However, Keynes himself was careful to separate the issue of aggregate demand from the issue of how well individual markets worked. He argued that individual markets for goods and services were appropriate and useful, but that sometimes that level of aggregate demand was just too low. When 10 million people are willing and able to work, but one million of them are unemployed, he argued, individual markets may be doing a perfectly good job of allocating the efforts of the nine million workers—the problem is that insufficient aggregate demand exists to support jobs for all 10 million. Thus, he believed that, while government should ensure that overall level of aggregate demand is sufficient for an economy to reach full employment, this task did not imply that the government should attempt to set prices and wages throughout the economy, nor to take over and manage large corporations or entire industries directly.

The Keynesian approach, with its focus on aggregate demand and sticky prices, has proved useful in understanding how the economy fluctuates in the short run and why recessions and cyclical unemployment occur. Later, will we cover a different viewpoint—the neoclassical perspective—and will consider some of the shortcomings of the Keynesian approach and why it is not especially well-suited for long-run macroeconomic analysis.

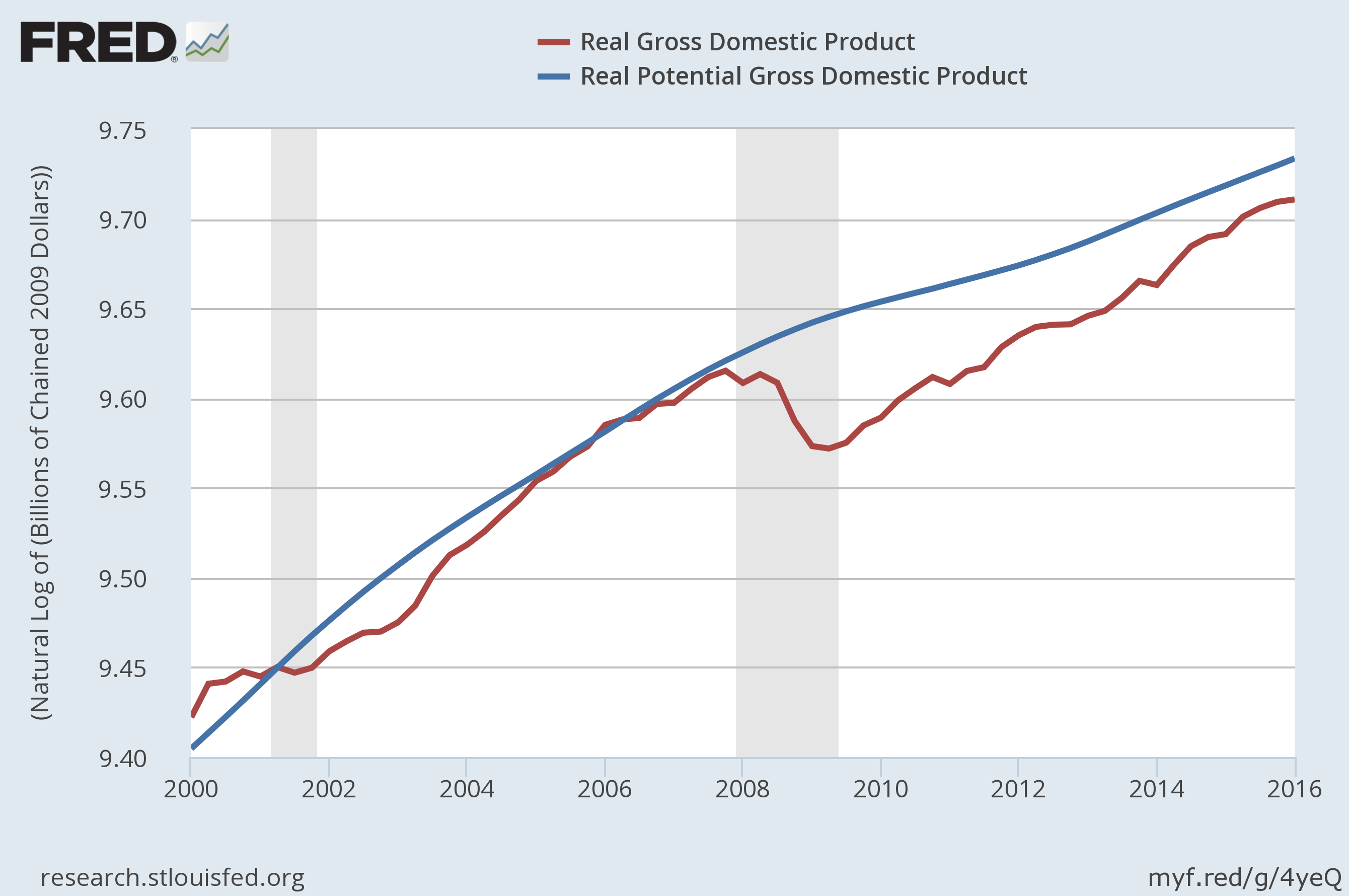

THE GREAT RECESSION

The lessons learned during the Great Depression of the 1930s and the aggregate expenditure model proposed by John Maynard Keynes gave the modern economists and policymakers of today the tools to effectively navigate the treacherous economy in the latter half of the 2000s. In “How the Great Recession Was Brought to an End,” Alan S. Blinder and Mark Zandi wrote that the actions taken by today’s policymakers stand in sharp contrast to those of the early years of the Great Depression. Today’s economists and policymakers were not content to let the markets recover from recession without taking proactive measures to support consumption and investment. The Federal Reserve actively lowered short-term interest rates and developed innovative ways to pump money into the economy so that credit and investment would not dry up. Both Presidents Bush and Obama (along with Congress) implemented a variety of programs ranging from tax rebates to “Cash for Clunkers” to the Troubled Asset Relief Program to stimulate and stabilize household consumption and encourage investment. Although these policies came under harsh criticism from the public and many politicians, they lessened the impact of the economic downturn and may have saved the country from a second Great Depression.