3.4: The need for adjusting entries

- Page ID

- 19992

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

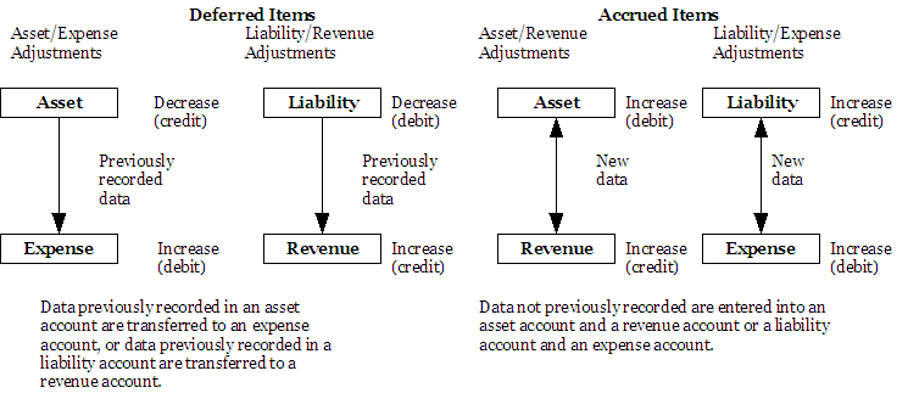

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)The income statement of a business reports all revenues earned and all expenses incurred to generate those revenues during a given period. An income statement that does not report all revenues and expenses is incomplete, inaccurate, and possibly misleading. Similarly, a balance sheet that does not report all of an entity’s assets, liabilities, and stockholders’ equity at a specific time may be misleading. Each adjusting entry has a dual purpose: (1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset or liability. Thus, every adjusting entry affects at least one income statement account and one balance sheet account.

|

January |

30 |

|

February |

9 |

|

March |

16 |

|

April |

8 |

|

May |

18 |

|

June |

49 |

|

July |

8 |

|

August |

14 |

|

September |

42 |

|

October |

17 |

|

November |

13 |

|

Subtotal |

224 |

|

December |

376 |

|

Total Companies |

600 |

|

Source' American Institute of Certified Public Accountants |

Accounting Trends & Techniques (New York' AICPA, 2004) p39 |

Exhibit 15: Summary-fiscal year ending by month

Since those interested in the activities of a business need timely information, companies must prepare financial statements periodically. To prepare such statements, the accountant divides an entity’s life into time periods. These time periods are usually equal in length and are called accounting periods. An accounting period may be one month, one quarter, or one year. An accounting year, or fiscal year, is an accounting period of one year. A fiscal year is any 12 consecutive months. The fiscal year may or may not coincide with the calendar year, which ends on December 31. As we show in Exhibit 15, 63 per cent of the companies surveyed in 2004 had fiscal years that coincide with the calendar year. In 2008, the comparable figure for publicly-traded companies in the US was 65 per cent. Companies in certain industries often have a fiscal year that differs from the calendar year. For instance many retail stores end their fiscal year on January 31 to avoid closing their books during their peak sales period. Other companies select a fiscal year ending at a time when inventories and business activity are lowest.

Periodic reporting and the matching principle necessitate the preparation of adjusting entries. Adjusting entries are journal entries made at the end of an accounting period or at any time financial statements are to be prepared to bring about a proper matchingof revenues and expenses. The matching principle requires that expenses incurred in producing revenues be deducted from the revenues they generated during the accounting period. The matching principle is one of the underlying principles of accounting. This matching of expenses and revenues is necessary for the income statement to present an accurate picture of the profitability of a business. Adjusting entries reflect unrecorded economic activity that has taken place but has not yet been recorded. Why has the company not recorded this activity by the end of the period? One reason is that it is more convenient and economical to wait until the end of the period to record the activity. A second reason is that no source document concerning that activity has yet come to the accountant’s attention.

Adjusting entries bring the amounts in the general ledger accounts to their proper balances before the company prepares its financial statements. That is, adjusting entries convert the amounts that are actually in the general ledger accounts to the amounts that should be in the general ledger accounts for proper financial reporting. To make this conversion, the accountants analyze the accounts to determine which need adjustment. For example, assume a company purchased a three-year insurance policy costing USD 600 at the beginning of the year and debited USD 600 to Prepaid Insurance. At year-end, the company should remove USD 200 of the cost from the asset and record it as an expense. Failure to do so misstates assets and net income on the financial statements.

Companies continuously receive benefits from many assets such as prepaid expenses (e.g. prepaid insurance and prepaid rent). Thus, an entry could be made daily to record the expense incurred. Typically, firms do not make the entry until financial statements are to be prepared. Therefore, if monthly financial statements are prepared, monthly adjusting entries are required. By custom, and in some instances by law, businesses report to their owners at least annually. Accordingly, adjusting entries are required at least once a year. Remember, however, that the entry transferring an amount from an asset account to an expense account should transfer only the asset cost that has expired.

An accounting perspective:

Uses of technology

Eventually, computers will probably enter adjusting entries continuously on a real-time basis so that up-to-date financial statements can be printed at any time without prior notice. Computers will be fed the facts concerning activities that would normally result in adjusting entries and instructed to seek any necessary information from their own databases or those of other computers to continually adjust the accounts.