9.1: Current versus Long-term Liabilities

- Page ID

- 97798

Use the following as a self-check while working through Chapter 9.

- What is the difference between a current and long-term liability?

- What are some examples of known current liabilities?

- How are known current liabilities different from estimated current liabilities?

- What are some examples of estimated current liabilities?

- How is an estimated current liability different from a contingent liability?

- What are bonds, and what rights are attached to bond certificates?

- What are some characteristics of bonds?

- When a bond is issued at a premium, is the market interest rate higher or lower than the contract interest rate on the bond?

- When a bond is issued at a discount, is the market interest rate higher or lower than the contract interest rate on the bond?

- How are bonds and related premiums or discounts recorded in the accounting records and disclosed on the balance sheet?

- How is a loan payable similar to a bond issue? How is it different?

- How are payments on a loan recorded, and how is a loan payable presented on the balance sheet?

NOTE: The purpose of these questions is to prepare you for the concepts introduced in the chapter. Your goal should be to answer each of these questions as you read through the chapter. If, when you complete the chapter, you are unable to answer one or more the Concept Self-Check questions, go back through the content to find the answer(s). Solutions are not provided to these questions.

9.1 Current versus Long-term Liabilities

LO1 – Identify and explain current versus long-term liabilities.

Current or short-term liabilities are a form of debt that is expected to be paid within the longer of one year of the balance sheet date or one operating cycle. Examples include accounts payable, wages or salaries payable, unearned revenues, short-term notes payable, and the current portion of long-term debt.

Long-term liabilities are forms of debt expected to be paid beyond one year of the balance sheet date or the next operating cycle, whichever is longer. Mortgages, long-term bank loans, and bonds payable are examples of long-term liabilities.

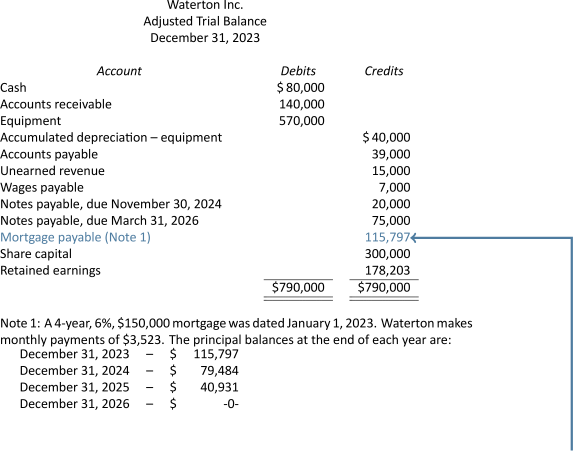

Current and long-term liabilities must be shown separately on the balance sheet. For example, assume the following adjusted trial balance at December 31, 2015 for Waterton Inc.:

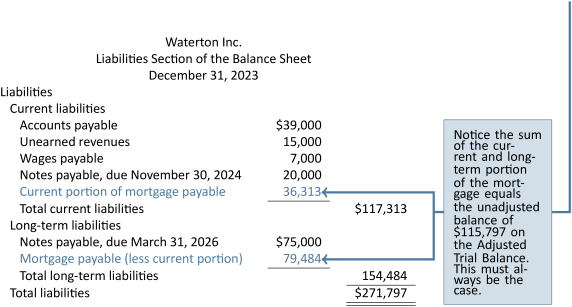

Based on this information, the liabilities section of the December 31, 2023 balance sheet would appear as follows:

The $20,000 notes payable, due November 30, 2024 is a current liability because its maturity date is within one year of the balance sheet date, a characteristic of a current liability. The $75,000 notes payable, due March 31, 2023 is a long-term liability since it is to be repaid beyond one year of the balance sheet date.

It is important to classify liabilities correctly otherwise decision makers may make incorrect conclusions regarding, for example, the organization's liquidity position.

9.2 Known Current Liabilities

LO2 – Record and disclose known current liabilities.

Known current liabilities are those where the payee, amount, and timing of payment are known. Examples include accounts payable, unearned revenues, and payroll liabilities. These are different from estimated current liabilities where the amount is not known and must be estimated. Estimated current liabilities are discussed later in this chapter.

Payroll Liabilities

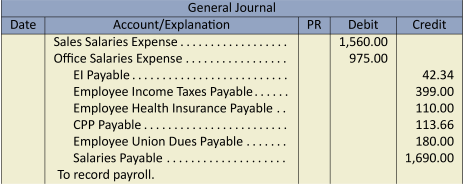

Accounts payable and unearned revenues were introduced and discussed in previous chapters. Payroll liabilities are amounts owing to employees. Employee income taxes, Canada Pension Plan (CPP, or Quebec Pension Plan in Quebec), Employment Insurance (EI), union dues, health insurance, and other amounts are deducted by the employer from an employee's salary or wages. These withheld amounts are remitted by the employer to the appropriate agencies. An employee's gross earnings, less the deductions withheld by the employer, equals the net pay. To demonstrate the journal entries to record a business's payroll liabilities for its two employees, assume the following payroll record:

| Deductions | Payment | Distribution | ||||||

| EI | Income Taxes | Health Ins. | CPP | Union Dues | Total Deductions | Net Pay | Sales Salaries Expense | Office Salaries Expense |

| 25.84 | 285.00 | 55.00 | 62.16 | 105.00 | 533.00 | 1,027.00 | 1,560.00 | |

| 16.50 | 114.00 | 55.00 | 51.50 | 75.00 | 312.00 | 663.00 | 975.00 | |

| 42.34 | 399.00 | 110.00 | 113.66 | 180.00 | 845.00 | 1,690.00 | 1,560.00 | 975.00 |

The employer's journal entries would be:

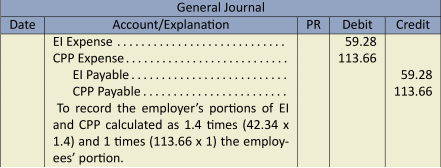

For EI and CPP, both the employee and employer are responsible for making payments to the government. At the time of writing, the employer's portion of EI was calculated as 1.4 times the employee's EI amount. For CPP, the employer is required to pay the same amount as the employee. EI, CPP, and federal/provincial income tax amounts payable are based on rates applied to an employee's gross earnings. The rates are subject to change each tax year. The actual rates for EI, CPP, and federal/provincial income tax can be viewed online at Canada Revenue Agency's website: http://www.cra-arc.gc.ca.

Sales Taxes

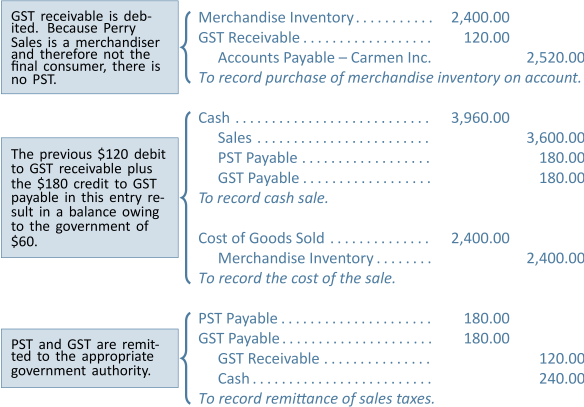

Sales taxes are also classified as known current liabilities. There are two types of sales taxes in Canada: federal Goods and Services Tax (GST) and Provincial Sales Tax (PST). The Goods and Services Tax (GST) is calculated as 5% of the selling price of taxable supplies. For example, if a business is purchasing supplies with a selling price of $1,000, the GST is $50 (calculated as $1,000 x 5%). Taxable supplies are the goods or services on which GST applies. GST is not applied to zero-rated supplies (prescription drugs, groceries, and medical supplies) or exempt supplies (services such as education, health care, and financial). Sellers of taxable supplies are registrants, businesses registered with Canada Revenue Agency that sell taxable supplies and collect GST on behalf of the Receiver General for Canada. The Receiver General for Canada is the federal government body to which all taxes, including federal income tax, are remitted. Registrants also pay GST on the purchase of taxable supplies recording an input tax credit for the GST paid. Total input tax credits, or GST receivable, less GST payable is the amount to be remitted/refunded.

Provincial Sales Tax (PST) is the provincial sales tax paid by the final consumers of products. The PST rate is determined provincially. PST is calculated as a percentage of the selling price. Quebec's equivalent to PST is called the Quebec Sales Tax (QST).

The Harmonized Sales Tax (HST) is a combination of GST and PST that is used in some Canadian jurisdictions. Figure 9.1 summarizes sales taxes across Canada.

| GST | PST | QST | HST | |

| Alberta | 5% | - | - | - |

| British Columbia | 5% | 7% | - | - |

| Manitoba | 5% | 7% | - | - |

| Northwest Territories | 5% | - | - | - |

| Nunavut | 5% | - | - | - |

| Saskatchewan | 5% | 5% | - | - |

| Yukon | 5% | - | - | - |

| Quebec | 5% | - | 9.975% | - |

| Newfoundland and Labrador | - | - | - | 13% |

| New Brunswick | - | - | - | 13% |

| Nova Scotia | - | - | - | 15% |

| Ontario | - | - | - | 13% |

| Prince Edward Island | - | - | - | 14% |

Short-term Notes Payable

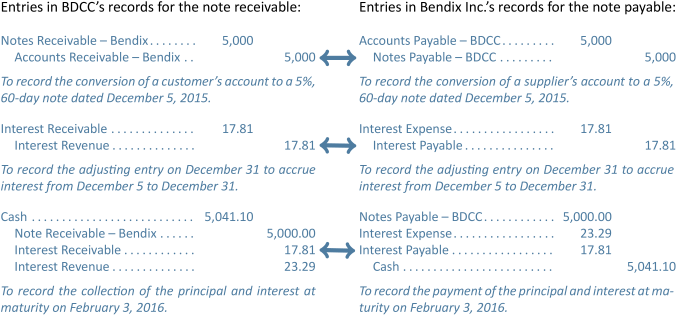

Short-term notes receivable were discussed in Chapter 7. A short-term note payable is identical to a note receivable except that it is a current liability instead of an asset. In Chapter 7, BDCC's customer Bendix Inc. was unable to pay its $5,000 account within the normal 30-day period. The receivable was converted to a 5%, 60-day note receivable dated December 5, 2023. The following example contrasts the entries recorded by BDCC for the note receivable to the entries recorded by Bendix Inc. for its note payable.

Notice that the dollar amounts in the entries for BDCC are identical to those for Bendix. The difference is that BDCC is recognizing a receivable from Bendix while Bendix is recognizing a payable to BDCC.

9.3 Estimated Current Liabilities

LO3 – Record and disclose estimated current liabilities.

An estimated liability is known to exist where the amount, although uncertain, can be estimated. Two common examples of estimated liabilities are warranties and income taxes.

Warranty Liabilities

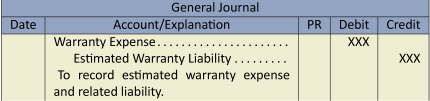

A warranty is an obligation incurred by the seller of a product or service to replace or repair defects. Warranties typically apply for a limited period of time. For example, appliances are often sold with a warranty for a specific time period. The seller does not know which product/service will require warranty work, when it might occur, or the amount. To match the warranty expense to the period in which the revenue was realized, the following entry that estimates the amount of warranty expense and related liability must be recorded:

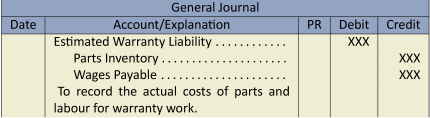

When the warranty work is actually performed, assuming both parts and labour, the following is recorded:

Income Tax Liabilities

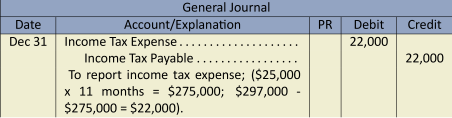

A corporation is taxed on the taxable income it earns. As for any entity, corporations must file a tax return annually. However, the government typically requires the corporation to make advance monthly payments based on an estimated amount. When the total actual amount of income tax is known at the end of the accounting period, the corporation will record an adjustment to reconcile any difference between the total actual tax and the total monthly tax accrued in the accounting records. For example, assume it is estimated that the total income tax for the year ended December 31, 2023 will be $300,000. This translates into $25,000 of income tax to be accrued at the end of each month ($300,000 ![]() 12 months = $25,000/month). Assume further that the government requires payments to be made by the 15th of the following month. The entries at the end of each month from January through to November would be:

12 months = $25,000/month). Assume further that the government requires payments to be made by the 15th of the following month. The entries at the end of each month from January through to November would be:

On the 15th of each month beginning February 15th to December 15th, the following entry would be recorded:

Assume that at the end of December, the corporation's actual income tax was determined to be $297,000 instead of the originally estimated $300,000. The entry at December 31 would be:

Contingent Liabilities

Recall that an estimated liability is recorded when the liability is probable and the amount can be reliably estimated. A contingent liability exists when one of the following two criteria are satisfied:

- it is not probable or

- it cannot be reliably estimated.

A liability that is determined to be contingent is not recorded, rather it is disclosed in the notes to the financial statements except when there is a remote likelihood of its existence. An example of a contingent liability is a lawsuit where it is probable there will be a loss but the amount cannot be reliably determined. A brief description of the lawsuit must be disclosed in the notes to the financial statements; it would not be recorded until the amount of the loss could be reliably estimated. Great care must be taken with contingencies — if an organization intentionally withholds information, it could cause decision makers, such as investors, to make decisions they would not otherwise have made.

Contingent assets, on the other hand, are not recorded until actually realized. If a contingent asset is probable, it is disclosed in the notes to the financial statements.

9.4 Long-Term Liabilities—Bonds Payable

LO4 – Identify, describe, and record bonds.

Corporations generally acquire long-lived assets like property, plant, and equipment through the issue of shares or long-term debt that is repayable over many years. Chapter 10 addresses the ways in which a corporation can raise funds by issuing shares, known as equity financing. This chapter discusses corporate financing by means of issuing long-term debt, known as debt financing. Types of long-term debt are typically classified according to their means of repayment.

- Bonds pay only interest at regular intervals to investors. The original investment is repaid to bondholders when the bond matures (or comes due), usually after a number of years. Bonds are generally issued to many individual investors.

- Loans are repaid in equal payments on a regular basis. The payments represent both interest and principal paid to creditors. Such payments are said to be blended. That is, each payment contains repayment of a certain amount of the original amount of the loan (the principal), as well as interest on the remaining principal balance.

Bonds are discussed in this section. Loans are expanded upon in the next section. Other types of debt, such as leases, are left for study in a more advanced accounting textbook.

Rights of Bondholders

As noted above, a bond is a debt instrument, generally issued to many investors, that requires future repayment of the original amount at a fixed date, as well as periodic interest payments during the intervening period. A contract called a bond indenture is prepared between the corporation and the future bondholders. It specifies the terms with which the corporation will comply, such as how much interest will be paid and when. Another of these terms may be a restriction on further borrowing by the corporation in the future. A trustee is appointed to be an intermediary between the corporation and the bondholder. The trustee administers the terms of the indenture.

Ownership of a bond certificate carries with it certain rights. These rights are printed on the actual certificate and vary among bond issues. The various characteristics applicable to bond issues are the subject of more advanced courses in finance and are not covered here. However, individual bondholders always acquire two rights.

- The right to receive the face value of the bond at a specified date in the future, called the maturity date.

- The right to receive periodic interest payments at a specified percent of the bond's face value.

Bond Authorization

Every corporation is legally required to follow a well-defined sequence in authorizing a bond issue. The bond issue is presented to the board of directors by management and must be approved by shareholders. Legal requirements must be followed and disclosure in the financial statements of the corporation is required.

Shareholder approval is an important step because bondholders are creditors with a prior claim on the corporation's assets if liquidation occurs. Further, dividend distributions may be restricted during the life of the bonds, and those shareholders affected usually need to approve this. These restrictions are typically reported to the reader of financial statements through note disclosure.

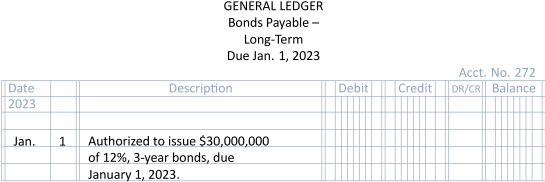

Assume that Big Dog Carworks Corp. decides to issue $30 million of 12% bonds to finance its expansion. The bonds are repayable three years from the date of issue, January 1, 2023. The amount of authorized bonds, their interest rate, and their maturity date can be shown in the accounts as follows:

Bonds in the Financial Statement

Each bond issue is disclosed separately in the notes to the financial statements because each issue may have different characteristics. The descriptive information disclosed to readers of financial statements includes the interest rate and maturity date of the bond issue. Also disclosed in a note are any restrictions imposed on the corporation's activities by the terms of the bond indenture and the assets pledged, if any.

Other Issues Related to Bond Financing

There are several additional considerations related to the issue of bonds.

- Cash Required in the Immediate and the Foreseeable Future

Most bond issues are sold in their entirety when market conditions are favourable. However, more bonds can be authorized in a particular bond issue than will be immediately sold. Authorized bonds can be issued whenever cash is required.

- Time Periods Associated with Bonds

The interest rate of bonds is associated with time, their maturity date is based on time, and other provisions — such as convertibility into share capital and restrictions on future dividend distributions of the corporation — are typically activated at a given point in time. These must also be considered, as the success of a bond issue often depends on the proper combination of these and other similar features.

- Assets of the Corporation to Be Pledged

Whether or not long-lived assets like property, plant, and equipment are pledged as security is an important consideration for bondholders because doing so helps to safeguard their investments. This decision is also important to the corporation because pledging all these assets may restrict future borrowings. The total amount of authorized bonds is usually a fraction of the pledged assets, such as 50%. The difference represents a margin of safety to bondholders. The value of these assets can shrink substantially but still permit reimbursement of bondholders should the company be unable to pay the bond interest or principal, and need to sell the pledged assets.

Bond Characteristics

Each corporation issuing bonds has unique financing needs and attempts to satisfy various borrowing situations and investor preferences. Many types of bonds have been created to meet these varying needs.

Secured bonds are backed by physical assets of the corporation. These are usually long-lived assets. When real property is legally pledged as security for the bonds, they are called mortgage bonds.

Unsecured bonds are commonly referred to as debentures. A debenture is a formal document stating that a company is liable to pay a specified amount with interest. The debt is not backed by any collateral. As such, debentures are usually only issued by large, well-established companies. Debenture holders are ordinary creditors of the corporation. These bonds usually command a higher interest rate because of the added risk for investors.

Registered bonds require the name and address of the owner to be recorded by the corporation or its trustee. The title to bearer bonds passes on delivery of the bonds to new owners and is not tracked. Payment of interest is made when the bearer clips coupons attached to the bond and presents these for payment. Bearer bonds are becoming increasingly rare.

When serial bonds are issued, the bonds have differing maturity dates, as indicated on the bond contract. Investors are able to choose bonds with a term that agrees with their investment plans. For example, in a $30 million serial bond issue, $10 million worth of the bonds may mature each year for three years.

The issue of bonds with a call provision permits the issuing corporation to redeem, or call, the bonds before their maturity date. The bond indenture usually indicates the price at which bonds are callable. Corporate bond issuers are thereby protected in the event that market interest rates decline below the bond contract interest rate. The higher interest rate bonds can be called to be replaced by bonds bearing a lower interest rate.

Some bonds allow the bondholder to exchange bonds for a specified type and amount of the corporation's share capital. Bonds with this feature are called convertible bonds. This feature permits bondholders to enjoy the security of being creditors while having the option to become shareholders if the corporation is successful.

When sinking fund bonds are issued, the corporation is required to deposit funds at regular intervals with a trustee. This feature ensures the availability of adequate cash for the redemption of the bonds at maturity. The fund is called "sinking" because the transferred assets are tied up or "sunk," and cannot be used for any purpose other than the redemption of the bonds.

The corporation issuing bonds may be required to restrict its retained earnings. The restriction of dividends means that dividends declared cannot exceed a specified balance in retained earnings. This protects bondholders by limiting the amount of dividends that can be paid.

Investors consider the interest rates of bonds as well as the quality of the assets, if any, that are pledged as security. The other provisions in a bond contract are of limited or no value if the issuing corporation is in financial difficulties. A corporation in such difficulties may not be able to sell its bonds, regardless of the attractive provisions attached to them.

Recording the Issuance of Bonds at Face Value (at Par)

Each bond has an amount printed on the face of the bond certificate. This is called the face value of the bond; it is also referred to as the par-value of the bond. When the cash received is the same as a bond's face value, the bond is said to be issued at par. A common face value of bonds is $1,000, although bonds of other denominations exist. A $30 million bond issue can be divided into 30,000 bonds, for example. This permits a large number of individuals and institutions to participate in corporate financing.

If a bond is sold at face value, the journal entry is:

Recording the Issuance of Bonds at a Premium

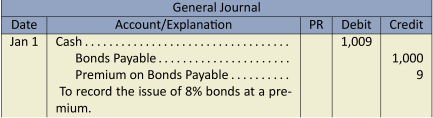

A $1,000 bond is sold at a premium when it is sold for more than its face value. This results when the bond interest rate is higher than the market interest rate. For instance, assume Big Dog Carworks Corp. issues a bond on January 1, 2023 with a face value of $1,000, a maturity date of one year, and a stated or contract interest rate of 8% per year, at a time when the market interest rate is 7%. Potential investors will bid up the bond price to $1,009.34 based on present value calculations where FV = $1,000; PMT = $80; i = 7 (the market rate); and n = 1.2 We will round the $1,009.34 to $1,009 to simplify the demonstration.

The premium is the $9 difference between the $1,009 selling price of the bond and the $1,000 face value. The journal entry to record the sale of the bond on January 1, 2023 is:

The Premium on Bonds Payable account is a contra liability account that is added to the value of the bonds on the balance sheet. Because the bonds mature in one year, the bond appears in the current liabilities section of the balance sheet as follows:

| Liabilities | ||

| Current | ||

|

Bonds payable |

$1,000 | |

|

Add: Premium on bonds payable |

9 | $1,009 |

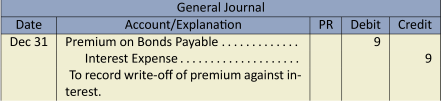

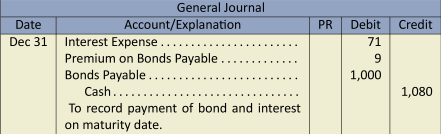

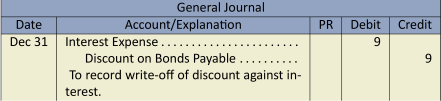

On the maturity date of December 31, 2023, the interest expense of $80 is paid, bondholders are repaid, and the premium is written off as a reduction of interest expense.

These three journal entries would be made:

Alternatively, a single entry would be preferable as follows:

Note that the interest expense recorded on the income statement would be $71 ($80 – 9). This is equal to the market rate of interest at the time of bond issue.

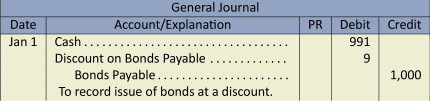

Recording the Issuance of Bonds at a Discount

If the bond is sold for less than $1,000, then the bond has been sold at a discount. This results when the bond interest rate is lower than the market interest rate. To demonstrate the journal entries, assume a $1,000, one-year, 8% bond is issued by BDCC when the market interest rate is 9%. The selling amount will be $990.83 using PV calculations where FV = $1,000; PMT = $80; i = 9 (the market rate); and n = 1. We will round the $990.83 to $991 to simplify the demonstration.

The difference between the face value of the bond ($1,000) and the selling price of the bond ($991) is $9. This is the discount.

The journal entry to record the transaction on January 1, 2023 is:

The $9 amount is a contra liability account and is deducted from the face value of the bonds on the balance sheet as follows:

| Liabilities | ||

| Current | ||

|

Bonds payable |

$1,000 | |

|

Less: Discount on bonds payable |

(9) | $991 |

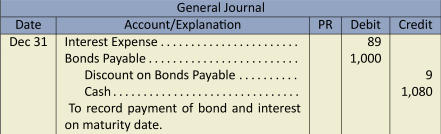

On December 31, 2023, when the bonds mature, the following entries would be recorded:

Alternatively, a single entry would be preferable as follows:

The interest expense recorded on the income statement would be $89 ($80 + 9). This is equal to the market rate of interest at the time of bond issue.

These are simplified examples, and the amounts of bond premiums and discounts in these examples are insignificant. In reality, bonds may be outstanding for a number of years, and related premiums and discounts can be substantial when millions of dollars of bonds are issued. These premiums and discounts are amortized using the effective interest method over the same number of periods as the related bonds are outstanding. The amortization of premiums and discounts is an intermediate financial accounting topic and is not covered here.

Refer to the Appendix Section 9.8 at the end of this chapter for discussions and illustrations regarding the use of the effective interest method for bonds issued at a premium or discount.

Bonds Issued in Between Interest Payments

If investors purchase bonds on dates falling in between the interest payment dates, then the investor pays an additional interest amount. This is because the bond issuer always pays the full six months interest to the bondholder on the interest payment date because it is the easiest way to administer multiple interest payments to potentially thousands of investors. For example, if an investor purchases a bond four months after the last interest payment, then the issuer will add these additional four months of interest to the purchase price. When the next interest payment date occurs, the issuer pays the full six months interest to the purchaser. The interest amount paid and received by the bond-holder will net to two months. This makes intuitive sense given that the bonds have only been held for two months making interest for two months the correct amount.

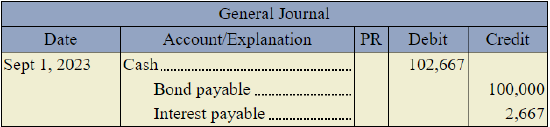

For example, on September 1, 2023, an investor purchases at face value, $100,000, 10-year, 8% bonds with interest payable each May 1 and November 1.

| Bond payable | $100,000 |

| Accrued interest ( |

2,667 |

| Total cash paid | $102,667 |

To record the bond issuance on September 1, with four months' accrued interest:

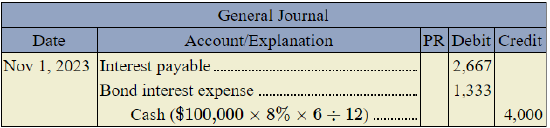

To record the first semi-annual interest payment on November 1 and zero out the interest payable:

Note that the bond interest on November 1 is for the amount the bondholder is entitled to, which is two months' of interest.

The December 31 year-end accrued interest entry:

At maturity, the May 1, 2026, entry would be:

Repayment Before Maturity Date

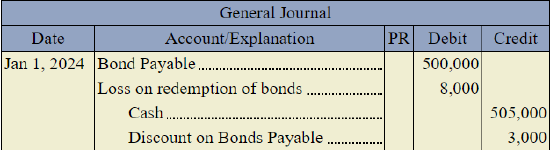

In some cases, a company may want to repay a bond issue before its maturity. Examples of such bonds are callable bonds, which give the issuer the right to call and retire the bonds before maturity. For example, if market interest rates drop, the issuer will want to take advantage of the lower interest rate. In this case, the reacquisition price paid to extinguish and derecognize the bond issuance will likely be slightly higher than the bond carrying value on that date, and the difference will be recorded by the issuing corporation as a loss on redemption. The company can, then, sell a new bond issuance at the new, lower interest rate.

For example, on January 1, 2020, Angen Ltd. issued bonds with a par value of $500,000 at 99, due in 2026. On January 1, 2024, the entire issue was called at 101 and cancelled. The bond payable carrying value on the call date was $497,000. Interest is paid annually and the discount amortized using the straight-line method. The carrying value of the bond on January 1, 2024, would be calculated as follows:

| Carrying value on call date | $497,000 |

| Re-acquisition price ( |

505,000 |

| Loss on redemption | $8,000 |

Angen Ltd. would make the following entry:

9.5 Long-term Liabilities—Loans Payable

LO5 – Explain, calculate, and record long-term loans.

A loan is another form of long-term debt that a corporation can use to finance its operations. Like bonds, loans can be secured, giving the lender the right to specified assets of the corporation if the debt cannot be repaid. For instance a mortgage is a loan secured by specified real estate of the company, usually land with buildings on it.

Unlike a bond, a loan is typically obtained from one lender such as a bank. Also, a loan is repaid in equal blended payments over a period time. These payments contain both interest payments and some repayment of principal. As well, a loan does not give rise to a premium or discount because it is obtained at the market rate of interest in effect at the time.

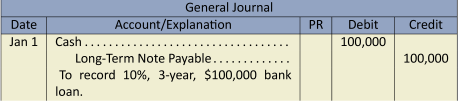

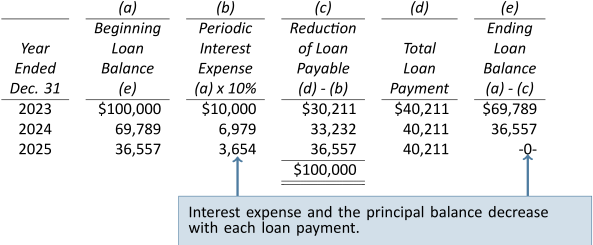

To demonstrate the journal entries related to long-term loans, assume BDCC obtained a three-year, $100,000, 10% loan on January 1, 2023 from First Bank to acquire a piece of equipment. When the loan proceeds are deposited into BDCC's bank account, the following entry is recorded:

The loan is repayable in three annual blended payments. To calculate the payments, PV analysis is used whereby the following keystrokes are entered into a business calculator:

| PV = 100000 (the cash received from the bank), |

| i = 10 (the interest rate), |

| n = 3 (the term of the loan is three years), and Compute PMT. |

The PMT (or payment) is -40211.48. The result is negative because payments are cash outflows. While the payments remain the same each year, the amount of interest paid decreases and the amount of principal increases. Figure 9.2 illustrates this effect.

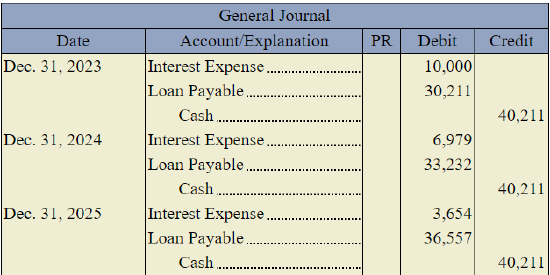

Figure 9.2 can be used to construct the journal entries to record the loan payments at the end of each year:

The amounts in Figure 9.2 can also be used to present the related information on the financial statements of BDCC at each year end. Recall that assets and liabilities need to be classified as current and non-current portions on the balance sheet. Current liabilities are amounts paid within one year of the balance sheet date. That part of the loan payable to First Bank to be paid in the upcoming year needs to be classified as a current liability on the balance sheet. The amount of the total loan outstanding at December 31, 2015, 2016, and 2017 and the current and non-current portions are shown in Figure 9.3:

| A | B | C | D |

| Year ended Dec. 31 | Ending loan balance per general ledger (Fig 9.2, Col. E) | Current portion (Fig. 9.2, Col. C) | (B – C) Long-term portion |

| 2023 | $69,788 | $33,232 | $36,557 |

| 2024 | 36,557 | 36,557 | -0- |

| 2025 | -0- | -0- | -0- |

| 2023 | 2024 | 2025 | |

| Current liabilities | |||

|

Current portion of bank loan |

$33,232 | $36,557 | $-0- |

| Long-term liabilities | |||

|

Bank loan (Note X) |

36,557 | -0- | -0- |

Details of the loan would be disclosed in a note to the financial statements. Only the principal amount of the loan is reported on the balance sheet. The interest expense portion is reported on the income statement as an expense. Because these loan payments are made at BDCC's year end, no interest payable is accrued or reported on the balance sheet.

9.6 Appendix A: Present Value Calculations

Interest is the time value of money. If you borrow $1 today for one year at 10% interest, its future value in one year is $1.10 ($1 ![]() 110% = $1.10). The increase of 10 cents results from the interest on $1 for the year. Conversely, if you are to pay $1.10 one year from today, the present value is $1 — the amount you would need to invest today at 10% to receive $1.10 in one year's time ($1.10/110% = $1). The exclusion of applicable interest in calculating present value is referred to as discounting.

110% = $1.10). The increase of 10 cents results from the interest on $1 for the year. Conversely, if you are to pay $1.10 one year from today, the present value is $1 — the amount you would need to invest today at 10% to receive $1.10 in one year's time ($1.10/110% = $1). The exclusion of applicable interest in calculating present value is referred to as discounting.

If the above $1.10 amount at the end of the first year is invested for an additional year at 10% interest, its future value would be $1.21 ($1.10 x 110%). This consists of the original $1 investment, $.10 interest earned in the first year, and $.11 interest earned during the second year. Note that the second year's interest is earned on both the original $1 and on the 10 cents interest earned during the first year. This increase provides an example of compound interest — interest earned on interest.

The following formula can be used to calculate this:

![]()

where FV = future value, PV = present value, i = the interest rate, and n = number of periods.

Substituting the values of our example, the calculation would be ![]() , or $1.21.

, or $1.21.

If the future value of today's $1 at 10% interest compounded annually amounts to $1.21 at the end of two years, the present value of $1.21 to be paid in two years, discounted at 10%, is $1. The formula to calculate this is just the inverse of the formula shown above, or

![]()

Substituting the values of our example,

![]()

That is, the present value of $1.21 received two years in the future is $1. The present value is always less than the future value, since an amount received today can be invested to earn a return (interest) in the intervening period. Calculating the present value of amounts payable or receivable over several time periods is explained more thoroughly below.

Instead of using formulas to calculate future and present values, a business calculator can be used where:

PV = present value

FV = future value

i = interest rate per period (for a semi-annual period where the annual interest rate is 8%, for example, i = 4% and would be entered into the calculator as '4' – not .04)

PMT = dollar amount of interest per period

n = number of periods.

The following three scenarios demonstrate how PV analysis is used to determine the issue price of a $100,000 bond.

- Big Dog Carworks Corp. issues $100,000 of 3-year, 12% bonds on January 1, 2023 when the market rate of interest is 12%. Interest is paid semi-annually.

- BDCC's bonds are issued at a premium because the market rate of interest is 8% at the date of issue.

- BDCC's bonds are issued at a discount because the market rate of interest is 16% at the date of issue.

In each scenario, the bond principal of $100,000 will be repaid at the end of three years, and interest payments of $6,000 (calculated as $100,000 x 12% x 6/12) will be received every six months for three years.

Scenario 1: The Bond Contract Interest Rate is 12% and the Market Interest Rate Is 12%

The market interest rate is the same as the bond interest rate, therefore the bond is selling at par. The present value will be $100,000, the face value of the bond, which can be confirmed by entering the following into a business calculator:

FV = -100000 (we enter this as a negative because it is a cash outflow — it is being paid and not received when the bond matures)

i = 6 (calculated as 12%/year ![]() 2 periods per year)

2 periods per year)

PMT = -6000 (we enter this as a negative because it is a cash outflow — it is being paid and not received each semi-annual interest period)

n = 6 (3-year bond ![]() 2 periods per year)

2 periods per year)

Compute PV

The PV = 100000. This result confirms that the bond is being issued at par or face value.

Scenario 2: The Bond Contract Interest Rate is 12% and the Market Interest Rate Is 8%

The market interest rate is less than the bond interest rate, therefore the bond is selling at a premium. The present value can be determined by entering the following into a business calculator:

FV = -100000 (we enter this as a negative because it is a cash outflow — it is being paid and not received when the bond matures)

i = 4 (calculated as 8%/year ![]() 2 periods per year)

2 periods per year)

PMT = -6000 (we enter this as a negative because it is a cash outflow — it is being paid and not received each semi-annual interest period)

n = 6 (3-year bond ![]() 2 periods per year)

2 periods per year)

Compute PV

The PV = 110484.27. This confirms that the bond is being issued at a premium. The premium is $10,484.27 calculated as the difference between the present value of $110,484.27 and the face value of $100,000.

Scenario 3: The Bond Contract Interest Rate is 12% and the Market Interest Rate Is 16%

The market interest rate is more than the bond interest rate, therefore the bond is selling at a discount. The present value can be determined by entering the following into a business calculator:

FV = -100000 (we enter this as a negative because it is a cash outflow — it is being paid and not received when the bond matures)

i = 8 (calculated as 16%/year ![]() 2 periods per year)

2 periods per year)

PMT = -6000 (we enter this as a negative because it is a cash outflow — it is being paid and not received each semi-annual interest period)

n = 6 (3-year bond ![]() 2 periods per year)

2 periods per year)

Compute PV

The PV = 90754.24. This confirms that the bond is being issued at a discount. The discount is $9,245.76 calculated as the difference between the present value of $90,754.24 and the face value of $100,000.

9.7 Appendix B: Additional Payroll Transactions

Net pay calculations

A business maintains a Payroll Register that summarizes the hours worked for each employee per pay period. The payroll register details an employee's regular pay plus any overtime pay before deductions, known as gross pay. An employee is paid their net pay (gross pay less total deductions). Payroll deductions are amounts subtracted by the employer from an employee's gross pay. Deductions are also known as withholdings or withheld amounts. Deductions can vary depending on the employer. Some deductions are optional and deducted by the employer based on directions made by the employee. Examples of optional deductions include an employee's charitable donations or Canada Savings Bonds contributions.

Certain payroll deductions are required by law. Deductions legally required to be deducted by the employer from an employee's gross pay are income tax, Employment Insurance (EI), and Canada Pension Plan (CPP or QPP in Quebec). The amount of legally required deductions is prescribed and based on an employee's income. For more detailed information regarding the calculation of these deductions, go to: http://www.cra-arc.gc.ca/tx/bsnss/tpcs/pyrll/clcltng/menu-eng.html

Other deductions that are often withheld by employers include union dues and health care premiums.

All deductions withheld by employers must be paid to the appropriate authority. For example, income tax, EI, and CPP must be paid to the Receiver General for Canada. Charitable donations withheld by an employer would be paid to the charity as directed by the employee.

Recording Payroll

The entry made by the employer to record payroll would debit the appropriate salary or wage expense category and credit:

- Salaries Payable or Wages Payable for the net pay and

- Each deduction such as EI Payable, CPP Payable, etc.

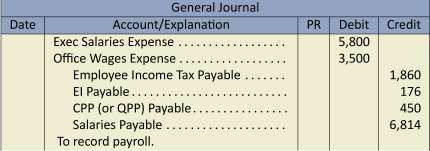

To demonstrate, assume the following payroll information for Wil Stavely and Courtney Dell:

| Deductions | Distribution | ||||||

| Gross Pay | Income Tax | EI | CPP | Net Pay | Exec Salaries | Office Wages | |

| Dell, Courtney | 5,800 | 1,160 | 106 | 280 | 4,254 | 5,800 | |

| Stavely, Will | 3,500 | 700 | 70 | 170 | 2,560 | 3,500 | |

The payroll journal entry would be:

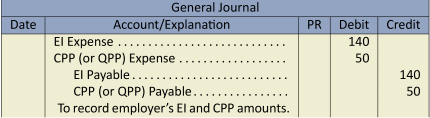

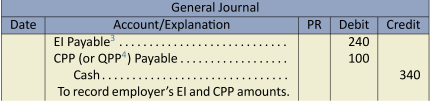

Recording Employer's CPP and EI Amounts

As already indicated, employers are legally required to deduct/withhold an employee's amount for each of the following from an employee's gross pay:

- the employee's amount for Canada Pension Plan (CPP or QPP in Quebec) and

- the employee's amount for Employment Insurance (EI).

The employer is required by law to pay Employment Insurance (EI) at the rate of 1.4 times the EI withheld from each employee. For example, if the employer withheld $100 of EI from Employee A's gross pay, the employer would have to pay EI of $140 (calculated as $100 x 1.4). Therefore, the total amount of EI being paid to the government regarding Employee A is $240 (calculated as the employee's portion of $100 plus the employer's portion of $140).

The employer is also required by law to pay CPP (or QPP in Quebec) of an amount that equals the employee amount. For example, if the employer withheld $50 of CPP from Employee A's gross pay, the employer would have to pay CPP of $50. Therefore, the total amount of CPP being paid to the government regarding Employee A is $100 (calculated as the employee's portion of $50 plus the employer's portion of $50).

The journal entry to record the employer's amounts above for EI and CPP would be:

Employer's Entries to Pay the Payroll Deductions

Employers are required by law to pay/remit to the Receiver General for Canada all income tax, EI, and CPP amounts deducted/withheld from employees along with the employer's portion of EI and CPP. Any other amounts deducted/withheld from employees such as union dues, health care premiums, or charitable donations must also be paid/remitted to the appropriate organizations. The journal entry to record these payments/remittances by the employer would debit the respective liability account and credit cash. For example, using the information from our previous example, we know that the employer withheld from the employee's gross pay $100 of EI and $50 of CPP. Additionally, the employer recorded its share of the EI ($140) and CPP ($50) amounts. The total EI to be paid is therefore $240 and the total CPP $100. The payment by the employer would be:

Fringe Benefits and Vacation Benefits

Some employers pay for an employee's benefits such as health insurance. The journal entry to record benefits would be:

Employers are also required to pay for vacation time equal to 4% of gross income. The entry to accrue vacation benefits would be:

When vacation benefits are realized by the employee, the Estimated Vacation Liability account is debited and the appropriate liability accounts to record deductions/withholdings and net pay are credited.

9.8 Appendix C: The Effective Interest Rate Method

Another way to calculate the interest expense when a bond is issued at a premium or discount is the effective interest rate method.

Below are two examples where a bond is issued at a premium or discount. The interest expense and the amortization of the premium or discount is computed using the effective interest rate method.

Note that the bond's fair value can be determined by either using the market spot rate or by performing a present value calculation. Use of the market spot rate is shown in the bond premium example, while the present value calculation is shown in the bond discount example. These are discussed next.

Bonds Issued at a Premium

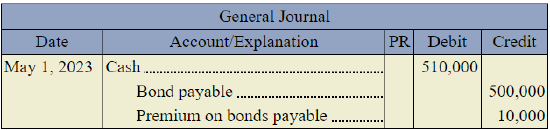

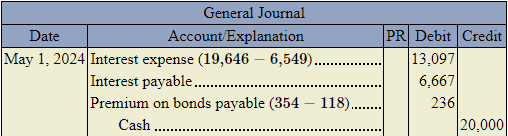

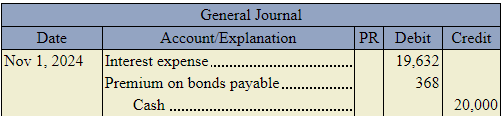

On May 1, 2023, Impala Ltd. issued a 10-year, 8%, $500,000 face value bond at a spot rate of 102 (2% above par). Interest is payable each year on May 1 and November 1. The company uses the effective interest rate method to calculate interest expense and amortize the bond premium.

The spot rate is 102, so the amount to be paid is $510,000 (![]() ) and, therefore, represents the fair value or present value of the bond issuance on the purchase date.

) and, therefore, represents the fair value or present value of the bond issuance on the purchase date.

The entry for the bond issuance is:

Below is a portion of the effective interest rate method table:

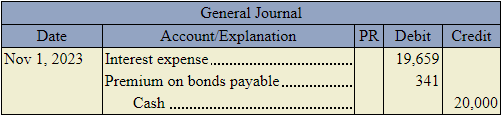

| Payment | Interest 3.8547% | Amortization of Premium | Balance | |

| May 1, 2023 | 510,000 | |||

| Nov 1, 2023 | 20,000 | 19,659 | 341 | 509,659 |

| May 1, 2024 | 20,000 | 19,646 | 354 | 509,305 |

| Nov 1, 2024 | 20,000 | 19,632 | 368 | 508,937 |

Using the information from the schedule, the entries are completed below.

To record the interest payment and amortization of premium on November 1:

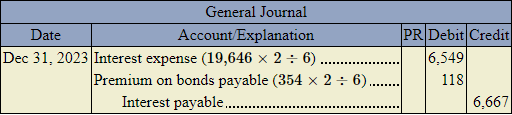

Recording the accrued interest at the December 31 year-end uses the relevant portion of the effective interest schedule. For example, at December 31, 2023, the table shows interest of $19,646 and bond amortization of $354 at May, 2017. Prorating these amounts for November and December, or two months, results in the following entry:

To record the interest payment on May 1, 2024, interest expense and amortization will be for the remainder of the table amounts of $19,646 and $354 respectively:

To record the interest payment on November 1, 2024:

At maturity, the May 1, 2033, entry would be:

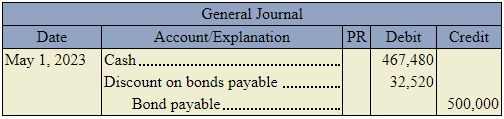

Bonds Issued at a Discount

On May 1, 2016, Engels Ltd. issued a 10-year, 8%, $500,000 face value bond with interest payable each year on May 1 and November 1. The market rate at the time of issuance is 9% and the company year-end is December 31. In this case the stated rate of 8% is less than the market rate of 9%. This means that the bond issuance is trading at a discount and the fair value, or its present value of the future cash flows, will be less than the face value upon issuance. The present value is calculated as:

| 20,000 | PMT | (where semi-annual interest using the stated or face rate is |

| 4.5 | I/Y | (where 9% market or effective interest is paid twice per year) |

| 20 | N | (where interest is paid twice per year for 10 years) |

| 500,000 | FV | (where a single payment of the face value is due in a future year 2026); |

Expressed in the following variables string, and using a financial calculator, the present value is calculated:

| Present value (PV) = (20,000 PMT, 4.5 I/Y, 20 N, 500,000 FV) = | $467,480 |

Had the market spot rate been used, this bond would be trading at a spot rate of 93.496 (or 93.496% of the bond's face value, which is below par). The fair value would also be $467,480 (![]() ).

).

The stated rate of 8% is less than the market rate of 9%, resulting in a present value less than the face amount of $500,000. This bond issuance is trading at a discount. Since the market rate is greater, the investor would not be willing to purchase bonds paying less interest at the face value. The bond issuer must, therefore, sell these at a discount in order to entice investors to purchase them. The investor pays the reduced price of $467,480. For the seller, the discount amount of $32,520 (![]() ) is then amortized over the life of the bond issuance using the effective interest rate method. The total interest expense for either method will be the same.

) is then amortized over the life of the bond issuance using the effective interest rate method. The total interest expense for either method will be the same.

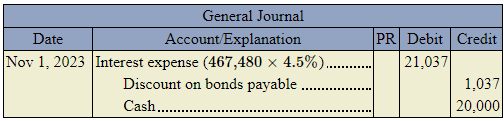

The interest schedule for the bond issuance is shown below:

| Payment | Interest 4.5% | Amortization of Discount | Balance | |

| May 1, 2023 | 467,480 | |||

| Nov 1, 2023 | 20,000 | 21,037 | 1,037 | 468,517 |

| May 1, 2024 | 20,000 | 21,083 | 1,083 | 469,600 |

| Nov 1, 2024 | 20,000 | 21,132 | 1,132 | 470,732 |

| May 1, 2025 | 20,000 | 21,183 | 1,183 | 471,915 |

| Nov 1, 2025 | 20,000 | 21,236 | 1,236 | 473,151 |

| May 1, 2026 | 20,000 | 21,292 | 1,292 | 474,443 |

| Nov 1, 2026 | 20,000 | 21,350 | 1,350 | 475,793 |

| May 1, 2027 | 20,000 | 21,411 | 1,411 | 477,203 |

| Nov 1, 2027 | 20,000 | 21,474 | 1,474 | 478,677 |

| May 1, 2028 | 20,000 | 21,540 | 1,540 | 480,218 |

| Nov 1, 2028 | 20,000 | 21,610 | 1,610 | 481,828 |

| May 1, 2029 | 20,000 | 21,682 | 1,682 | 483,510 |

| Nov 1, 2029 | 20,000 | 21,758 | 1,758 | 485,268 |

| May 1, 2030 | 20,000 | 21,837 | 1,837 | 487,105 |

| Nov 1, 2030 | 20,000 | 21,920 | 1,920 | 489,025 |

| May 1, 2031 | 20,000 | 22,006 | 2,006 | 491,031 |

| Nov 1, 2031 | 20,000 | 22,096 | 2,096 | 493,127 |

| May 1, 2032 | 20,000 | 22,191 | 2,191 | 495,318 |

| Nov 1, 2032 | 20,000 | 22,289 | 2,289 | 497,607 |

| May 1, 2033 | 20,000 | 22,392 | 2,392 | 500,000 |

Using the information from the schedule, the entries are completed below.

To record the interest payment on November 1:

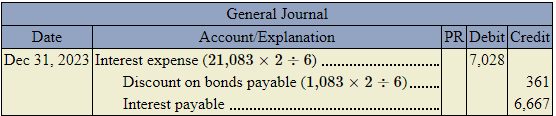

Recording the accrued interest at the December 31 year-end uses the relevant portion of the effective interest schedule. For example, at December 31, 2023, the table shows interest of $21,083 and bond amortization of $1,083 at May, 2024. Prorating these amounts for November and December, or two months, results in the following entry

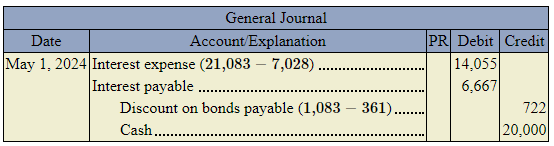

To record the interest payment on May 1, 2024, interest expense and amortization will be for the remainder of the table amounts of $21,083 and $1,083 respectively:

At maturity, the May 1, 2033, entry would be:

Summary of Chapter 9 Learning Objectives

LO1 – Identify and explain current versus long-term liabilities.

Current or short-term liabilities are a form of debt that is expected to be paid within the longer of one year of the balance sheet date or one operating cycle. Long-term liabilities are a form of debt that is expected to be paid beyond one year of the balance sheet date or the next operating cycle, whichever is longer. Current and long-term liabilities must be shown separately on the balance sheet.

LO2 – Record and disclose known current liabilities.

Known current liabilities are those where the payee, amount, and timing of payment are known. Payroll liabilities are a type of known current liability. Employers are responsible for withholding from employees amounts including Employment Insurance (EI), Canada Pension Plan (CPP), and income tax, and then remitting the amounts to the appropriate authority. Sales taxes, including the Goods and Services Tax (GST) and Provincial Sales Tax (PST), must be collected by registrants and subsequently remitted to the Receiver General for Canada. Short-term notes payable, also a known current liability, can involve the accrual of interest if the maturity date falls in the next accounting period.

LO3 – Record and disclose estimated current liabilities.

An estimated liability is known to exist where the amount, although uncertain, can be estimated. Warranties and income taxes are examples of estimated liabilities. Contingent liabilities are neither a known liability nor an estimated liability and are not recorded if they are determined to exist. A contingent liability exists when it is not probable or it cannot be realiably estimated. A contingent liability is disclosed in the notes to the financial statements.

LO4 – Identify, describe, and record bonds.

Bonds pay interest at regular intervals to bondholders. The original investment is repaid to bondholders when the bonds mature. There are different types of bonds: secured or unsecured, as well as registered or bearer bonds. Bonds can have a variety of characteristics, including: varying maturity dates, call provisions, conversion privileges, sinking fund requirements, or dividend restrictions. Bonds are issued: (a) at par (also known as the face value) when the market interest rate is the same as the bond (or contract) interest rate; (b) at a discount when the market interest rate is higher than the bond interest rate; or (c) at a premium when the market interest rate is lower than the bond interest rate.

LO5 – Explain, calculate, and record long-term loans.

A loan is a form of long-term debt that can be used by a corporation to finance its operations. Loans can be secured and are typically obtained from a bank. Loans are often repaid in equal blended payments containing both interest and principal.

- What is the difference between a current and long-term liability?

- What are some examples of known current liabilities?

- How are known current liabilities different from estimated current liabilities?

- What are some examples of estimated current liabilities?

- How is an estimated current liability different from a contingent liability?

- What is a bond? ...a bond indenture? Why might a trustee be used to administer a bond indenture?

- List and explain some bondholder rights.

- How are different bond issues reported in the financial statements of a corporation?

- What are three reasons why bonds might be redeemed before their maturity date?

- Why would investors pay a premium for a corporate bond? Why would a corporation issue its bonds at a discount? Explain, using the relationship between the bond contract interest rate and the prevailing market interest rate.

- How is an unamortised bond premium or discount disclosed in accordance with GAAP?

- If the bond contract interest rate is greater than that required in the market on the date of issue, what is the effect on the selling price of the bond? Why?

- What method is used to amortise premiums and discounts?

- How is a loan payable similar to a bond? How is it different?

- Distinguish between future value and present value. What is the time value of money? Why is it important?

- How is the actual price of a bond determined?