5.1: The Basics of Merchandising

- Page ID

- 97794

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Use the following questions as a self-check while working through Chapter 5.

- What is gross profit and how is it calculated?

- How is a merchandiser different from a service company?

- What is a perpetual inventory system?

- How is the purchase of merchandise inventory on credit recorded in a perpetual system?

- How is a purchase return recorded in a perpetual system?

- What does the credit term of "1/15, n30" mean?

- How is a purchase discount recorded in a perpetual system?

- How is the sale of merchandise inventory on credit recorded in a perpetual system?

- How is a sales return that is restored to inventory recorded versus a sales return that is not restored to inventory (assuming a perpetual inventory system)?

- What is a sales discount and how is it recorded in a perpetual inventory system?

- Why does merchandise inventory need to be adjusted at the end of the accounting period and how is this done in a perpetual inventory system?

- What types of transactions affect merchandise inventory in a perpetual inventory system?

- How are the closing entries for a merchandiser using a perpetual inventory system different than for a service company?

- When reporting expenses on an income statement, how is the function of an expense reported versus the nature of an expense?

- On a classified multiple-step income statement, what is reported under the heading 'Other revenues and expenses' and why?

- What is the periodic inventory system?

- How is cost of goods sold calculated under the periodic inventory system?

NOTE: The purpose of these questions is to prepare you for the concepts introduced in the chapter. Your goal should be to answer each of these questions as you read through the chapter. If, when you complete the chapter, you are unable to answer one or more the Concept Self-Check questions, go back through the content to find the answer(s). Solutions are not provided to these questions.

5.1 The Basics of Merchandising

LO1 – Describe merchandising and explain the financial statement components of sales, cost of goods sold, merchandise inventory, and gross profit; differentiate between the perpetual and periodic inventory systems.

A merchandising company, or merchandiser, differs in several basic ways from a company that provides services. First, a merchandiser purchases and then sells goods whereas a service company sells services. For example, a car dealership is a merchandiser that sells cars while an airline is a service company that sells air travel. Because merchandising involves the purchase and then the resale of goods, an expense called cost of goods sold results. Cost of goods sold is the cost of the actual goods sold. For example, the cost of goods sold for a car dealership would be the cost of the cars purchased from manufacturers and then resold to customers. A service company does not have an expense called cost of goods sold since it does not sell goods. Because a merchandiser has cost of goods sold expense and a service business does not, the income statement for a merchandiser includes different details. A merchandising income statement highlights cost of goods sold by showing the difference between sales revenue and cost of goods sold called gross profit or gross margin. The basic income statement differences between a service business and a merchandiser are illustrated in Figure 5.1.

| Service Company | Merchandising Company |

| Revenues | Sales |

| Less: Cost of Goods Sold | |

| Equals: Gross Profit | |

| Less: Expenses | Less: Expenses |

| Equals: Net Income | Equals: Net Income |

Assume that Excel Cars Corporation decides to go into the business of buying used vehicles from a supplier and reselling these to customers. If Excel purchases a vehicle for $3,000 and then sells it for $4,000, the gross profit would be $1,000, as follows:

| Sales | $ 4,000 |

| Cost of Goods Sold | 3,000 |

| Gross Profit | $ 1,000 |

The word "gross" is used by accountants to indicate that other expenses incurred in running the business must still be deducted from this amount before net income is calculated. In other words, gross profit represents the amount of sales revenue that remains to pay expenses after the cost of the goods sold is deducted.

A gross profit percentage can be calculated to express the relationship of gross profit to sales. The sale of the vehicle that cost $3,000 results in a 25% gross profit percentage ($1,000/4,000). That is, for every $1 of sales, the company has $.25 left to cover other expenses after deducting cost of goods sold. Readers of financial statements use this percentage as a means to evaluate the performance of one company against other companies in the same industry, or in the same company from year to year. Small fluctuations in the gross profit percentage can have significant effects on the financial performance of a company because the amount of sales and cost of goods sold are often very large in comparison to other income statement items.

Another difference between a service company and a merchandiser relates to the balance sheet. A merchandiser purchases goods for resale. Goods held for resale by a merchandiser are called merchandise inventory and are reported as an asset on the balance sheet. A service company would not normally have merchandise inventory.

Inventory Systems

There are two types of ways in which inventory is managed: perpetual inventory system or periodic inventory system. In a perpetual inventory system, the merchandise inventory account and cost of goods sold account are updated immediately when transactions occur. In a perpetual system, as merchandise inventory is purchased, it is debited to the merchandise inventory account. As inventory is sold to customers, the cost of the inventory sold is removed from the merchandise inventory account and debited to the cost of goods sold account. A perpetual system means that account balances are known on a real-time basis. This chapter focuses on the perpetual system.

Some businesses still use a periodic inventory system in which the purchase of merchandise inventory is debited to a temporary account called Purchases. At the end of the accounting period, inventory is counted (known as a physical count) and the merchandise inventory account is updated and cost of goods sold is calculated. In a periodic inventory system, the real-time balances in merchandise inventory and cost of goods sold are not known. It should be noted that even in a perpetual system a physical count must be performed at the end of the accounting period to record differences between the actual inventory on hand and the account balance. The entry to record this difference is discussed later in this chapter. The periodic system is discussed in greater detail in the appendix to this chapter.

5.2 The Purchase and Payment of Merchandise Inventory (Perpetual)

LO2 – Analyze and record purchase transactions for a merchandiser.

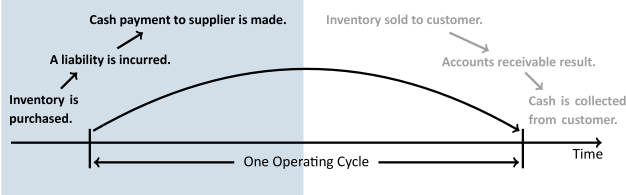

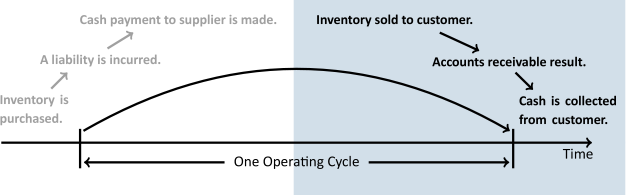

As introduced in Chapter 3, a company's operating cycle includes purchases on account or on credit and is highlighted in Figure 5.2.

Recording the Purchase of Merchandise Inventory (Perpetual)

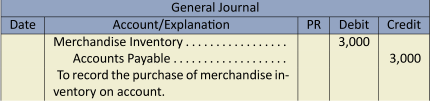

When merchandise inventory is purchased, the cost is recorded in a Merchandise Inventory general ledger account. An account payable results when the merchandise inventory is acquired but will not be paid in cash until a later date. For example, recall the vehicle purchased on account by Excel for $3,000. The journal entry and general ledger T-account effects would be as follows.

In addition to the purchase of merchandise inventory, there are other activities that affect the Merchandise Inventory account. For instance, merchandise may occasionally be returned to a supplier or damaged in transit, or discounts may be earned for prompt cash payment. These transactions result in the reduction of amounts due to the supplier and the costs of inventory. The purchase of merchandise inventory may also involve the payment of transportation and handling costs. These are all costs necessary to prepare inventory for sale, and all such costs are included in the Merchandise Inventory account. These costs are discussed in the following sections.

Purchase Returns and Allowances (Perpetual)

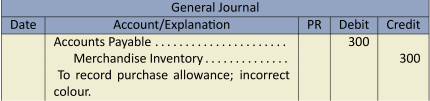

Assume that the vehicle purchased by Excel turned out to be the wrong colour. The supplier was contacted and agreed to reduce the price by $300 to $2,700. This is an example of a purchase returns and allowances adjustment. The amount of the allowance, or reduction, is recorded as a credit to the Merchandise Inventory account, as follows:

Note that the cost of the vehicle has been reduced to $2,700 ($3,000 – 300) as has the amount owing to the supplier. Again, the perpetual inventory system records changes in the Merchandise Inventory account each time a relevant transaction occurs.

Purchase Discounts (Perpetual)

Purchase discounts affect the purchase price of merchandise if payment is made within a time period specified in the supplier's invoice. For example, if the terms on the $3,000 invoice for one vehicle received by Excel indicates "1/15, n45", this means that the $3,000 must be paid within 45 days ('n' = net). However, if cash payment is made by Excel within 15 days, the purchase price will be reduced by 1%.

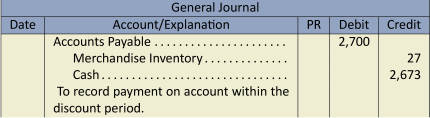

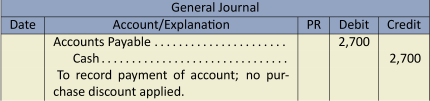

Assuming the amount is paid within 15 days, the supplier's terms entitle Excel to deduct $27 [($3,000 - $300) = $2,700 x 1% = $27]. The payment to the supplier would be recorded as:

The cost of the vehicle in Excel's inventory records is now $2,673 ($3,000 – 300 – 27). If payment is made after the discount period, $2,700 of cash is paid and the entry would be:

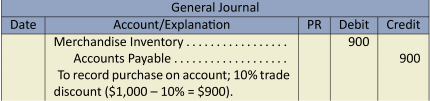

Trade discounts are similar to purchase discounts. A supplier advertises a list price which is the normal selling price of its goods to merchandisers. Trade discounts are given by suppliers to merchandisers that buy a large quantity of goods. For instance, assume a supplier offers a 10% trade discount on purchases of 1,000 units or more where the list price is $1/unit. If Beta Merchandiser Corp. buys 1,000 units on account, the entry in Beta's records would be:

Note that the net amount (list price less trade discount) is recorded.

Transportation

Costs to transport goods from the supplier to the seller must also be considered when recording the cost of merchandise inventory. The shipping terms on the invoice identify the point at which ownership of the inventory transfers from the supplier to the purchaser. When the terms are FOB shipping point, ownership transfers at the 'shipping point' so the purchaser is responsible for transportation costs. FOB destination indicates that ownership transfers at the 'destination point' so the seller is responsible for transportation costs. FOB is the abbreviation for "free on board."

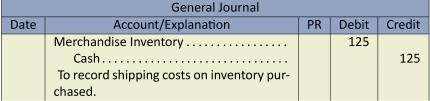

Assume that Excel's supplier sells with terms of FOB shipping point indicating that transportation costs are Excel's responsibility. If the cost of shipping is $125 and this amount was paid in cash to the truck driver at time of delivery, the entry would be:

The cost of the vehicle in the Excel Merchandise Inventory account is now $2,798 (calculated as $3,000 original cost - $300 allowance - $27 discount + $125 shipping). It is important to note that Excel's transportation costs to deliver goods to customers are recorded as delivery expenses and do not affect the Merchandise Inventory account.

The next section describes how the sale of merchandise is recorded as well as the related costs of items sold.

5.3 Merchandise Inventory: Sales and Collection (Perpetual)

LO3 – Analyze and record sales transactions for a merchandiser.

In addition to purchases on account, a merchandising company's operating cycle includes the sale of merchandise inventory on account or on credit as highlighted in Figure 5.3.

There are some slight recording differences when revenue is earned in a merchandising company. These are discussed below.

Recording the Sale of Merchandise Inventory (Perpetual)

The sale of merchandise inventory is recorded with two entries:

- recording the sale by debiting Cash or Accounts Receivable and crediting Sales, and

- recording the cost of the sale by debiting Cost of Goods Sold and crediting Merchandise Inventory.

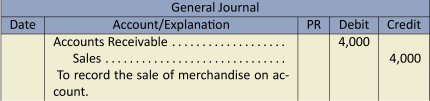

Assume the vehicle purchased by Excel is sold for $4,000 on account. Recall that the cost of this vehicle in the Excel Merchandise Inventory account is $2,798, as shown below.

The entries to record the sale of the merchandise inventory are:

The first entry records the sales revenue. The second entry is required to reduce the Merchandise Inventory account and transfer the cost of the inventory sold to the Cost of Goods Sold account. The second entry ensures that both the Merchandise Inventory account and Cost of Goods Sold account are up to date.

Sales Returns and Allowances

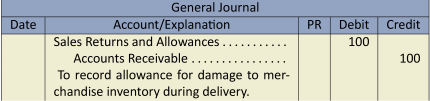

When merchandise inventory that has been sold is returned to the merchandiser by the customer, a sales return and allowance is recorded. For example, assume some damage occurs to the merchandise inventory sold by Excel while it is being delivered to the customer. Excel gives the customer a sales allowance by agreeing to reduce the amount owing by $100. The entry is:

Accounts receivable is credited because the original sale was made on account and has not yet been paid. The amount owing from the customer is reduced to $3,900. If the $3,900 had already been paid, a credit would be made to Cash and $100 refunded to the customer. The Sales Returns and Allowances account is a contra revenue account and is therefore deducted from Sales when preparing the income statement.

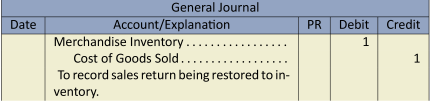

If goods are returned by a customer, a sales return occurs. The related sales and cost of goods sold recorded on the income statement are reversed and the goods are returned to inventory. For example, assume Max Corporation sells a plastic container for $3 that it purchased for $1. The dual entry at the time of sale would be:

If the customer returns the container and the merchandise is restored to inventory, the dual journal entry would be:

The use of a contra account to record sales returns and allowances permits management to track the amount of returned and damaged items.

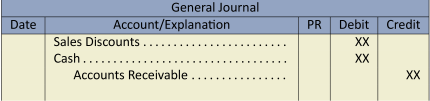

Sales Discounts

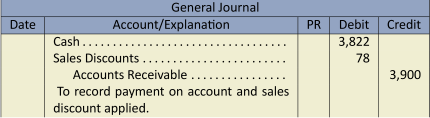

Another contra revenue account, Sales Discounts, records reductions in sales amounts when a customer pays within a certain time period. For example, assume Excel Cars Corporation offers sales terms of "2/10, n30." This means that the amount owed must be paid by the customer within 30 days ('n' = net); however, if the customer chooses to pay within 10 days, a 2% discount may be deducted from the amount owing.

Consider the sale of the vehicle for $3,900 ($4,000 less the $100 allowance for damage). Payment within 10 days entitles the customer to a $78 discount ($3,900 x 2% = $78). If payment is made within the discount period, Excel receives $3,822 cash ($3,900 - 78) and prepares the following entry:

This entry reduces the accounts receivable amount to zero which is the desired result. If payment is not made within the discount period, the customer pays the full amount owing of $3,900.

As was the case for Sales Returns and Allowances, the balance in the Sales Discounts account is deducted from Sales on the income statement to arrive at Net Sales. Merchandisers often report only the net sales amount on the income statement. Details from sales returns and allowances, and sales discounts, are often omitted because they are immaterial in amount relative to total sales. However, as already stated, separate general ledger accounts for each of sales returns and allowances, and sales discounts, are useful in helping management identify potential problems that require investigation.

5.4 Adjustments to Merchandise Inventory (Perpetual)

LO4 – Record adjustments to merchandise inventory.

To verify that the actual amount of merchandise inventory on hand is consistent with the balance recorded in the accounting records, a physical inventory count must be performed at the end of the accounting period. When a physical count of inventory is conducted, the costs attached to these inventory items are totalled. This total is compared to the Merchandise Inventory account balance in the general ledger. Any discrepancy is called shrinkage. Theft and deterioration of merchandise inventory are the most common causes of shrinkage.

The adjusting entry to record shrinkage is:

Summary of Merchandising Transactions

As the preceding sections have illustrated, there are a number of entries which are unique to a merchandiser. These are summarized below (assume all transactions were on account):

(a) To record the purchase of merchandise inventory from a supplier:

(b) To record purchase return and allowances:

(c) To record purchase discounts:

(d) To record shipping costs from supplier to merchandiser:

(e) To record sale of merchandise inventory and cost of the sale:

AND

(f) To record sales returns restored to inventory:

AND

(g) To record sales returns and allowances (where returns are not restored to inventory):

(h) To record discounts:

(i) To record adjustment for shrinkage at the end of the accounting period:

The effect of these transactions on each of merchandise inventory and cost of goods sold is depicted below:

| Merchandise Inventory (MI) | Cost of Goods Sold (COGS) | ||

| (a) Purchase of MI | (b) Purchase Ret. & Allow. | (e) Cost of MI Sold | (f) Cost of sales returns restored to inventory |

| (d) Shipping Costs | (c) Purchase Discounts | (i) Shrinkage Adjustment | |

| (f) Sales Return (when restored to inventory) | (e) Sale of MI | ||

| (i) Shrinkage Adjustment | |||

| Adjusted Balance Reported on the Balance Sheet | Adjusted Balance Reported on the Income Statement | ||

5.5 Merchandising Income Statement

LO5 – Explain and prepare a classified multiple-step income statement for a merchandiser.

Businesses are required to show expenses on the income statement based on either the nature or the function of the expense. The nature of an expense is determined by its basic characteristics (what it is). For example, when expenses are listed on the income statement as interest, depreciation, income tax, or wages, this identifies the nature of each expense. In contrast, the function of an expense describes the grouping of expenses based on their purpose (what they relate to). For example, an income statement that shows cost of goods sold, selling expenses, and general and administrative expenses has grouped expenses by their function. When expenses are grouped by function, additional information must be disclosed to show the nature of expenses within each group. The full disclosure principle is the generally accepted accounting principle that requires financial statements to report all relevant information about the operations and financial position of the entity. Information that is relevant but not included in the body of the statements is provided in the notes to the financial statements.

A merchandising income statement can be prepared in different formats. For this course, only one format will be introduced — the classified multiple-step format. This format is generally used for internal reporting because of the detail it includes. An example of a classified multiple-step income statement is shown below using assumed data for XYZ Inc. for its month ended December 31, 2023.

| XYZ Inc. | ||||

| Income Statement | ||||

| Month Ended December 31, 2023 | ||||

| Sales | $100,000 | |||

|

Less: Sales discounts |

$1,000 | |||

|

Sales returns and allowances |

500 | 1,500 | ||

|

Net sales |

$98,500 | |||

| Cost of goods sold | 50,000 | |||

| Gross profit from sales | $48,500 | |||

| Operating expenses: | ||||

|

Selling expenses: |

||||

|

Sales salaries expense |

$11,000 | |||

|

Rent expense, selling space |

9,000 | |||

|

Advertising expense |

5,000 | |||

|

Depreciation expense, store equipment |

3,000 | |||

|

Total selling expenses |

$28,000 | |||

|

General and administrative expenses: |

||||

|

Office salaries expense |

$9,000 | |||

|

Rent expense, office space |

3,000 | |||

|

Office supplies expense |

1,500 | |||

|

Depreciation expense, office equipment |

1,000 | |||

|

Insurance expense |

1,000 | |||

|

Total general and administrative expenses |

15,500 | |||

|

Total operating expenses |

43,500 | |||

| Income from operations | $5,000 | |||

|

Other revenues and expenses: |

||||

|

Rent revenue |

$12,000 | |||

|

Interest expense |

1,500 | 10,500 | ||

| Income before tax | $15,500 | |||

| Income tax expense | 3,000 | |||

| Net income | $12,500 | |||

Notice that the classified multiple-step income statement shows expenses by both function and nature. The broad categories that show expenses by function include operating expenses, selling expenses, and general and administrative expenses. Within each category, the nature of expenses is disclosed including sales salaries, advertising, depreciation, supplies, and insurance. Notice that Rent Expense has been divided between two groupings because it applies to more than one category or function.

The normal operating activity for XYZ Inc. is merchandising. Revenues and expenses that are not part of normal operating activities are listed under Other Revenues and Expenses. XYZ Inc. shows Rent Revenue under Other Revenues and Expenses because this type of revenue is not part of its merchandising operations. Interest earned, dividends earned, and gains on the sale of property, plant, and equipment are other examples of revenues not related to merchandising operations. XYZ Inc. deducts Interest Expense under Other Revenues and Expenses. Interest expense does not result from operating activities; it is a financing activity because it is associated with the borrowing of money. Another example of a non-operating expense is losses on the sale of property, plant, and equipment. Income tax expense is a government requirement so it is shown separately. Notice that income tax expense follows the subtotal 'Income before tax'.

5.6 Closing Entries for a Merchandiser

LO6 – Explain the closing process for a merchandiser.

The process of recording closing entries for service companies was illustrated in Chapter 3. The closing procedure for merchandising companies is the same as for service companies — all income statement accounts are transferred to the Income Summary account, the Income Summary is closed to Retained Earnings, and Dividends are closed to Retained Earnings.

When preparing closing entries for a merchandiser, the income statement accounts unique for merchandisers need to be considered — Sales, Sales Discounts, Sales Returns and Allowances, and Cost of Goods Sold. Sales is a revenue account so has a normal credit balance. To close Sales, it must be debited with a corresponding credit to the income summary. Sales Discounts and Sales Returns and Allowances are both contra revenue accounts so each has a normal debit balance. Cost of Goods Sold has a normal debit balance because it is an expense. To close these debit balance accounts, a credit is required with a corresponding debit to the income summary.

5.7 Appendix A: The Periodic Inventory System

LO7 – Explain and identify the entries regarding purchase and sales transactions in a periodic inventory system.

The perpetual inventory system maintains a continuous, real-time balance in both Merchandise Inventory, a balance sheet account, and Cost of Goods Sold, an income statement account. As a result, the Merchandise inventory general ledger account balance should always equal the value of physical inventory on hand at any point in time. Additionally, the Cost of Goods Sold general ledger account balance should always equal the total cost of merchandise inventory sold for the accounting period. The accounts should perpetually agree; hence the name. An alternate system is considered below, called the periodic inventory system.

Description of the Periodic Inventory System

The periodic inventory system does not maintain a constantly-updated merchandise inventory balance. Instead, ending inventory is determined by a physical count and valued at the end of an accounting period. The change in inventory is recorded only periodically. Additionally, a Cost of Goods Sold account is not maintained in a periodic system. Instead, cost of goods sold is calculated at the end of the accounting period.

When goods are purchased using the periodic inventory system, the cost of merchandise is recorded in a Purchases account in the general ledger, rather than in the Merchandise Inventory account as is done under the perpetual inventory system. The Purchases account is an income statement account that accumulates the cost of merchandise acquired for resale.

The journal entry, assuming a purchase of merchandise on credit, is:

Purchase Returns and Allowances (Periodic)

Under the periodic inventory system, any purchase returns or purchase allowances are accumulated in a separate account called Purchase Returns and Allowances, an income statement account, and recorded as:

Purchase Returns and Allowances is a contra expense account and the balance is deducted from Purchases when calculating cost of goods sold on the income statement.

Purchase Discounts (Periodic)

Another contra expense account, Purchase Discounts, accumulates reductions in the purchase price of merchandise if payment is made within a time period specified in the supplier's invoice and recorded as:

Transportation (Periodic)

Under the periodic inventory system, an income statement account called Transportation-in is used to accumulate transportation or freight charges on merchandise purchased for resale. The Transportation-in account is used in calculating the cost of goods sold on the income statement. It is recorded as:

At the end of the accounting period, cost of goods sold must be calculated which requires that the balance in Merchandise Inventory be determined. To determine the end of the period balance in Merchandise Inventory, a physical count of inventory is performed. The total value of the inventory as identified by the physical count becomes the ending balance in Merchandise Inventory. Cost of goods sold can then be calculated as follows:

| Beginning Balance of Merchandise Inventory | XX |

| Plus: Net Cost of Goods Purchased* | XX |

| Less: Ending Balance of Merchandise Inventory | XX |

| Equals: Cost of Goods Sold | XX |

| *Net Cost of Goods Purchased is calculated as: | |

|

|

XX |

|

|

XX |

|

|

XX |

|

|

XX |

|

|

XX |

|

|

XX |

Closing Entries (Periodic)

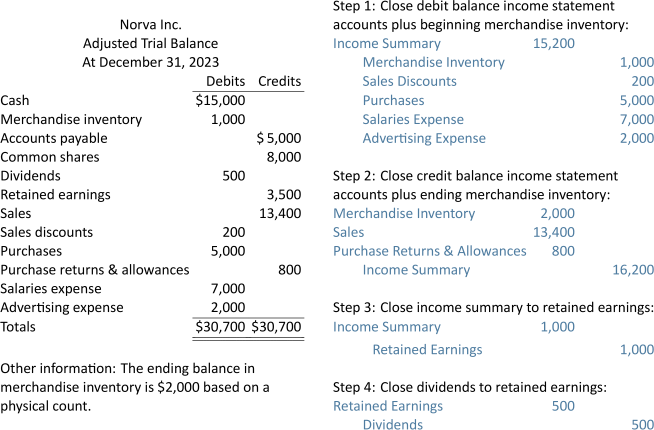

In the perpetual inventory system, the Merchandise Inventory account is continuously updated and is adjusted at the end of the accounting period based on a physical inventory count. In the periodic inventory system, the balance in Merchandise Inventory does not change during the accounting period. As a result, at the end of the accounting period, the balance in Merchandise Inventory in a periodic system is the beginning balance. In order for the Merchandise Inventory account to reflect the ending balance as determined by the physical inventory count, the beginning inventory balance must be removed by crediting Merchandise Inventory, and the ending inventory balance entered by debiting it. This is accomplished as part of the closing process. Closing entries for a merchandiser that uses a periodic inventory system are illustrated below using the adjusted trial balance information for Norva Inc.

When the closing entries above are posted and a post-closing trial balance prepared as shown below, notice that the Merchandise Inventory account reflects the correct balance based on the physical inventory count.

| Norva Inc. | ||

| Adjusted Trial Balance | ||

| At December 31, 2023 | ||

| Debits | Credits | |

| Cash | $15,000 | |

| Merchandise inventory | 2,000 | |

| Accounts payable | $ 5,000 | |

| Common shares | 8,000 | |

| Retained earnings | 4,000 | |

| Totals | $17,000 | $17,000 |

Summary of Chapter 5 Learning Objectives

LO1 – Describe merchandising and explain the financial statement components of sales, cost of goods sold, merchandise inventory, and gross profit; differentiate between the perpetual and periodic inventory systems.

Merchandisers buy and resell products. Merchandise inventory, an asset, is purchased from suppliers and resold to customers to generate sales revenue. The cost of the merchandise inventory sold is an expense called cost of goods sold. The profit realized on the sale of merchandise inventory before considering any other expenses is called gross profit. Gross profit may be expressed as a dollar amount or as a percentage. To track merchandise inventory and cost of goods sold in real time, a perpetual inventory system is used; the balance in each of Merchandise Inventory and Cost of Goods Sold is always up-to-date. In a periodic inventory system, a physical count of the inventory must be performed in order to determine the balance in Merchandise Inventory and Cost of Goods Sold.

LO2 – Analyze and record purchase transactions for a merchandiser.

In a perpetual inventory system, a merchandiser debits Merchandise Inventory regarding the purchase of merchandise for resale from a supplier. Any purchase returns and allowances or purchase discounts are credited to Merchandise Inventory as they occur to keep the accounts up-to-date.

LO3 – Analyze and record sales transactions for a merchandiser.

In a perpetual inventory system, a merchandiser records two entries at the time of sale: one to record the sale and a second to record the cost of the sale. Sales returns that are returned to inventory also require two entries: one to reverse the sale by debiting a sales returns and allowances account and a second to restore the merchandise to inventory by debiting Merchandise Inventory and crediting Cost of Goods Sold. Sales returns not restored to inventory as well as sales allowances are recorded with one entry: debit sales returns and allowances and credit cash or accounts receivable. Sales discounts are recorded when a credit customer submits their payment within the discount period specified.

LO4 – Record adjustments to merchandise inventory.

A physical count of merchandise inventory is performed and the total compared to the general ledger balance of Merchandise Inventory. Discrepancies are recorded as an adjusting entry that debits cost of goods sold and credits Merchandise Inventory.

LO5 – Explain and prepare a classified multiple-step income statement for a merchandiser.

A classified multiple-step income statement for a merchandiser is for internal use because of the detail provided. Sales, less sales returns and allowances and sales discounts, results in net sales. Net sales less cost of goods sold equals gross profit. Expenses are shown based on both their function and nature. The functional or group headings are: operating expenses, selling expenses, and general and administrative expenses. Within each grouping, the nature of expenses is detailed including: depreciation, salaries, advertising, wages, and insurance. A specific expense can be divided between groupings.

LO6 – Explain the closing process for a merchandiser.

The steps in preparing closing entries for a merchandiser are the same as for a service company. The difference is that a merchandiser will need to close income statement accounts unique to merchandising such as: Sales, Sales Returns and Allowances, Sales Discounts, and Cost of Goods Sold.

LO7 – Explain and identify the entries regarding purchase and sales transactions in a periodic inventory system.

A periodic inventory system maintains a Merchandise Inventory account but does not have a Cost of Goods Sold account. The Merchandise Inventory account is updated at the end of the accounting period as a result of a physical inventory count. Because a merchandiser using a period system does not use a Merchandise Inventory account to record purchase or sales transactions during the accounting period, it maintains accounts that are different than under a perpetual system, namely, Purchases, Purchase Returns and Allowances, Purchase Discounts, and Transportation-in.

- How does the income statement prepared for a company that sells goods differ from that prepared for a service business?

- How is gross profit calculated? What relationships do the gross profit and gross profit percentage calculations express? Explain, using an example.

- What are some common types of transactions that are recorded in the merchandise Inventory account?

- Contrast and explain the sales and collection cycle and the purchase and payment cycle.

- What contra accounts are used in conjunction with sales? What are their functions?

- (Appendix) Compare the perpetual and periodic inventory systems. What are some advantages of each?