant's career.

Let us examine the duties and skills needed at each level—Staff Accountant (years 1-2), Senior Accountant (years 3-4), Manager/ Senior Manager (years 5-11) and Partner (years 11+).

Staff accountant—Enthusiastic learner

Let us travel with Tracy as she begins her career at the staff level. At the outset, she works directly under a senior accountant on each of her audits and is responsible for completing audits and administrative tasks assigned to her. Her duties include documenting work papers, interacting with client accounting staff, clerical tasks and discussing questions that arise with her senior. Tracy will work on different audit engagements during her first year and learn the firm's audit approach. She will be introduced to various industries and accounting systems.

The two most important traits to be demonstrated at the staff level are (1) a positive attitude and (2) the ability to learn quickly while adapting to unfamiliar situations.

Senior accountant—Organizer and teacher

As a senior accountant, Tracy will be responsible for the day-to-day management of several audit engagements during the year. She will plan the audits, oversee the performance of interim audit testing and direct year-end field work. She will also perform much of the final wrap-up work, such as preparing checklists, writing the management letter and reviewing or drafting the financial statements. Throughout this process, Tracy will spend a substantial amount of time instructing and supervising staff accountants.

The two most critical skills needed at the senior level are (1) the ability to organize and control an audit and (2) the ability to teach staff accountants how to audit.

Manager/senior manager—General manager and salesperson

Upon promotion to manager, Tracy will begin the transformation from auditor to executive. She will manage several audits at one time and become active in billing clients as well as negotiating audit fees. She will handle many important client meetings and closing conferences. Tracy will also become more involved in the firm's administrative tasks. Finally, outside of her client service and administrative duties, Tracy will be evaluated to a large extent on her community involvement and ability to assist the partners in generating new business for the firm.

The two skills most emphasized at the manager level are (1) general management ability and (2) sales and communication skills.

Partner—Leader and expert

As a partner in the firm, Tracy will have many broad responsibilities. She will engage in high-level client service activities, business development, recruiting, strategic planning, office administration and counseling. Besides serving as the engagement partner on several audits, she will have ultimate responsibility for the quality of service provided to each of her clients. Although a certain industry or administrative function will become her specialty, she will often be called upon to perform a wide variety of audit and administrative duties when other partners have scheduling conflicts. She will be expected to serve as a positive example to those who work for her and will train others in her areas of expertise.

At the partnership level, what is looked for is leadership ability plus the ability to become an expert in a specific industry or administrative function.

In the meantime

Those planning on a public accounting career should do more than just learn accounting. To develop the needed skills, a broad education background in business and nonbusiness courses is required plus participation in extracurricular activities that promote leadership and communication skills. It is never too early to start building the skills for long-term success.

Source: Dana R. Hermanson and Heather M. Hermanson, New Accountant, January 1990, pp. 24-26, © 1990, New DuBois Corporation.

The development of the personal computer (PC) in 1976 and its widespread use a decade later drastically changed the accounting systems of small and medium-sized businesses. The number and quality of accounting software packages for PCs and the power of PCs quickly increased. Soon small and medium-sized businesses could maintain all accounting functions on a PC. By the 1990s, the cost of PCs and accounting software packages had decreased significantly, accounting software packages had become more user-friendly, and computer literacy had increased so much that many very small businesses converted from manual to computerized systems. However, some small business owners still use manual systems because they are familiar and meet their needs, and the persons keeping the records may not be computer literate.

Your knowledge of the basic manual accounting system described in these first four chapters enables you to better understand a computerized accounting system. The computer automatically performs some of the steps in the accounting cycle, such as posting journal entries to the ledger accounts, closing the books, and preparing the financial statements. However, if you understand all of the steps in the accounting cycle, you will better understand how to use the resulting data in decision making.

An accounting perspective:

The impact of technology

Results from a recent survey of 1,400 chief financial officers (CFOs) indicate that tomorrow's accounting professionals will be called upon to bridge the gap between technology and business. With the rise of integrated accounting and information systems, technical expertise will go hand in hand with general business knowledge.

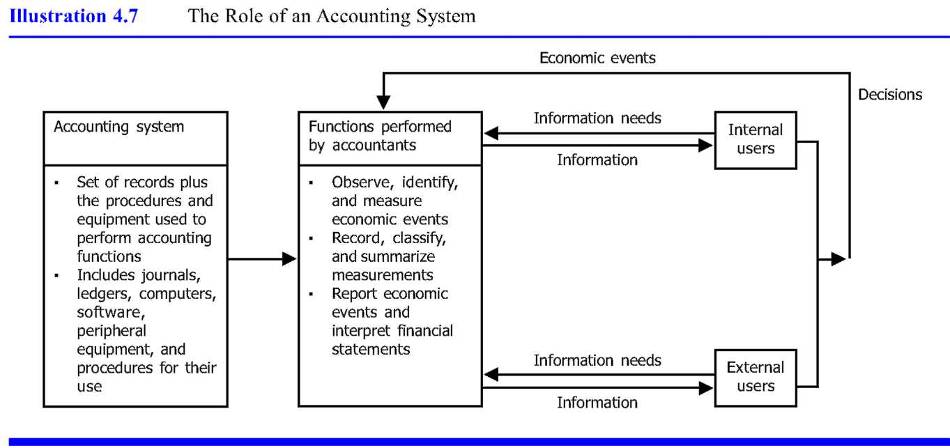

As we show in Exhibit 25, an accounting system is a set of records and the procedures and equipment used to perform the accounting functions. Manual systems consist of journals and ledgers on paper. Computerized accounting systems consist of accounting software, computer files, computers, and related peripheral equipment such as printers.

Regardless of the system, the functions of accountants include: (1) observing, identifying, and measuring economic events; (2) recording, classifying, and summarizing measurements; and (3) reporting economic events and interpreting financial statements. Both internal and external users tell accountants their information needs. The accounting system enables a company's accounting staff to supply relevant accounting information to meet those needs. As internal and external users make decisions that become economic events, the cycle of information, decisions, and economic events begins again.

The primary focus of the first four chapters has been on how you can use an accounting system to prepare financial statements. However, we also discussed how to use that information in making decisions. Later chapters also show how to prepare information and how that information helps users to make informed decisions. We have not eliminated the preparation aspects because we believe that the most informed users are ones who also understand how the information was prepared. These users understand not only the limitations of the information but also its relevance for decision making.

The next section discusses and illustrates the classified balance sheet, which aids in the analysis of the financial position of companies. One example of this analysis is the current ratio and its use in analyzing the short-term debt-paying ability of a company.

An accounting perspective

Uses of technology

Accounting software packages are typically menu driven and organized into modules such as general ledger, accounts payable, accounts receivable, invoicing, inventory, payroll, fixed assets, job cost, and purchase order. For instance, general journal entries are made in the general ledger module, and this module contains all of the company's accounts. The accounts payable module records all transactions involving credit purchases from suppliers and payments made to those suppliers. The accounts receivable module records all sales on credit to various customers and amounts received from customers.