5.9: Exercises

- Page ID

- 98084

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)EXERCISE 5–1 (LO1)

Consider the following information of Jones Corporation over four years:

| 2024 | 2023 | 2022 | 2021 | |

|---|---|---|---|---|

| Sales | $10,000 | $9,000 | $ ? | $7,000 |

| Cost of Goods Sold | ? | 6,840 | 6,160 | ? |

| Gross Profit | 2,500 | ? | 1,840 | ? |

| Gross Profit Percentage | ? | ? | ? | 22% |

Required:

- Calculate the missing amounts for each year.

- What does this information indicate about the company?

EXERCISE 5–2 (LO2)

Reber Corp. uses the perpetual inventory system. Its transactions during July 2023 are as follows:

| July 6 | Purchased $600 of merchandise on account from Hobson Corporation for terms 1/10, net 30. |

| 9 | Returned $200 of defective merchandise. |

| 15 | Paid the amount owing to Hobson. |

Required: Prepare journal entries to record the above transactions for Reber Corp.

EXERCISE 5–3 (LO2,3,4)

Horne Inc. and Sperling Renovations Ltd. both sell goods and use the perpetual inventory system. Horne Inc. had $3,000 of merchandise inventory at the start of its fiscal year, January 1, 2023. During the 2023, Horne Inc. had the following transactions:

| May 5 | Horne sold $4,000 of merchandise on account to Sperling Renovations Ltd., terms 2/10, net 30. Cost of merchandise to Horne from its supplier was $2,500. |

| 7 | Sperling returned $500 of merchandise received in error which Horne returned to inventory; Horne issued a credit memo. Cost of merchandise to Horne was $300. |

| 15 | Horne received the amount due from Sperling Renovations Ltd. |

A physical count and valuation of Horne's Merchandise Inventory at May 31, the fiscal year-end, showed $700 of goods on hand.

Required: Prepare journal entries to record the above transactions and adjustment:

- In the records of Horne Inc.

- In the records of Sperling Renovations Ltd.

EXERCISE 5–4 (LO2,3) Recording Purchase and Sales Transactions

Below are transactions for March, 2023 for AngieJ Ltd.:

| March 1 | Purchased $25,000 of merchandise on account for terms 2/10, n30. |

| March 3 | Sold merchandise to a customer for $5,000 for terms 1/10, n30. (Cost $2,600) |

| March 4 | Customer from March 3 returned $200 of some unsuitable goods which were returned to inventory. (Cost $100) |

| March 5 | Purchased $15,000 of merchandise from a supplier for cash and arranged for shipping, fob shipping point. |

| March 6 | Paid $200 for shipping on the March 5 purchase. |

| March 7 | Contacted the supplier from March 5 regarding $2,000 of merchandise with some minor damages. Supplier agreed to reduce the price and offered an allowance of $500 cash, which was accepted. |

| March 8 | Sold $25,000 of merchandise for terms 1.5/10, n30. (Cost $13,000). Agreed to pay shipping costs for the goods sold to the customer. |

| March 9 | Shipped the goods sold on March 8 to customer, fob destination for $500 cash. (Hint: Shipping costs paid to ship merchandise sold to a customer is an operating expense.) |

| March 11 | Paid for fifty percent of the March 1 purchase to the supplier. |

| March 13 | Collected the account owing from the customer from March 3. |

| March 15 | Purchased office supplies on account for $540 for terms 1/10, n30. |

| March 18 | Ordered merchandise inventory from a supplier totalling $15,000. Goods to be shipped on April 10, fob shipping point. |

| March 20 | Collected $6,010 cash from an account owing from two months ago. The early payment discount had expired. |

| March 25 | Paid for the March 15 purchase. |

| March 27 | Sold $12,500 of merchandise inventory for cash (Cost $5,000). |

| March 31 | Paid the remaining of the amount owing from the March 1 purchase. |

Required: Prepare the journal entries, if any, for AngieJ Ltd.

EXERCISE 5–5 (LO2,3) Recording Purchase and Sales Transactions

Below are the April, 2023 sales for Beautort Corp.

| April 1 | Purchased $15,000 of merchandise for cash. |

| April 3 | Sold merchandise to a customer for $8,000 cash. (Cost $4,600) |

| April 5 | Purchased $10,000 of merchandise from a supplier for terms 1/10, n30. |

| April 7 | Returned $2,000 of damaged merchandise inventory from April 5 back to the supplier. Supplier will repair the items and return them to their own inventory. |

| April 8 | Sold $8,000 of merchandise for terms 2/10, n30. (Cost $4,000). Agreed to pay shipping costs for the goods sold to the customer. |

| April 9 | Shipped the goods sold on April 8 to customer, fob shipping point for $500 cash. (Hint: Shipping costs paid to ship merchandise sold to a customer is not an inventory cost.) |

| April 10 | Customer from April 3 returned $1,000 of unsuitable goods which were returned to inventory. (Cost $400). Amount paid was refunded. |

| April 10 | Agreed to give customer from April 8 sale a sales allowance of $200. |

| April 12 | Purchased inventory on account for $22,000 for terms 1/10, n30. |

| April 15 | Paid amount owing for purchases on April 5. |

| April 16 | Paid $600 for shipping on the April 12 purchase. |

| April 18 | Collected $5,000 cash, net of discount, for the customer account owing from April 8. |

| April 27 | Paid for the April 12 purchase. |

| April 27 | Sold $20,000 of merchandise inventory for cash (Cost $10,000). |

Required: Prepare the journal entries, if any, for Beautort Corp. Round final entry amounts to the nearest whole dollar.

EXERCISE 5–6 (LO5)

The following information is taken from the records of Smith Corp. for the year ended June 30, 2023:

| Advertising Expense | $ 1,500 |

| Commissions Expense | 4,000 |

| Cost of Goods Sold | 50,000 |

| Delivery Expense | 500 |

| Depreciation Expense – Equipment | 500 |

| Insurance Expense | 1,000 |

| Office Salaries Expense | 3,000 |

| Rent Expense – Office | 1,000 |

| Rent Expense – Store | 1,500 |

| Sales Salaries Expense | 2,000 |

| Sales | 72,000 |

| Sales Returns and Allowances | 2,000 |

Required:

- Prepare a classified multi-step income statement for the year ended June 30, 2023. Assume an income tax rate of 20%.

- Compute the gross profit percentage, rounding to two decimal places.

EXERCISE 5–7 (LO4) Calculating Inventory and Cost of Goods Sold

Below is a table that contains two important calculations that link together to determine net income/(loss):

| Inventory, opening balance | $ 10,000 | $ 53,000 | ? | 168,540 | 50,562 |

| Plus: purchases | 30,000 | ? | 1,685,400 | ? | ? |

| Total goods available for sale | ? | 212,000 | 2,247,200 | ? | 657,306 |

| Less: ending inventory | 15,000 | ? | 842,700 | 556,180 | 100,000 |

| Cost of goods sold | ? | 132,500 | ? | ? | ? |

| Sales | ? | 240,000 | 1,600,000 | 900,000 | ? |

| Less: cost of goods sold | ? | ? | ? | ? | ? |

| Gross profit | 30,000 | ? | ? | 276,400 | 142,694 |

| Less: operating expenses | 12,000 | ? | 275,000 | ? | ? |

| Net income/(loss) | ? | 43,900 | ? | 26,400 | (2,306) |

| Gross profit/sales (%) | ? | ? | ? | ? | ? |

Required: Calculate the missing account balances using the relationships between these accounts. Percentage can be rounded to the nearest two decimal places.

EXERCISE 5–8 (LO6)

Refer to the information in EXERCISE 5–6.

Required:

- Prepare all closing entries. Assume cash dividends totalling $2,000 were declared during the year and recorded as a debit to Dividends Declared and a credit to Cash.

- Calculate the June 30, 2023 post-closing balance in Retained Earnings assuming a beginning balance of $18,000.

EXERCISE 5–9 (LO7 Appendix)

Consider the information for each of the following four companies.

| A | B | C | D | |

| Opening Inventory | $ ? | $ 184 | $ 112 | $ 750 |

| Purchases | 1415 | ? | 840 | 5,860 |

| Transportation-In | 25 | 6 | 15 | ? |

| Cost of Goods Available for Sale | 1,940 | 534 | ? | 6,620 |

| Ending Inventory | 340 | 200 | 135 | ? |

| Cost of Goods Sold | ? | ? | ? | 5,740 |

Required: Calculate the missing amounts.

EXERCISE 5–10 (LO7 Appendix)

The following data pertain to Pauling Inc.

| Opening Inventory | $ 375 |

| Purchases | 2930 |

| Purchases Discounts | 5 |

| Purchases Returns and Allowances | 20 |

| Transportation-In | 105 |

Ending inventory amounts to $440.

Required: Calculate cost of goods sold.

EXERCISE 5–11 (LO7 Appendix)

The following information is taken from the records of four different companies in the same industry:

| A | B | C | D | |

|---|---|---|---|---|

| Sales | $300 | $150 | $ ? | $ 90 |

| Opening Inventory | ? | 40 | 40 | 12 |

| Purchases | 240 | ? | ? | 63 |

| Cost of Goods Available for Sale | 320 | ? | 190 | ? |

| Ending Inventory | ? | (60) | (60) | (15) |

| Cost of Goods Sold | ? | 100 | 130 | 60 |

| Gross Profit | $100 | $ ? | $ 65 | $ ? |

| Gross Profit percentage | ? | ? | ? | ? |

Required:

- Calculate the missing amounts.

- Which company seems to be performing best? Why?

Problems

PROBLEM 5–1 (LO1,2,3,4)

Salem Corp. was incorporated on July 2, 2023 to operate a merchandising business. It uses the perpetual inventory system. All its sales are on account with terms: 2/10, n30. Its transactions during July 2023 are as follows:

| July 2 | Issued share capital for $5,000 cash. |

| 2 | Purchased $3,500 merchandise on account from Blic Pens Ltd. for terms 2/10, n30. |

| 2 | Sold $2,000 of merchandise on account to Spellman Chair Rentals Inc. (Cost to Salem: $1,200). |

| 3 | Paid Sayer Holdings Corp. $500 for July rent. |

| 5 | Paid Easton Furniture Ltd. $1,000 for equipment. |

| 8 | Collected $200 for a cash sale made today to Ethan Matthews Furniture Ltd. (Cost: $120). |

| 8 | Purchased $2,000 merchandise on account from Shaw Distributors Inc. for terms 2/15, n30. |

| 9 | Received the amount due from Spellman Chair Rentals Inc. for the July 2 sale. |

| 10 | Paid Blic Pens Ltd. for the July 2 purchase. |

| 10 | Purchased $200 of merchandise on account from Peel Products Inc. for terms n30. |

| 15 | Sold $2,000 of merchandise on account to Eagle Products Corp. (Cost: $1,300). |

| 15 | Purchased $1,500 of merchandise on account from Bevan Door Inc. for terms 2/10, n30. |

| 15 | Received a memo from Shaw Distributors Inc. to reduce accounts payable by $100 for defective merchandise included in the July 8 purchase. |

| 16 | Eagle Products Corp. returned $200 of defective merchandise which was scrapped (Cost to Salem: $150). |

| 20 | Sold $3,500 of merchandise on account to Aspen Promotions Ltd. (Cost: $2,700). |

| 20 | Paid Shaw Distributors Inc. for half the purchase made July 8. |

| 24 | Received half the amount due from Eagle Products Corp. in partial payment for the July 15 sale. |

| 24 | Paid Bevan Doors Ltd. for the purchase made July 15. |

| 26 | Sold $600 merchandise on account to Longbeach Sales Ltd. (Cost: $400). |

| 26 | Purchased $800 of merchandise on account from Silverman Co. for terms 2/10, n30. |

| 31 | Paid Speedy Transport Co. $350 for transportation to Salem's warehouse during the month (all purchases are fob shipping point). |

Required:

- Prepare journal entries to record the July transactions. Include general ledger account numbers and a brief description.

- Calculate the unadjusted ending balance in merchandise inventory.

- Assume the merchandise inventory is counted at July 31 and assigned a total cost of $2,400. Prepare the July 31 adjusting entry.

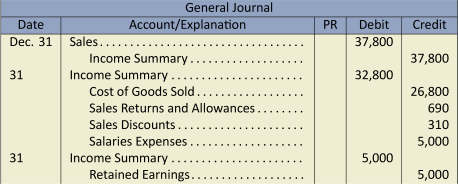

PROBLEM 5–2 (LO1,5,6)

The following closing entries were prepared for Whirlybird Products Inc. at December 31, 2023, the end of its fiscal year.

Required: Calculate gross profit.

PROBLEM 5–3 (LO1,5,6)

The following alphabetized adjusted trial balance has been extracted from the records of Acme Automotive Inc. at December 31, 2023, its third fiscal year-end. All accounts have a normal balance.

| Accounts Payable | 9,000 |

| Accounts Receivable | 15,000 |

| Accumulated Depreciation – Equipment | 36,000 |

| Advertising Expense | 14,000 |

| Bank Loan | 14,000 |

| Cash | 2,000 |

| Commissions Expense | 29,000 |

| Cost of Goods Sold | 126,000 |

| Delivery Expense | 14,800 |

| Depreciation Expense | 12,000 |

| Dividends | 11,000 |

| Equipment | 120,000 |

| Income Taxes Expense | 4,200 |

| Income Taxes Payable | 4,200 |

| Insurance Expense | 10,400 |

| Interest Expense | 840 |

| Merchandise Inventory | 26,000 |

| Office Supplies Expense | 3,100 |

| Rent Expense | 32,400 |

| Rent Revenue | 19,200 |

| Retained Earnings | 12,440 |

| Sales | 310,000 |

| Sales Discounts | 1,300 |

| Sales Returns and Allowances | 2,900 |

| Sales Salaries Expense | 26,400 |

| Share Capital | 70,000 |

| Supplies | 3,200 |

| Telephone Expense | 1,800 |

| Utilities Expense | 4,200 |

| Wages Expense – Office | 14,300 |

Required:

- Prepare a classified multi-step income statement and statement of changes in equity for the year ended December 31, 2023. Assume 40% of the Rent Expense is allocated to general and administrative expenses with the remainder allocated to selling expenses. Additionally, assume that $20,000 of shares were issued during the year ended December 31, 2023.

- Prepare closing entries.

PROBLEM 5–4 (LO1,2,3,4) Challenge Question – Pulling It All Together

Calculating Purchases, Inventory Shrinkage, Net Sales, Cost Goods Sold, Gross Profit, and Net Income/(Loss)

The information below is a summary of the merchandise inventory and sales transactions for 2016.

| Total cost of purchases | $250,000 |

| Total sales | 580,000 |

| Purchases shipping costs | 500 |

| Merchandise inventory, opening balance | 55,000 |

| Purchase discounts | 3,500 |

| Sales discounts | 200 |

| Total sales returns to inventory | 100 |

| Merchandise inventory, closing GL balance | 90,000 |

| Merchandise inventory, physical inventory count | 88,500 |

| Sales allowances | 600 |

| Operating expenses | 250,000 |

| Sales returns | 200 |

| Purchase returns and allowances | 200 |

| Net purchases | ? |

| Inventory shrinkage adjustment amount | ? |

| Cost of goods sold | ? |

| Net sales | ? |

| Gross profit | ? |

| Net income/(loss) | ? |

| Gross profit ratio | ? |

Required: Calculate and fill in the blanks. (Hint: Refer to the merchandising company illustration in Section 5.1 and the T-account summary illustrations for inventory and cost of goods sold at the end of Section 5.4.)

PROBLEM 5–5 (LO1,2,3,5,6) Preparing a Classified Multiple-step Income Statement and Closing Entries

Below is the adjusted trial balance presented in alphabetical order for Turret Retail Ltd., for 2023. Their year-end is December 31.

| Turret Retail Ltd. | ||

| Trial Balance | ||

| At December 31, 2023 | ||

| Accounts payable | $31,250 | |

| Accounts receivable | $140,000 | |

| Accrued salaries and benefits payable | 12,000 | |

| Accumulated depreciation, furniture | 4,300 | |

| Cash | 21,000 | |

| Cash dividends | 10,000 | |

| Cost of goods sold | 240,000 | |

| Bank loan payable (long-term) | 40,320 | |

| Depreciation expense | 3,200 | |

| Copyright | 20,000 | |

| Furniture | 20,000 | |

| Income tax expense | 2,028 | |

| Income taxes payable | 8,000 | |

| Insurance expense | 5,000 | |

| Interest expense | 200 | |

| Interest payable | 550 | |

| Land | 140,000 | |

| Merchandise inventory | 120,000 | |

| Prepaid insurance expense | 6,000 | |

| Rent expense | 30,240 | |

| Rental income | 6,000 | |

| Retained earnings | 307,748 | |

| Salaries expense | 57,000 | |

| Sales | 360,000 | |

| Sales discounts | 3,600 | |

| Sales returns and allowances | 9,600 | |

| Share capital | 20,000 | |

| Shop supplies expense | 2,400 | |

| Shop supplies expense | 1,000 | |

| Travel expense | 2,100 | |

| Unearned revenue | 50,500 | |

| Utilities expense | 7,300 | |

| 840,668 | 840,668 | |

Required:

- Prepare a classified multiple-step income statement in good form, reporting operating expenses by nature, for the year ended December 31, 2023.

- Prepare the closing entries for the year-ended December 31, 2023.

- Calculate the gross profit ratio to two decimal places and comment on what this ratio means.

PROBLEM 5–6 (LO1,2,3,4,5) Challenge Question – Preparing Adjusting Entries and a Classified Multiple-step Income Statement

Below are the unadjusted accounts balances for Yuba Yabi Enterprises Ltd., for the year ended March 31, 2023. All account balances are normal. Yuba Yabi's business involves selling frozen food to restaurants as well as providing consulting services to assist restaurant businesses with their daily operations.

| Yuba Yabi Enterprises Ltd. | |

| Unadjusted Trial Balance | |

| March 31, 2023 | |

| Accounts payable | 68,750 |

| Accounts receivable | 308,000 |

| Accrued salaries and benefits payable | 26,400 |

| Accumulated depreciation, furniture | 9,460 |

| Cash | 46,200 |

| Cash dividends | 22,000 |

| Cost of goods sold | 528,000 |

| Advertising expense | 9,900 |

| Bank loan payable (long-term) | 88,704 |

| Depreciation expense | 7,040 |

| Copyright | 44,000 |

| Franchise | 66,000 |

| Furniture | 44,000 |

| Income tax expense | - |

| Income taxes payable | 17,600 |

| Insurance expense | 11,000 |

| Interest expense | 440 |

| Interest payable | 1,210 |

| Land | 308,000 |

| Merchandise inventory | 264,000 |

| Prepaid insurance expense | 13,200 |

| Prepaid advertising expense | 8,800 |

| Rent expense | 66,528 |

| Rental income | 13,200 |

| Retained earnings | 265,364 |

| Salaries expense | 125,400 |

| Sales | 792,000 |

| Sales discounts | 7,920 |

| Sales returns and allowances | 21,120 |

| Service revenue | 495,000 |

| Share capital | 44,000 |

| Shop supplies | 8,360 |

| Shop supplies expense | 2,200 |

| Travel expense | 4,620 |

| Unearned service revenue | 111,100 |

| Utilities expense | 16,060 |

Additional information:

The following are adjusting entries that have not yet been recorded:

| Accrued salaries | $12,000 |

| Accrued interest on the bank loan | 5,600 |

| Inventory shrinkage | 7,800 |

| Prepaid insurance expense | 5,000 has expired |

| Prepaid advertising expense | no change |

| Unearned revenue | 30,000 has been earned |

| Income tax rate | 30% |

Required:

- Update the affected accounts by the adjustments, if any. Round all adjustments to the nearest whole dollar.

- Prepare a classified multiple-step income statement in good form for the year ended March 31, 2023.