7.1: Internal Control

- Page ID

- 97796

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Use the following as a self-check while working through Chapter 7.

- What constitutes a good system of control over cash?

- What is a petty cash system and how is it used to control cash?

- How is petty cash reported on the balance sheet?

- How does the preparation of a bank reconciliation facilitate control over cash?

- What are the steps in preparing a bank reconciliation?

- How does the estimation of uncollectible accounts receivable address the GAAP of matching?

- How are uncollectible accounts disclosed on financial statements?

- What are the different methods used for estimating uncollectible accounts receivable?

- How is aging of accounts receivable used in estimating uncollectible accounts?

- How are notes receivable recorded?

- What is the acid-test ratio and how is it calculated?

- How is the accounts receivable turnover calculated and what does it mean?

NOTE: The purpose of these questions is to prepare you for the concepts introduced in the chapter. Your goal should be to answer each of these questions as you read through the chapter. If, when you complete the chapter, you are unable to answer one or more the Concept Self-Check questions, go back through the content to find the answer(s). Solutions are not provided to these questions.

7.1 Internal Control

LO1 – Define internal control and explain how it is applied to cash.

Assets are the lifeblood of a company. As such, they must be protected. This duty falls to managers of a company. The policies and procedures implemented by management to protect assets are collectively referred to as internal controls. An effective internal control program not only protects assets, but also aids in accurate recordkeeping, produces financial statement information in a timely manner, ensures compliance with laws and regulations, and promotes efficient operations. Effective internal control procedures ensure that adequate records are maintained, transactions are authorized, duties among employees are divided between recordkeeping functions and control of assets, and employees' work is checked by others. The use of electronic recordkeeping systems does not decrease the need for good internal controls.

The effectiveness of internal controls is limited by human error and fraud. Human error can occur because of negligence or mistakes. Fraud is the intentional decision to circumvent internal control systems for personal gain. Sometimes, employees cooperate in order to avoid internal controls. This collusion is often difficult to detect, but fortunately, it is not a common occurrence when adequate controls are in place.

Internal controls take many forms. Some are broadly based, like mandatory employee drug testing, video surveillance, and scrutiny of company email systems. Others are specific to a particular type of asset or process. For instance, internal controls need to be applied to a company's accounting system to ensure that transactions are processed efficiently and correctly to produce reliable records in a timely manner. Procedures should be documented to promote good recordkeeping, and employees need to be trained in the application of internal control procedures.

Financial statements prepared according to generally accepted accounting principles are useful not only to external users in evaluating the financial performance and financial position of the company, but also for internal decision making. There are various internal control mechanisms that aid in the production of timely and useful financial information. For instance, using a chart of accounts is necessary to ensure transactions are recorded in the appropriate account. As an example, expenses are classified and recorded in applicable expense accounts, then summarized and evaluated against those of a prior year.

The design of accounting records and documents is another important means to provide financial information. Financial data is entered and summarized in records and transmitted by documents. A good system of internal control requires that these records and documents be prepared at the time a transaction takes place or as soon as possible afterward, since they become less credible and the possibility of error increases with the passage of time. The documents should also be consecutively pre-numbered, to indicate whether there may be missing documents.

Internal control also promotes the protection of assets. Cash is particularly vulnerable to misuse. A good system of internal control for cash should provide adequate procedures for protecting cash receipts and cash payments (commonly referred to as cash disbursements). Procedures to achieve control over cash vary from company to company and depend upon such variables as company size, number of employees, and cash sources. However, effective cash control generally requires the following:

- Separation of duties: People responsible for handling cash should not be responsible for maintaining cash records. By separating the custodial and record-keeping duties, theft of cash is less likely.

- Same-day deposits: All cash receipts should be deposited daily in the company's bank account. This prevents theft and personal use of the money before deposit.

- Payments made using non-cash means: Cheques or electronic funds transfer (EFT) provide a separate external record to verify cash disbursements. For example, many businesses pay their employees using electronic funds transfer because it is more secure and efficient than using cash or even cheques.

Two forms of internal control over cash will be discussed in this chapter: the use of a petty cash account and the preparation of bank reconciliations.

7.2 Petty Cash

LO2 – Explain and journalize petty cash transactions.

The payment of small amounts by cheque may be inconvenient and costly. For example, using cash to pay for postage on an incoming package might be less than the total processing cost of a cheque. A small amount of cash kept on hand to pay for small, infrequent expenses is referred to as a petty cash fund.

Establishing and Reimbursing the Petty Cash Fund

To set up the petty cash fund, a cheque is prepared for the amount of the fund. The custodian of the fund cashes the cheque and places the coins and currency in a locked box. Responsibility for the petty cash fund should be delegated to only one person, who should be held accountable for its contents. Cash payments are made by this petty cash custodian out of the fund as required when supported by receipts. When the amount of cash has been reduced to a pre-determined level, the receipts are compiled and submitted for entry into the accounting system. A cheque is then issued to reimburse the petty cash fund. At any given time, the petty cash amount should consist of cash and supporting receipts, all totalling the petty cash fund amount. To demonstrate the management of a petty cash fund, assume that a $200 cheque is issued for the purpose of establishing a petty cash fund.

The journal entry is:

Petty Cash is a current asset account. When reporting Cash on the financial statements, the balances in Petty Cash and Cash are added together and reported as one amount.

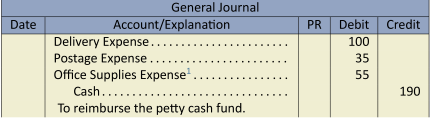

Assume the petty cash custodian has receipts totalling $190 and $10 in coin and currency remaining in the petty cash box. The receipts consist of the following: delivery charges $100, $35 for postage, and office supplies of $55. The petty cash custodian submits the receipts to the accountant who records the following entry and issues a cheque for $190.

The petty cash receipts should be cancelled at the time of reimbursement in order to prevent their reuse for duplicate reimbursements. The petty cash custodian cashes the $190 cheque. The $190 plus the $10 of coin and currency in the locked box immediately prior to reimbursement equals the $200 total required in the petty cash fund.

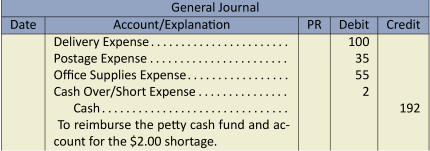

Sometimes, the receipts plus the coin and currency in the petty cash locked box do not equal the required petty cash balance. To demonstrate, assume the same information above except that the coin and currency remaining in the petty cash locked box was $8. This amount plus the receipts for $190 equals $198 and not $200, indicating a shortage in the petty cash box. The entry at the time of reimbursement reflects the shortage and is recorded as:

Notice that the $192 credit to Cash plus the $8 of coin and currency remaining in the petty cash box immediately prior to reimbursement equals the $200 required total in the petty cash fund.

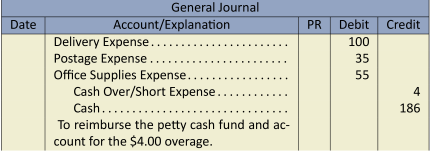

Assume, instead, that the coin and currency in the petty cash locked box was $14. This amount plus the receipts for $190 equals $204 and not $200, indicating an overage in the petty cash box. The entry at the time of reimbursement reflects the overage and is recorded as:

Again, notice that the $186 credit to Cash plus the $14 of coin and currency remaining in the petty cash box immediately prior to reimbursement equals the $200 required total in the petty cash fund.

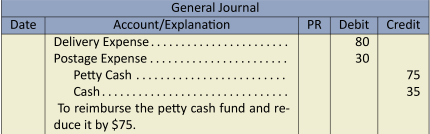

What happens if the petty cash custodian finds that the fund is rarely used? In such a case, the size of the fund should be decreased to reduce the risk of theft. To demonstrate, assume the petty cash custodian has receipts totalling $110 and $90 in coin and currency remaining in the petty cash box. The receipts consist of the following: delivery charges $80 and postage $30. The petty cash custodian submits the receipts to the accountant and requests that the petty cash fund be reduced by $75. The following entry is recorded and a cheque for $35 is issued.

The $35 credit to Cash plus the $90 of coin and currency remaining in the petty cash box immediately prior to reimbursement equals the $125 new balance in the petty cash fund ($200 original balance less the $75 reduction).

In cases when the size of the petty cash fund is too small, the petty cash custodian could request an increase in the size of the petty cash fund at the time of reimbursement. Care should be taken to ensure that the size of the petty cash fund is not so large as to become a potential theft issue. Additionally, if a petty cash fund is too large, it may be an indicator that transactions that should be paid by cheque are not being processed in accordance with company policy. Remember that the purpose of the petty cash fund is to pay for infrequent expenses; day-to-day items should not go through petty cash.

7.3 Cash Collections and Payments

LO3 – Explain the purpose of and prepare a bank reconciliation, and record related adjustments.

The widespread use of banks facilitates cash transactions between entities and provides a safeguard for the cash assets being exchanged. This involvement of banks as intermediaries between entities has accounting implications. At any point in time, the cash balance in the accounting records of a particular company usually differs from the bank cash balance of that company. The difference is usually because some cash transactions recorded in the accounting records have not yet been recorded by the bank and, conversely, some cash transactions recorded by the bank have not yet been recorded in the company's accounting records.

The use of a bank reconciliation is one method of internal control over cash. The reconciliation process brings into agreement the company's accounting records for cash and the bank statement issued by the company's bank. A bank reconciliation explains the difference between the balances reported by the company and by the bank on a given date.

A bank reconciliation proves the accuracy of both the company's and the bank's records, and reveals any errors made by either party. The bank reconciliation is a tool that can help detect attempts at theft and manipulation of records. The preparation of a bank reconciliation is discussed in the following section.

The Bank Reconciliation

The bank reconciliation is a report prepared by a company at a point in time. It identifies discrepancies between the cash balance reported on the bank statement and the cash balance reported in a business's Cash account in the general ledger, more commonly referred to as the books. These discrepancies are known as reconciling items and are added or subtracted to either the book balance or bank balance of cash. Each of the reconciling items is added or subtracted to the business's cash balance. The business's cash balance will change as a result of the reconciling items. The cash balance prior to reconciliation is called the unreconciled cash balance. The balance after adding and subtracting the reconciling items is called the reconciled cash balance. The following is a list of potential reconciling items and their impact on the bank reconciliation.

| Book reconciling items | Bank reconciling items |

|---|---|

| Collection of notes receivable (added) | Outstanding deposits (added) |

| NSF cheques (subtracted) | Outstanding cheques (subtracted) |

| Bank charges (subtracted) | |

| Book errors (added or subtracted, | Bank errors (added or subtracted, |

| depending on the nature of the error) | depending on the nature of the error) |

Book Reconciling Items

The collection of notes receivable may be made by a bank on behalf of the company. These collections are often unknown to the company until they appear as an addition on the bank statement, and so cause the general ledger cash account to be understated. As a result, the collection of a notes receivable is added to the unreconciled book balance of cash on the bank reconciliation.

Cheques returned to the bank because there were not sufficient funds (NSF) to cover them appear on the bank statement as a reduction of cash. The company must then request that the customer pay the amount again. As a result, the general ledger cash account is overstated by the amount of the NSF cheque. NSF cheques must therefore be subtracted from the unreconciled book balance of cash on the bank reconciliation to reconcile cash.

Cheques received by a company and deposited into its bank account may be returned by the customer's bank for a number of reasons (e.g., the cheque was issued too long ago, known as a stale-dated cheque, an unsigned or illegible cheque, or the cheque shows the wrong account number). Returned cheques cause the general ledger cash account to be overstated. These cheques are therefore subtracted on the bank statement, and must be deducted from the unreconciled book balance of cash on the bank reconciliation.

Bank service charges are deducted from the customer's bank account. Since the service charges have not yet been recorded by the company, the general ledger cash account is overstated. Therefore, service charges are subtracted from the unreconciled book balance of cash on the bank reconciliation.

A business may incorrectly record journal entries involving cash. For instance, a deposit or cheque may be recorded for the wrong amount in the company records. These errors are often detected when amounts recorded by the company are compared to the bank statement. Depending on the nature of the error, it will be either added to or subtracted from the unreconciled book balance of cash on the bank reconciliation. For example, if the company recorded a cheque as $520 when the correct amount of the cheque was $250, the $270 difference would be added to the unreconciled book balance of cash on the bank reconciliation. Why? Because the cash balance reported on the books is understated by $270 as a result of the error. As another example, if the company recorded a deposit as $520 when the correct amount of the deposit was $250, the $270 difference would be subtracted from the unreconciled book balance of cash on the bank reconciliation. Why? Because the cash balance reported on the books is overstated by $270 as a result of the error. Each error requires careful analysis to determine whether it will be added or subtracted in the unreconciled book balance of cash on the bank reconciliation.

Bank Reconciling Items

Cash receipts are recorded as an increase of cash in the company's accounting records when they are received. These cash receipts are deposited by the company into its bank. The bank records an increase in cash only when these amounts are actually deposited with the bank. Since not all cash receipts recorded by the company will have been recorded by the bank when the bank statement is prepared, there will be outstanding deposits, also known as deposits in transit. Outstanding deposits cause the bank statement cash balance to be understated. Therefore, outstanding deposits are a reconciling item that must be added to the unreconciled bank balance of cash on the bank reconciliation.

On the date that a cheque is prepared by a company, it is recorded as a reduction of cash in a company's books. A bank statement will not record a cash reduction until a cheque is presented and accepted for payment (or clears the bank). Cheques that are recorded in the company's books but are not paid out of its bank account when the bank statement is prepared are referred to as outstanding cheques. Outstanding cheques mean that the bank statement cash balance is overstated. Therefore, outstanding cheques are a reconciling item that must be subtracted from the unreconciled bank balance of cash on the bank reconciliation.

Bank errors sometimes occur and are not revealed until the transactions on the bank statement are compared to the company's accounting records. When an error is identified, the company notifies the bank to have it corrected. Depending on the nature of the error, it is either added to or subtracted from the unreconciled bank balance of cash on the bank reconciliation. For example, if the bank cleared a cheque as $520 that was correctly written for $250, the $270 difference would be added to the unreconciled bank balance of cash on the bank reconciliation. Why? Because the cash balance reported on the bank statement is understated by $270 as a result of this error. As another example, if the bank recorded a deposit as $520 when the correct amount was actually $250, the $270 difference would be subtracted from the unreconciled bank balance of cash on the bank reconciliation. Why? Because the cash balance reported on the bank statement is overstated by $270 as a result of this specific error. Each error must be carefully analyzed to determine how it will be treated on the bank reconciliation.

Illustrative Problem—Bank Reconciliation

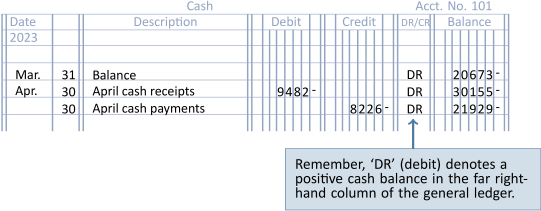

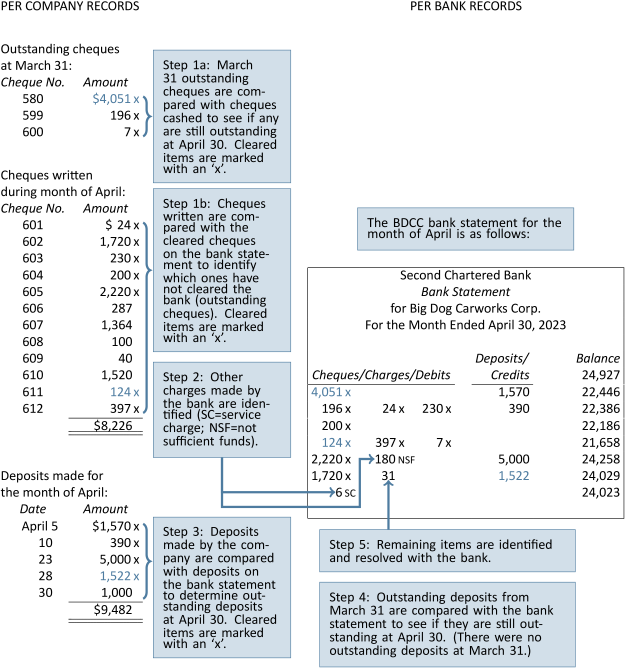

Assume that a bank reconciliation is prepared by Big Dog Carworks Corp. (BDCC) at April 30. At this date, the Cash account in the general ledger shows a balance of $21,929 and includes the cash receipts and payments shown in Figure 7.1.

Extracts from BDCC's accounting records are reproduced with the bank statement for April in Figure 7.2.

For each entry in BDCC's general ledger Cash account, there should be a matching entry on its bank statement. Items in the general ledger Cash account but not on the bank statement must be reported as a reconciling item on the bank reconciliation. For each entry on the bank statement, there should be a matching entry in BDCC's general ledger Cash account. Items on the bank statement but not in the general ledger Cash account must be reported as a reconciling item on the bank reconciliation.

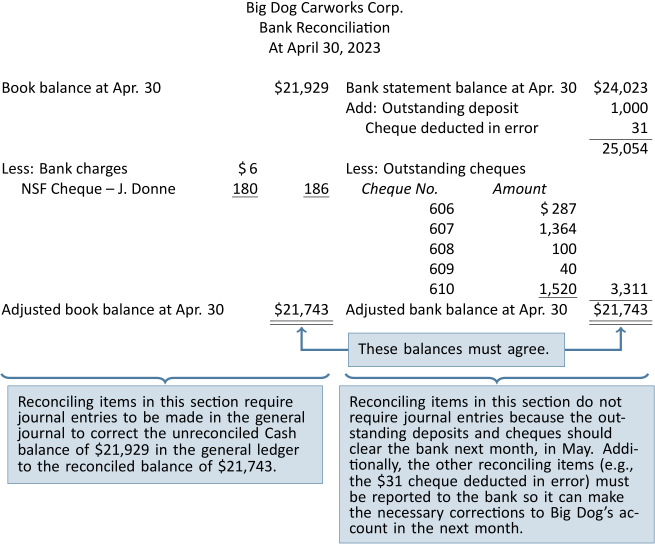

There are nine steps to follow in preparing a bank reconciliation for BDCC at April 30, 2023:

Step 1

Identify the ending general ledger cash balance ($21,929 from Figure 7.1) and list it on the bank reconciliation as the book balance on April 30 as shown in Figure 7.3. This represents the unreconciled book balance.

Step 2

Identify the ending cash balance on the bank statement ($24,023 from Figure 7.2) and list it on the bank reconciliation as the bank statement balance on April 30 as shown in Figure 7.3. This represents the unreconciled bank balance.

Step 3

Cheques written that have cleared the bank are returned with the bank statement. These cheques are said to be cancelled because, once cleared, the bank marks them to prevent them from being used again. Cancelled cheques are compared to the company's list of cash payments. Outstanding cheques are identified using two steps:

- Any outstanding cheques listed on the BDCC's March 31 bank reconciliation are compared to the cheques listed on the April 30 bank statement.

For BDCC, all of the March outstanding cheques (nos. 580, 599, and 600) were paid by the bank in April. Therefore, there are no reconciling items to include in the April 30 bank reconciliation. If one of the March outstanding cheques had not been paid by the bank in April, it would be subtracted as an outstanding cheque from the unreconciled bank balance on the bank reconciliation.

- The cash payments listed in BDCC's accounting records are compared to the cheques on the bank statement. This comparison indicates that the following cheques are outstanding.

Cheque No. Amount 606 $ 287 607 1,364 608 100 609 40 610 1,520 Outstanding cheques must be deducted from the bank statement's unreconciled ending cash balance of $24,023 as shown in Figure 7.3.

Step 4

Other payments made by the bank are identified on the bank statement and subtracted from the unreconciled book balance on the bank reconciliation.

- An examination of the April bank statement shows that the bank had deducted the NSF cheque of John Donne for $180. This is deducted from the unreconciled book balance on the bank reconciliation as shown in Figure 7.3.

- An examination of the April 30 bank statement shows that the bank had also deducted a service charge of $6 during April. This amount is deducted from the unreconciled book balance on the bank reconciliation as shown in Figure 7.3.

Step 5

Last month's bank reconciliation is reviewed for outstanding deposits at March 31. There were no outstanding deposits at March 31. If there had been, the amount would have been added to the unreconciled bank balance on the bank reconciliation.

Step 6

The deposits shown on the bank statement are compared with the amounts recorded in the company records. This comparison indicates that the April 30 cash receipt amounting to $1,000 was deposited but it is not included in the bank statement. The outstanding deposit is added to the unreconciled bank balance on the bank reconciliation as shown in Figure 7.3.

Step 7

Any errors in the company's records or in the bank statement must be identified and reported on the bank reconciliation.

An examination of the April bank statement shows that the bank deducted a cheque issued by another company for $31 from the BDCC bank account in error. Assume that when notified, the bank indicated it would make a correction in May's bank statement.

The cheque deducted in error must be added to the bank statement balance on the bank reconciliation as shown in Figure 7.3.

Step 8

Total both sides of the bank reconciliation. The result must be that the book balance and the bank statement balance are equal or reconciled. These balances represent the adjusted balance.

The bank reconciliation in Figure 7.3 is the result of completing the preceding eight steps.

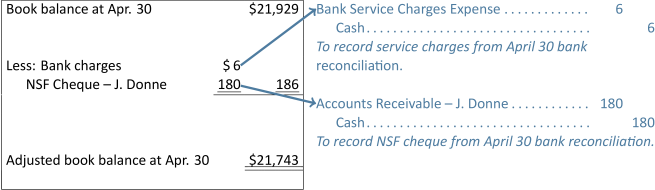

Step 9

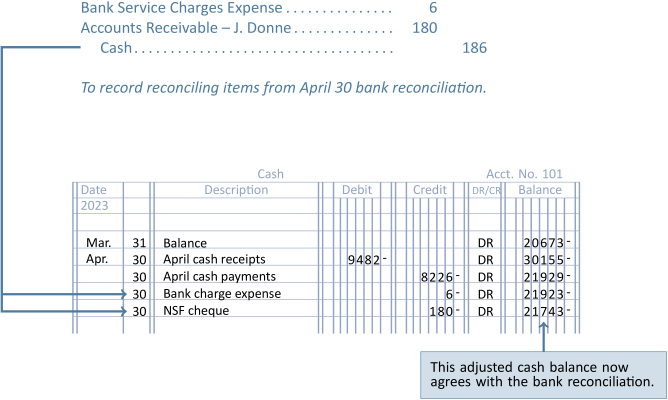

For the adjusted balance calculated in the bank reconciliation to appear in the accounting records, an adjusting entry(s) must be prepared.

The adjusting entry(s) is based on the reconciling item(s) used to calculate the adjusted book balance. The book balance side of BDCC's April 30 bank reconciliation is copied to the left below to clarify the source of the following April 30 adjustments.

It is common practice to use one compound entry to record the adjustments resulting from a bank reconciliation as shown below for BDCC.

Once the adjustment is posted, the Cash general ledger account is up to date, as illustrated in Figure 7.4.

Note that the balance of $21,743 in the general ledger Cash account is the same as the adjusted book balance of $21,743 on the bank reconciliation. Big Dog does not make any adjusting entries for the reconciling items on the bank side of the bank reconciliation since these will eventually clear the bank and appear on a later bank statement. Bank errors will be corrected by the bank.

Debit and Credit Card Transactions

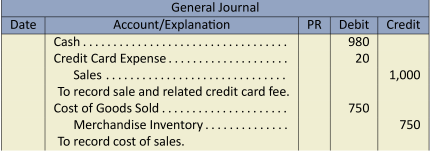

Debit and credit cards are commonly accepted by companies when customers make purchases. Because the cash is efficiently and safely transferred directly into a company's bank account by the debit or credit card company, such transactions enhance internal control over cash. However, the seller is typically charged a fee for accepting debit and credit cards. For example, assume BDCC makes a $1,000 sale to a customer who uses a credit card that charges BDCC a fee of 2%; the cost of the sale is $750. BDCC would record:

The credit card fee is calculated as the ![]() . This means that BDCC collects net cash proceeds of $980 (

. This means that BDCC collects net cash proceeds of $980 (![]() ). The use of debit cards also involves fees and these would be journalized in the same manner.

). The use of debit cards also involves fees and these would be journalized in the same manner.

7.4 Accounts Receivable

LO4 – Explain, calculate, and record estimated uncollectible accounts receivable and subsequent write-offs and recoveries.

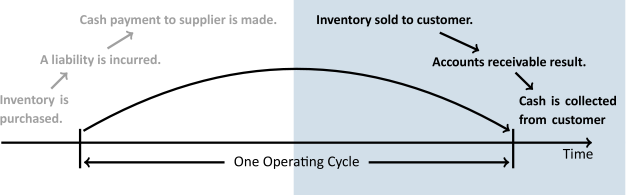

Recall from Chapter 5 that the revenue portion of the operating cycle, as copied in Figure 7.5, begins with a sale on credit and is completed with the collection of cash. Unfortunately, not all receivables are collected. This section discusses issues related to accounts receivable and their collection.

Uncollectible Accounts Receivable

Extending credit to customers results in increased sales and therefore profits. However, there is a risk that some accounts receivable will not be collected. A good internal control system is designed to minimize bad debt losses. One such control is to permit sales on account only to credit-worthy customers; this can be difficult to determine in advance. Companies with credit sales realize that some of these amounts may never be collected. Uncollectible accounts, commonly known as bad debts, are an expense associated with selling on credit.

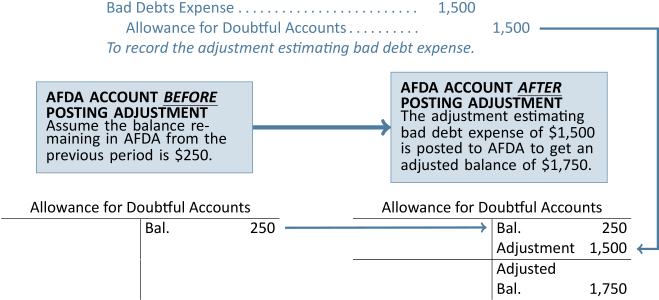

Bad debt expenses must be matched to the credit sales of the same period. For example, assume BDCC recorded a $1,000 credit sale to XYA Company in April, 2015. Assume further that in 2016 it was determined that the $1,000 receivable from XYA Company would never be collected. The bad debt arising from the credit sale to XYA Company should be matched to the period in which the sale occurred, namely, April, 2015. But how can that be done if it is not known which receivables will become uncollectible? A means of estimating and recording the amount of sales that will not be collected in cash is needed. This is done by establishing a contra current asset account called Allowance for Doubtful Accounts (AFDA) in the general ledger to record estimated uncollectible receivables. This account is a contra account to accounts receivable and is disclosed on the balance sheet as shown below using assumed values.

| Accounts receivable | $25,000 | |

| Less: Allowance for doubtful accounts | 1,400 | 23,600 |

| OR | ||

| Accounts receivable (net of $1,400 AFDA) | $ 23,600 |

The Allowance for Doubtful Accounts contra account reduces accounts receivable to the amount that is expected to be collected — in this case, $23,600.

Estimating Uncollectible Accounts Receivable

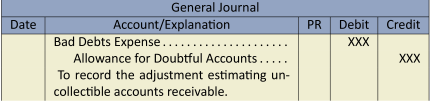

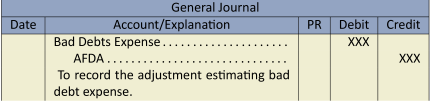

The AFDA account is used to reflect how much of the total Accounts Receivable is estimated to be uncollectible. To record estimated uncollectible accounts, the following adjusting entry is made.

The bad debt expense is shown on the income statement. AFDA appears on the balance sheet and is subtracted from accounts receivable resulting in the estimated net realizable accounts receivable.

Two different methods can be used to estimate uncollectible accounts. One method focuses on estimating Bad Debt Expense on the income statement, while the other focuses on estimating the desired balance in AFDA on the balance sheet.

The Income Statement Method

The objective of the income statement method is to estimate bad debt expense based on credit sales. Bad debt expense is calculated by applying an estimated loss percentage to credit sales for the period. The percentage is typically based on actual losses experienced in prior years. For instance, a company may have the following history of uncollected sales on account:

| Year | Credit Sales | Amounts Not Collected |

|---|---|---|

| 2020 | $150,000 | $1,000 |

| 2021 | 200,000 | 1,200 |

| 2022 | 250,000 | 800 |

| $600,000 | $3,000 |

The average loss over these years is ![]() , or

, or ![]() of 1%. If management anticipates that similar losses can be expected in 2023 and credit sales for 2023 amount to $300,000, bad debts expense would be estimated as $1,500 ($300,000 x 0.005). Under the income statement method, the $1,500 represents estimated bad debt expense and is recorded as:

of 1%. If management anticipates that similar losses can be expected in 2023 and credit sales for 2023 amount to $300,000, bad debts expense would be estimated as $1,500 ($300,000 x 0.005). Under the income statement method, the $1,500 represents estimated bad debt expense and is recorded as:

This estimated bad debt expense is calculated without considering any existing balance in the AFDA account.

The Balance Sheet Method

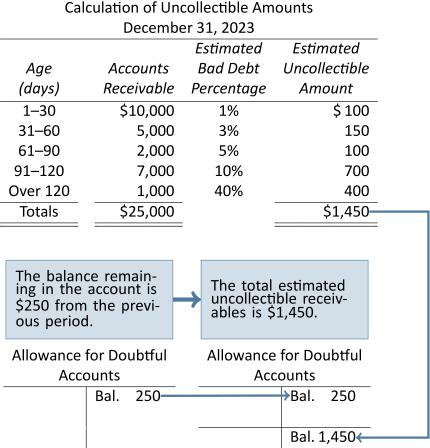

Estimated uncollectible accounts can also be calculated by using the balance sheet method where a process called aging of accounts receivable is used. At the end of the period, the total of estimated uncollectible accounts is calculated by analyzing accounts receivable according to how long each account has been outstanding. An aging analysis approach assumes that the longer a receivable is outstanding, the less chance there is of collecting it. This process is illustrated in the following schedule.

| Aging of Accounts Receivable | ||||||||||||||

| December 31, 2023 | ||||||||||||||

| Number of Days Past Due | ||||||||||||||

| Customer | Total | Not Yet Due | 1–30 | 31–60 | 61–90 | 91–120 | Over 120 | |||||||

| Bendix Inc. | $ | 1,000 | $ | 1,000 | ||||||||||

| Devco Marketing Inc. | 6,000 | $ | 1,000 | $ | 3,000 | $ | 2,000 | |||||||

| Horngren Corp | 4,000 | 2,000 | 1,000 | $ | 1,000 | |||||||||

| Perry Co. Ltd. | 5,000 | 3,000 | 1,000 | 1,000 | ||||||||||

| Others | 9,000 | 4,000 | 5,000 | |||||||||||

| Totals | $ | 25,000 | $ | 0 | $ | 10,000 | $ | 5,000 | $ | 2,000 | $ | 7,000 | $ | 1,000 |

In this example, accounts receivable total $25,000 at the end of the period. These are classified into six time periods: those receivables that are not yet due; 1–30 days past due; 31–60 days past due; 61–90 days past due; 91–120 days past due; and over 120 days past due.

Based on past experience, assume management estimates a bad debt percentage, or rate of uncollectibility, for each time period as follows:

| Number of Days Outstanding | Not Yet Due | 1–30 | 31–60 | 61–90 | 91–120 | Over 120 |

| Rate of Uncollectibility | 0.5% | 1% | 3% | 5% | 10% | 40% |

The calculation of expected uncollectible accounts receivable at December 31, 2023 would be as follows:

A total of $1,450 of accounts receivable is estimated to be uncollectible at December 31, 2023.

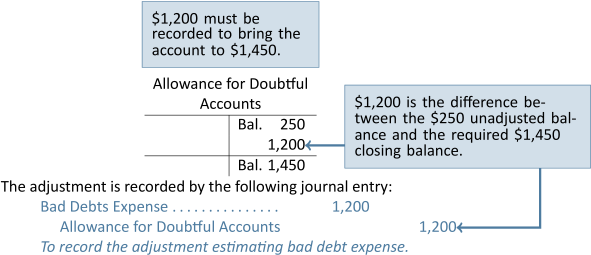

Under the balance sheet method, the estimated bad debt expense consists of the difference between the opening AFDA balance ($250, as in the prior example) and the estimated uncollectible receivables ($1,450) required at year-end.

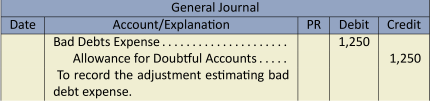

As an alternative to using an aging analysis to estimate uncollectible accounts, a simplified balance sheet method can be used. The simplified balance sheet method calculates the total estimated uncollectible accounts as a percentage of the outstanding accounts receivables balance. For example, assume an unadjusted balance in AFDA of $250 as in the preceding example. Also assume the accounts receivable balance at the end of the period was $25,000 as in the previous illustration. If it was estimated that 6% of these would be uncollectible based on historical data, the adjustment would be:

The total estimated uncollectible accounts was $1,500 ($25,000 ![]() 0.06). Given an unadjusted balance in AFDA of $250, the adjustment to AFDA must be a credit of $1,250 ($1,500 – $250).

0.06). Given an unadjusted balance in AFDA of $250, the adjustment to AFDA must be a credit of $1,250 ($1,500 – $250).

Regardless of whether the income statement method or balance sheet method is used, the amount estimated as an allowance for doubtful accounts seldom agrees with the amounts that actually prove uncollectible. A credit balance remains in the allowance account if fewer bad debts occur during the year than are estimated. There is a debit balance in the allowance account if more bad debts occur during the year than are estimated. By monitoring the balance in the Allowance for Doubtful Accounts general ledger account at each year-end, though, management can determine whether the estimates of uncollectible amounts are accurate. If not, they can adjust these estimates going forward.

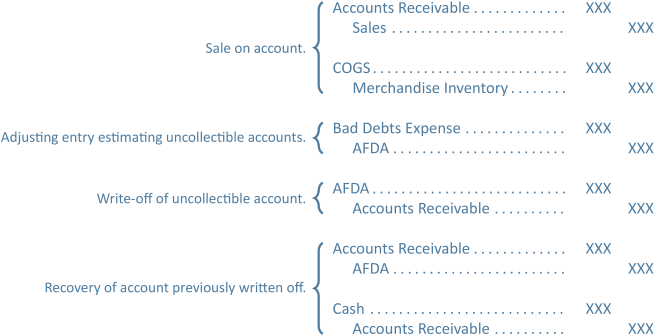

Writing Off Accounts Receivable

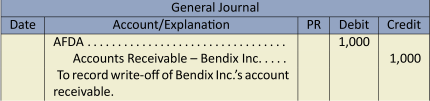

When recording the adjusting entry to estimate uncollectible accounts receivable at the end of the period, it is not known which specific receivables will become uncollectible. When an account is determined to be uncollectible, it must be removed from the accounts receivable account. This process is known as a write-off. To demonstrate the write-off of an account receivable, assume that on January 15, 2024 the $1,000 credit account for customer Bendix Inc. is identified as uncollectible because of the company's bankruptcy. The receivable is removed by:

The $1,000 write-off reduces both the accounts receivable and AFDA accounts. The write-off does not affect net realizable accounts receivable as demonstrated below.

| Before Write-Off | Write-Off | After Write-Off | |

| Accounts receivable | $25,000 | Cr 1,000 | $24,000 |

| Less: Allowance for doubtful accounts | 1,450 | Dr 1,000 | 450 |

| Net accounts receivable | $23,550 | $23,550 |

Additionally, a write-off does not affect bad debt expense. This can be a challenge to understand. To help clarify, recall that the adjusting entry to estimate uncollectibles was:

This adjustment was recorded because GAAP requires that the bad debt expense be matched to the period in which the sales occurred even though it is not known which receivables will become uncollectible. Later, when an uncollectible receivable is identified, it is written off as:

Notice that the AFDA entries cancel each other out so that the net effect is a debit to bad debt expense and a credit to accounts receivable. The use of the AFDA contra account allows us to estimate uncollectible accounts in one period and record the write-off of bad receivables as they become known in a later period.

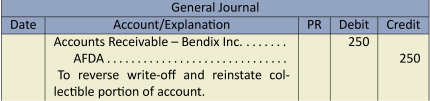

Recovery of a Write-Off

When Bendix Inc. went bankrupt, its debt to Big Dog Carworks Corp. was written off in anticipation that there would be no recovery of the amount owed. Assume that later, an announcement was made that 25% of amounts owed by Bendix would be paid. This new information indicates that BDCC will be able to recover a portion of the receivable previously written off. A recovery requires two journal entries. The first entry reinstates the amount expected to be collected by BDCC—$250

($1,000 ![]() 25%) in this case and is recorded as:

25%) in this case and is recorded as:

This entry reverses the collectible part of the receivable previously written off. The effect of the reversal is shown below.

| Accounts Receivable | Allowance for Doubtful Accounts | ||||||

|---|---|---|---|---|---|---|---|

| Bal. | $25,000 | Bal. | 1,450 | ||||

| Write-off | 1,000 | Write-off | 1,000 | ||||

| Recovery | 250 | Recovery | 250 | ||||

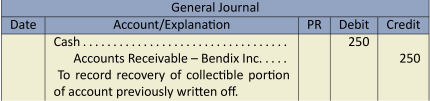

The second entry records the collection of the reinstated amount as:

The various journal entries related to accounts receivable are summarized below.

7.5 Short-Term Notes Receivable

LO5 – Explain and record a short-term notes receivable as well as calculate related interest.

Short-term notes receivable are current assets, since they are due within the greater of 12 months or the business's operating cycle. A note receivable is a promissory note. A promissory note is a signed document where the debtor, the person who owes the money, promises to pay the creditor the principal and interest on the due date. The principal is the amount owed. The creditor, or payee, is the entity owed the principal and interest. Interest is the fee for using the principal and is calculated as: Principal ![]() Annual Interest Rate

Annual Interest Rate ![]() Time. The time or term of the note is the period from the date of the note to the due date. The due date, also known as the maturity date, is the date on which the principal and interest must be paid. The date of the note is the date the note begins accruing interest.

Time. The time or term of the note is the period from the date of the note to the due date. The due date, also known as the maturity date, is the date on which the principal and interest must be paid. The date of the note is the date the note begins accruing interest.

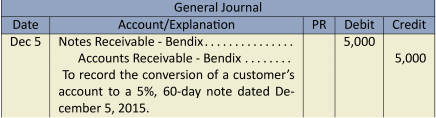

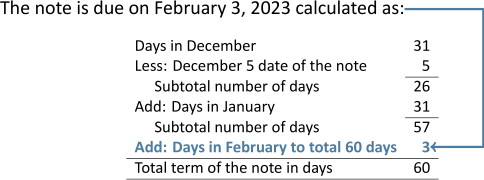

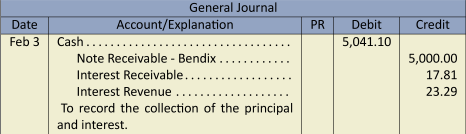

Short-term notes receivable can arise at the time of sale or when a customer's account receivable becomes overdue. To demonstrate the conversion of a customer's account to a short-term receivable, assume that BDCC's customer Bendix Inc. is unable to pay its $5,000 account within the normal 30-day period. The receivable is converted to a 5%, 60-day note dated December 5, 2023 with the following entry:

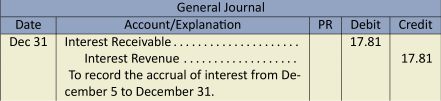

Assuming a December 31, year-end for BDCC, the adjusting entry to accrue interest on December 31 would be:

The interest of $17.81 was calculated as: $5,000 ![]() 5%

5% ![]() 26/3652 = $17.80822 rounded to $17.81. All interest calculations in this textbook are rounded to two decimal places.

26/3652 = $17.80822 rounded to $17.81. All interest calculations in this textbook are rounded to two decimal places.

At maturity, February 3, 2024, BDCC collects the note plus interest and records:

The total interest realized on the note was $41.10 ($5,000 ![]() 5%

5% ![]() 60/365 = $41.0959 rounded to $41.10). Part of the $41.10 total interest revenue was realized in 2023 ($17.81) and the rest in 2024 ($41.10 - $17.81 = $23.29). Therefore, care must be taken to correctly allocate the interest between periods. The total cash received by BDCC on February 3 was the sum of the principal and interest: $5,000.00 + $41.10 = $5,041.10.

60/365 = $41.0959 rounded to $41.10). Part of the $41.10 total interest revenue was realized in 2023 ($17.81) and the rest in 2024 ($41.10 - $17.81 = $23.29). Therefore, care must be taken to correctly allocate the interest between periods. The total cash received by BDCC on February 3 was the sum of the principal and interest: $5,000.00 + $41.10 = $5,041.10.

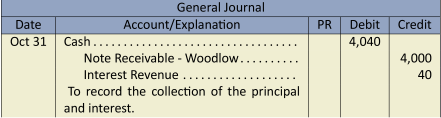

When the term of a note is expressed in months, the calculations are less complex. For example, assume that BDCC sold customer Woodlow a $4,000 service on August 1, 2023. On that date, the customer signed a 4%, 3-month note. The term of the note is based on months and not days therefore the maturity date is October 31, 2023. BDCC would record the collection on October 31 as:

The total interest realized on the note was $40 ($4,000 ![]() 4%

4% ![]() 3/123 = $40.00)

3/123 = $40.00)

7.6 Appendix A: Ratio Analysis—Acid Test

LO6 – Explain and calculate the acid-test ratio.

The acid-test ratio, also known as the quick ratio, is a liquidity ratio that is a strict measure of a business's availability of cash to pay current liabilities as they come due. It is considered a strict measure because it includes only quick current assets. Quick current assets are those current assets that are one step away from becoming cash. For example, accounts receivable are a quick current asset because collection of receivables results in cash. However, inventory is not a quick current asset because it is two steps from cash — it has to be sold which creates an account receivable and the receivable then has to be collected. Prepaids are not a quick current asset because the intent in holding prepaids is not to convert them into cash but, instead, to use them (e.g., prepaid insurance becomes insurance expense as it is used). Quick current assets include only cash, short-term investments, and receivables.

The acid-test ratio is calculated as:

| Quick current assets | Current liabilities |

The acid-test ratios for three companies operating in a similar industry are shown below:

| Acid-Test Ratios | |||

| Year | Company A | Company B | Company C |

| 2022 | 0.56 | 1.3 | 8.6 |

| 2023 | 0.72 | 1.2 | 8.7 |

In 2022, Company A's acid-test ratio shows that it has only $0.56 to cover each $1.00 of current liabilities as they come due. Company A therefore has a liquidity issue. Although Company A's acid-test ratio is still unfavourable in 2023, the change is favourable because the liquidity improved. So a company can have an unfavourable acid-test ratio but show a favourable change.

Company B's 2022 acid-test shows that it has favourable liquidity: $1.30 to cover each $1.00 of current liabilities as they come due. However, the change from 2022 to 2023 shows a decrease in the acid-test ratio which is unfavourable although Company B's acid-test still shows favourable liquidity. So a company can have a favourable acid-test ratio but an unfavourable change.

Company C's 2022 acid-test ratio indicates that it has favourable liquidity: $8.60 to cover each $1.00 of current liabilities as they come due. However, this is actually unfavourable because a company can have an acid-test ratio that is too high. If the acid-test ratio is too high, it is a reflection that the company has idle assets. Idle assets do not typically generate the most optimum levels of revenue. Remember that the purpose of holding assets is to generate revenue. In 2023, Company C's acid-test ratio increased a bit and it is still excessive which is unfavourable. So the change was favourable but because the ratio is too high, it reflects an unfavourable liquidity position, though for different reasons than Company A.

7.7 Appendix B: Ratio Analysis—Accounts Receivable Turnover

LO7 – Explain and calculate the accounts receivable turnover.

The accounts receivable turnover not only measures the liquidity of receivables but also the efficiency of collection, referred to as turnover (i.e., accounts receivable turnover into cash). A low turnover indicates high levels of accounts receivable which has an unfavourable impact on liquidity since cash is tied up in receivables. A low turnover means management might need to review credit granting policies and/or strengthen collection efforts.

The accounts receivable turnover is calculated as:

Net credit sales (or revenues) ![]() Average net accounts receivable4

Average net accounts receivable4

Average accounts receivable is calculated by taking the beginning of the period balance plus the end of the period balance and dividing the sum by two.

The accounts receivable turnover ratios for two companies operating in a similar industry are shown below:

| Accounts Receivable Turnover | ||

| Year | Company A | Company B |

| 2023 | 5.8 | 6.9 |

Company B is more efficient at collecting receivables than is Company A. The higher the ratio, the more favourable.

Summary of Chapter 7 Learning Objectives

LO1 – Define internal control and explain how it is applied to cash.

The purpose of internal controls is to safeguard the assets of a business. Since cash is a particularly vulnerable asset, policies and procedures specific to cash need to be implemented, such as the use of cheques and electronic funds transfer for payments, daily cash deposits into a financial institution, and the preparation of bank reconciliations.

LO2 – Explain and journalize petty cash transactions.

A petty cash fund is used to pay small, irregular amounts for which issuing a cheque would be inefficient. A petty cash custodian administers the fund by obtaining a cheque from the cash payments clerk. The cheque is cashed and the coin and currency placed in a locked box. The petty cash custodian collects receipts and reimburses individuals for the related amounts. When the petty cash fund is replenished, the receipts are compiled and submitted for entry in the accounting records so that a replacement cheque can be issued and cashed.

LO3 – Explain the purpose of and prepare a bank reconciliation, and record related adjustments.

A bank reconciliation is a form of internal control that reconciles the bank statement balance to the general ledger cash account, also known as the book balance. Reconciling items that affect the bank statement balance are outstanding deposits, outstanding cheques, and bank errors. Reconciling items that affect the book balance are collections made by the bank on behalf of the company, NSF cheques, bank service charges, and errors. Once the book and bank statement balances are reconciled, an adjusting entry is prepared based on the reconciling items affecting the book balance.

LO4 – Explain, calculate, and record estimated uncollectible accounts receivable and subsequent write-offs and recoveries.

Not all accounts receivable are collected, resulting in uncollectible accounts. Because it is not known which receivables will become uncollectible, the allowance approach is used to match the cost of estimated uncollectible accounts to the period in which the related revenue was generated. The adjusting entry to record estimated uncollectibles is a debit to Bad Debt Expense and a credit to Allowance for Doubtful Accounts (AFDA). The income statement method and the balance sheet method are two ways to estimate and apply the allowance approach. The income statement method calculates bad debt expense based on a percentage of credit sales while the balance sheet method calculates total estimated uncollectible accounts (aka the balance in AFDA) using an aging analysis. When receivables are identified as being uncollectible, they are written off. If write-offs subsequently become collectible, a recovery is recorded using two entries: by reversing the write-off (or the portion that is recoverable) and then journalizing the collection.

LO5 – Explain and record a short-term notes receivable as well as calculate related interest.

A short-term notes receivable is a promissory note that bears an interest rate calculated over the term of the note. Short-term notes receivable are current assets that mature within 12 months from the date of issue or within a business's operating cycle, whichever is longer. Notes can be issued to a customer at the time of sale, or a note receivable can replace an overdue receivable.

LO6 – Explain and calculate the acid-test ratio.

The acid-test ratio is a strict measure of liquidity. It is calculated as quick current assets divided by current liabilities. Quick assets include cash, short-term investments, and accounts receivable.

LO7 – Explain and calculate the accounts receivable turnover.

The accounts receivable turnover is a measure of liquidity and demonstrates how efficiently receivables are being collected. It is calculated as net sales divided by average accounts receivable. Average accounts receivable are the sum of the beginning accounts receivable, including short-term notes receivable from customers, plus ending receivables, divided by two.

- What is internal control?

- How does the preparation of a bank reconciliation strengthen the internal control of cash?

- What are some reconciling items that appear in a bank reconciliation?

- What are the steps in preparing a bank reconciliation?

- What is an NSF cheque?

- What is a petty cash system?

- What is the difference between establishing and replenishing the petty cash fund?

- How does use of allowance for doubtful accounts match expenses with revenue?

- How does the income statement method calculate the estimated amount of uncollectible accounts?

- What is an ageing schedule for bad debts, and how is it used in calculating the estimated amount of uncollectible accounts?

- How are credit balances in accounts receivable reported on the financial statements?