68: Untitled Page 53

- Page ID

- 10382

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)1. PRINCIPLE OF EQUALITY: TAXATION OF MARRIED AND NON-MARRIED COUPLES

In 1982, Mr. and Mrs. Hegetschweiler filed a complaint to the Swiss Federal Supreme Court, alleging that their canton of residence (Zurich) applied an income tax rate scheme that resulted in a non-justified higher or at least different tax burden for married couples as compared to unmarried taxpayers.

The Federal Supreme Court upheld the complaint, deciding that there had been an infringement of the Constitution.28 According to the court, the principle of equality requires that a married couple must not be taxed at a higher rate than an unmarried couple living in the same circumstances and deriving the same taxable income.

As already mentioned, Swiss income tax law applies family taxation. The joint assessment in connection with the progressive income tax rates may often lead to a so-called “progression effect”, meaning that the spouses pay higher taxes just because of their joint taxation.

As a consequence of the decision in the Hegetschweiler case, all the cantons had to amend their laws. The cantons introduced different measures to ensure equal treatment such as splitting spouses’ income to define the applicable tax rate, making special deductions for dual-income households, having various applicable tax rate schemes etc. Today, unequal treatment of married and unmarried couples is largely abolished on the cantonal and communal level. On the federal level, however, unequal taxation is not fully abolished. In particular, married couples with a high taxable income are still affected by the progression effect.

2. ABILITY-TO-PAY PRINCIPLE: DEGRESSIVE INCOME TAX RATES

In 2007, the Federal Supreme Court had to decide on the constitutionality of degressive income tax rates.29

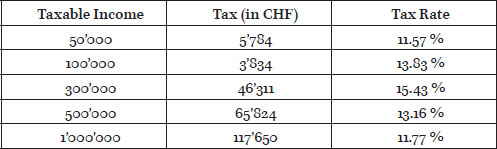

The people of the Canton of Obwalden approved, in a popular vote, a new income tax scale that included degressive tax rates. The tax scale combined progressive tax rates applicable to a taxable income of up to CHF 299’999 with degressive tax rates starting at a taxable income of CHF 300’000. The income tax scale was hence as follows:

Figure 1: Tax Income Scale

A majority of 86 % of the people of the Canton of Obwalden voted in favour of this new income tax scale, most likely being convinced by the government’s argument that low income tax rates for higher taxable income could attract very wealthy new taxpayers to the canton.

However, some taxpayers in the Canton of Obwalden argued before the Federal Supreme Court that such a partially degressive tax scale infringes the ability-to-pay principle as well as the principle of uniformity. The Federal Supreme Court upheld this complaint. They particularly considered that the conversion from a progressive to a degressive tax scale at a taxable income of CHF 300’000 is arbitrary and cannot be reasonably justified. As a consequence, the new law did not enter into force. This judgement clarified that, in Switzerland, income tax rates must be progressive or at least proportional.

3. PRINCIPLE OF GOOD FAITH: SWISS RULING PRACTICE

A Swiss company belonging to a Swiss group set up a permanent establishment in the Cayman Island. The permanent establishment’s purpose was carrying on financing functions for the whole group. In 1999, the cantonal tax administration approved the chosen structure in an advance tax ruling and confirmed that the income allocated to the Cayman permanent establishment will be exempted from Swiss income tax. A few years later, the Federal Tax Administration took the view that the Cayman permanent establishment did not have enough substance and that therefore the income previously attributed to the Cayman permanent establishment will be attributed to the Swiss company. The cantonal tax administration informed the Swiss company about this position in February 2005. The dispute was brought before the Federal Supreme Court.

Advance tax rulings are of high practical importance in Swiss tax practice. Taxpayers have the possibility of asking the competent tax authority to assess the tax implications of a proposed structure or transaction before implementing the structure or carrying on the transaction. Such assessments have a binding nature, based on Article 9 Constitution and the principles of good faith and the prohibition of the abuse of rights.

The Federal Supreme Court confirmed in the mentioned decision the basic requirements for a tax ruling to have binding effect:

-the planned transaction and the accompanying facts must be described in detail and must be correct (including the name of the taxpayer);

-the ruling must be approved by the competent authority;

-the information provided by the tax administration must not be obviously incorrect;

-the taxpayer, based on the information provided in the ruling, has taken steps that cannot be easily undone;

-the law has not changed; and

-the public interest does not require a strict application of the law where this is contrary to the content of the tax ruling.

In the case at hand, the Federal Supreme Court established that the Swiss company’s trust in the tax ruling should be protected for as long as its trust in the tax ruling was not destroyed.30 However, from the moment the Swiss company received the letter from the cantonal authorities informing them of the opinion of the Federal Tax Administration, the Swiss company could no longer rely on the ruling and the protection of his good faith.

4. PRINCIPLE OF NON-DISCRIMINATION: SALARY WITHHOLDING TAX

X, a Swiss national living in France, commuted every day to Geneva for work. According to the double taxation treaty concluded between Switzerland and France, Switzerland was allowed to tax X’s income from employment.

Since X was a Swiss non-resident, his employment income was taxed at source. Under the Swiss source tax system, the source tax that was deducted from X’s salary by his employer did not allow for the deduction of individual expenses, such as commuting costs, contributions to pension funds, and personal tax allowances. Instead, only flat-rate deductions were included in the source tax scale. X complained that such taxation infringes the principle of equality and the Agreement on the Free Movement of Persons concluded between Switzerland and the European Union.31

The Federal Supreme Court upheld X’s complaint. The court referred to the Schumacker doctrine of the European Court of Justice (C-279/93), deciding that the principles developed by the European Court of Justice in that decision are also applicable to the Swiss source tax. In the case at hand, X earned more than 95 % of his taxable income in Switzerland. According to the Schumacker doctrine, Switzerland thus had to take into account his personal situation and was not allowed to tax X less favourably than a Swiss tax resident.

Due to this decision, the law on the source taxation of employment income was amended. The new law does not fundamentally change source taxation as such, but gives taxpayers who are taxed at source the possibility to request, under certain conditions, an ordinary tax assessment. The new law will most likely enter into force on 1 January 2021.

28BGE 110 Ia 7.

29BGE 133 I 206.

30BGE 141 I 161.

31BGE 136 II 241.