4.6: Choices on Tax Liability of Patronage Refunds

- Page ID

- 4264

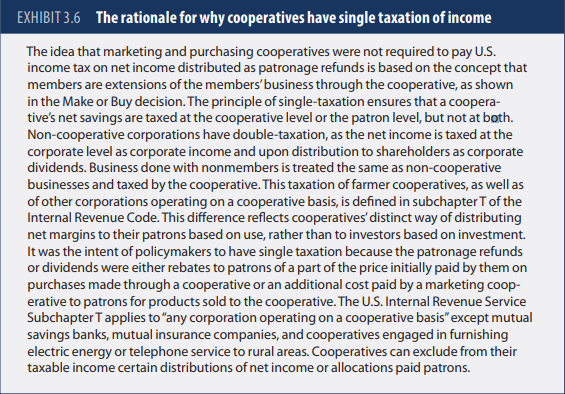

When patronage refunds are properly made in accordance with U.S. Internal Revenue Service tax regulations, they are referred to as qualified and are deductible for corporate income tax purposes. Thus, cooperatives do not pay corporate taxes which are based on income on qualified patronage refunds. As described earlier, a non-cooperative corporation is taxed twice—at both the corporate and individual level—upon distribution of dividends. The majority of boards of directors choose to allocate patronage-sourced income as a qualified distribution.

A board of directors may choose to allocate the patronage-sourced income as nonqualified patronage refunds. This is the reverse of distributing patronage refunds as a qualified distribution in that the cooperative pays the corporate income tax on a nonqualified patronage refund. The member does not pay income tax on this patronage refund until it is received in cash from the cooperative. Single taxation continues to exist with nonqualified refunds.

The patronage-sourced income not paid in cash is called a retained patronage refund, which is the noncash portion of qualified or nonqualified patronage refunds. These patronage refunds are placed on the balance sheet as allocated equity and members are notified in writing of the value

of these patronage refunds allocated but not paid in cash. Remember that the accounting identity states that equity is equivalent to the difference between assets and liabilities. Thus, these retained patronage refunds represent investments in new assets or reinvestment in existing assets to maintain them in good condition to provide the products and services desired by members to satisfy them as customers. Remember also that total equity is the sum of allocated equity and unallocated equity. Historically, boards of directors have chosen to have as much of their equity as possible in allocated equity relative to unallocated equity, although in recent years boards have chosen to increase their unallocated equity.