4.1: Financial Statement Disclosure Decisions

- Page ID

- 97793

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Use the following as a self-check while working through Chapter 4.

- What shapes and limits an accountant's measurement of wealth?

- Are financial statements primarily intended for internal or external users?

- What is a classified balance sheet?

- What are the classifications within a classified balance sheet?

- What are current assets?

- What are non-current assets?

- What are current liabilities?

- What are long-term liabilities?

- What is the current-portion of a long-term liability?

- What is the purpose and content of the notes to the financial statements?

- What is the purpose and content of the auditor's report?

- What is the purpose and content of the report that describes management's responsibility for financial statements?

NOTE: The purpose of these questions is to prepare you for the concepts introduced in the chapter. Your goal should be to answer each of these questions as you read through the chapter. If, when you complete the chapter, you are unable to answer one or more the Concept Self-Check questions, go back through the content to find the answer(s). Solutions are not provided to these questions.

4.1 Financial Statement Disclosure Decisions

LO1 – Explain the importance of and challenges related to basic financial statement disclosure.

Financial statements communicate information, with a focus on the needs of financial statement users such as a company's investors and creditors. Accounting information should make it easier for management to allocate resources and for shareholders to evaluate management. A key objective of financial statements is to fairly present the entity's economic resources, obligations, equity, and financial performance.

Fulfilling these objectives is challenging. Accountants must make a number of subjective decisions about how to apply generally accepted accounting principles. For example, they must decide how to measure wealth and how to apply recognition criteria. They must also make practical cost-benefit decisions about how much information is useful to disclose. Some of these decisions are discussed in the following section.

Making Accounting Measurements

Economists often define wealth as an increase or decrease in the entity's ability to purchase goods and services. Accountants use a more specific measurement — they consider only increases and decreases resulting from actual transactions. If a transaction has not taken place, they do not record a change in wealth.

The accountant's measurement of wealth is shaped and limited by the generally accepted accounting principles introduced and discussed in Chapter 1, including cost, the monetary unit, the business entity, timeliness, recognition, and going concern. These principles mean that accountants record transactions in one currency (for example, dollars). They assume the monetary currency retains its purchasing power. Changes in market values of assets are generally not recorded. The entity is expected to continue operating into the foreseeable future.

Economists, on the other hand, do recognize changes in market value. For example, if an entity purchased land for $100,000 that subsequently increased in value to $125,000, economists would recognize a $25,000 increase in wealth. International Financial Reporting Standards generally do not recognize this increase until the entity actually disposes of the asset; accountants would continue to value the land at its $100,000 purchase cost. This practice is based on the application of the cost principle, which is a part of GAAP.

Economic wealth is also affected by changes in the purchasing power of the dollar. For example, if the entity has cash of $50,000 at the beginning of a time period and purchasing power drops by 10% because of inflation, the entity has lost wealth because the $50,000 can purchase only $45,000 of goods and services. Conversely, the entity gains wealth if purchasing power increases by 10%. In this case, the same $50,000 can purchase $55,000 worth of goods and services. However, accountants do not record any changes because the monetary unit principle assumes that the currency unit is a stable measure.

Qualities of Accounting Information

Financial statements are focused primarily on the needs of external users. To provide information to these users, accountants make cost-benefit judgments. They use materiality considerations to decide how particular items of information should be recorded and disclosed. For example, if the costs associated with financial information preparation are too high or if an amount is not sufficiently large or important, a business might implement a materiality policy for various types of asset purchases to guide how such costs are to be recorded. For example, a business might have a materiality policy for the purchase of office equipment whereby anything costing $100 or less is expensed immediately instead of recorded as an asset. In this type of situation, purchases of $100 or less are recorded as an expense instead of an asset to avoid having to record depreciation expense, a cost-benefit consideration that will not impact decisions made by external users of the business's financial statements.

Accountants must also make decisions based on whether information is useful. Is it comparable to prior periods? Is it verifiable? Is it presented with clarity and conciseness to make it understandable? Readers' perception of the usefulness of accounting information is determined by how well those who prepare financial statements address these qualitative considerations.

4.2 Classified Balance Sheet

LO2 – Explain and prepare a classified balance sheet.

The accounting cycle and double-entry accounting have been the focus of the preceding chapters. This chapter focuses on the presentation of financial statements, including how financial information is classified (the way accounts are grouped) and what is disclosed.

A common order for the presentation of financial statements is:

- Income statement

- Statement of changes in equity

- Balance sheet

- Statement of cash flows

- Notes to the financial statements

In addition, the financial statements are often accompanied by an auditor's report and a statement entitled "Management's Responsibility for Financial Statements." Each of these items will be discussed below. Financial statement information must be disclosed for the most recent year with the prior year for comparison.

Because external users of financial statements have no access to the entity's accounting records, it is important that financial statements be organized in a manner that is easy to understand. Thus, financial data are grouped into useful, similar categories within classified financial statements, as discussed below.

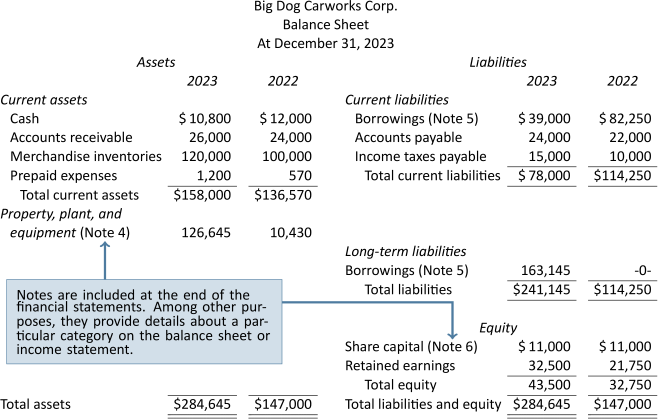

The Classified Balance Sheet

A classified balance sheet organizes the asset and liability accounts into categories. The previous chapters used an unclassified balance sheet which included only three broad account groupings: assets, liabilities, and equity. The classification of asset and liability accounts into meaningful categories is designed to facilitate the analysis of balance sheet information by external users. Assets and liabilities are classified as either current or non-current. Another common term for non-current is long-term. Non-current assets, also referred to as long-term assets, can be classified further into long-term investments; property, plant and equipment; and intangible assets. The asset and liability classifications are summarized below:

| Assets | Liabilities |

|---|---|

|

Non-current or long-term assets:

|

Non-current or long-term liabilities |

Current Assets

Current assets are those resources that the entity expects to convert to cash, or to consume during the next year or within the operating cycle of the entity, whichever is longer. Examples of current assets include:

- cash, comprising paper currency and coins, deposits at banks, cheques, and money orders.

- short-term investments, the investment of cash that will not be needed immediately, in short-term, interest-bearing notes that are easily convertible into cash.

- accounts receivable that are due to be collected within one year.

- notes receivable, usually formalized account receivables — written promises to pay specified amounts with interest, and due to be collected within one year.

- merchandise inventory that is expected to be sold within one year.

The current asset category also includes accounts whose future benefits are expected to expire in a short period of time. These are not expected to be converted into cash, and include:

- prepaid expenses that will expire within the next year, usually consisting of advance payments for insurance, rent, and other similar items.

- supplies on hand at the end of an accounting year that will be used during the next year.

On the balance sheet, current assets are normally reported before non-current assets. They are listed by decreasing levels of liquidity — their ability to be converted into cash. Therefore, cash appears first under the current asset heading since it is already liquid.

Non-current Assets

Non-current assets are assets that will be useful for more than one year; they are sometimes referred to as long-lived assets. Non-current assets include property, plant, and equipment (PPE) items used in the operations of the business. Some examples of PPE are: a) land, b) buildings, c) equipment, and d) motor vehicles such as trucks.

Other types of non-current assets include long-term investments and intangible assets. Long-term investments are held for more than one year or the operating cycle and include long-term notes receivable and investments in shares and bonds. Intangible assets are resources that do not have a physical form and whose value comes from the rights held by the owner. They are used over the long term to produce or sell products and services and include copyrights, patents, trademarks, and franchises.

Current Liabilities

Current liabilities are obligations that must be paid within the next 12 months or within the entity's next operating cycle, whichever is longer. They are shown first in the liabilities section of the balance sheet and listed in order of their due dates, with any bank loans shown first. Examples of current liabilities include:

- bank loans (or notes payable) that are payable on demand or due within the next 12 months

- accounts payable

- accrued liabilities such as interest payable and wages payable

- unearned revenue

- the current portion of long-term liabilities

- income taxes payable.

The current portion of a long-term liability is the principal amount of a long-term liability that is to be paid within the next 12 months. For example, assume a $24,000 note payable issued on January 1, 2023 where principal is repaid at the rate of $1,000 per month over two years. The current portion of this note on the January 31, 2023 balance sheet would be $12,000 (calculated as 12 months X $1,000/month). The remaining principal would be reported on the balance sheet as a long-term liability.

Non-Current or Long-Term Liabilities

Non-current liabilities, also referred to as long-term liabilities, are borrowings that do not require repayment for more than one year, such as the long-term portion of a bank loan or a mortgage. A mortgage is a liability that is secured by real estate.

Equity

The equity section of the classified balance sheet consists of two major accounts: share capital and retained earnings.

The following illustrates the presentation of Big Dog Carworks Corp.'s classified balance sheet after several years of operation.

The balance sheet can be presented in the account form balance sheet, as shown above where liabilities and equities are presented to the right of the assets. An alternative is the report form balance sheet where liabilities and equity are presented below the assets.

The Classified Income Statement

Recall that the income statement summarizes a company's revenues less expenses over a period of time. An income statement for BDCC was presented in Chapter 1 as copied below.

| Big Dog Carworks Corp. | ||

| Income Statement | ||

| For the Month Ended January 31, 2023 | ||

| Revenues | ||

|

Repair revenues |

$10,000 | |

| Expenses | ||

|

Rent expense |

$1,600 | |

|

Salaries expense |

3,500 | |

|

Supplies expense |

2,000 | |

|

Fuel expense |

700 | |

| Total expenses | 7,800 | |

| Net income | $2,200 | |

The format used above was sufficient to disclose relevant financial information for Big Dog's simple start-up operations. Like the classified balance sheet, an income statement can be classified as well as prepared with comparative information. The classified income statement will be discussed in detail in Chapter 5.

Regardless of the type of financial statement, any items that are material must be disclosed separately so users will not otherwise be misled. Materiality is a matter for judgment. Office supplies of $2,000 per month used by BDCC in January 2023 might be a material amount and therefore disclosed as a separate item on the income statement for the month ended January 31, 2023. If annual revenues grew to $1 million, $2,000 per month for supplies might be considered immaterial. These expenditures would then be grouped with other similar items and disclosed as a single amount.

4.3 Notes to Financial Statements

LO3 – Explain the purpose and content of notes to financial statements.

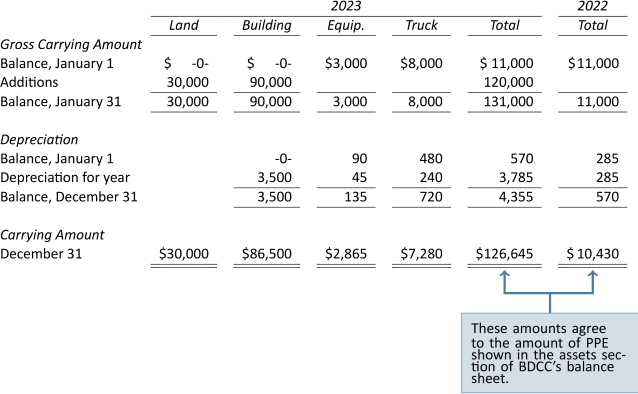

As an integral part of its financial statements, a company provides notes to the financial statements. In accordance with the disclosure principle, notes to the financial statements provide relevant details that are not included in the body of the financial statements. For instance, details about property, plant, and equipment are shown in Note 4 in the following sample notes to the financial statements. The notes help external users understand and analyze the financial statements.

Although a detailed discussion of disclosures that might be included as part of the notes is beyond the scope of an introductory financial accounting course, a simplified example of note disclosure is shown below for Big Dog Carworks Corp.

Big Dog Carworks Corp.

Notes to the Financial Statements

For the Year Ended December 31, 2023

-

Nature of operations

The principal activity of Big Dog Carworks Corp. is the servicing and repair of vehicles. -

General information and statement of compliance with IFRS

Big Dog Carworks Corp. is a limited liability company incorporated and domiciled in Canada. Its registered office and principal place of business is 123 Fox Street, Owlseye, Alberta, T1K 0L1, Canada. Big Dog Carworks Corp.'s shares are listed on the Toronto Stock Exchange.The financial statements of Big Dog Carworks Inc. have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued the International Accounting Standards Boards (IASB).

The financial statements for the year ended December 31, 2023 were approved and authorised for issue by the board of directors on March 17, 2024.

-

Summary of accounting policies

The financial statements have been prepared using the significant accounting policies and measurement bases summarized below.- Revenue

Revenue arises from the rendering of service. It is measured by reference to the fair value of consideration received or receivable.

- Operating expenses

Operating expenses are recognized in the income statement upon utilization of the service or at the date of their origin.

- Borrowing costs

Borrowing costs directly attributable to the acquisition, construction, or production of property, plant, and equipment are capitalized during the period of time that is necessary to complete and prepare the asset for its intended use or sale. Other borrowing costs are expensed in the period in which they are incurred and reported as interest expense.

- Property, plant, and equipment

Land held for use in production or administration is stated at cost. Other property, plant, and equipment are initially recognized at acquisition cost plus any costs directly attributable to bringing the assets to the locations and conditions necessary to be employed in operations. They are subsequently measured using the cost model: cost less subsequent depreciation.

Depreciation is recognized on a straight-line basis to write down the cost, net of estimated residual value. The following useful lives are applied:

- Buildings: 25 years

- Equipment: 10 years

- Truck: 5 years

Residual value estimates and estimates of useful life are updated at least annually.

- Income taxes

Current income tax liabilities comprise those obligations to fiscal authorities relating to the current or prior reporting periods that are unpaid at the reporting date. Calculation of current taxes is based on tax rates and tax laws that have been enacted or substantively enacted by the end of the reporting period.

- Share capital

Share capital represents the nominal value of shares that have been issued.

- Estimation uncertainty

When preparing the financial statements, management undertakes a number of judgments, estimates, and assumptions about the recognition and measurement of assets, liabilities, income, and expenses. Information about estimates and assumptions that have the most significant effect on recognition and measurement of assets, liabilities, income, and expenses is provided below. Actual results may be substantially different.

- Revenue

- Property, plant, and equipment

Details of the company's property, plant, and equipment and their carrying amounts at December 31 are as follows:

- Borrowings

Borrowings include the following financial liabilities measured at cost:

Current Non-Current 2023 2022 2023 2022 Demand bank loan $ 20,000 $ 52,250 $ -0- $ -0- Subordinated shareholder loan 13,762 30,000 -0- -0- Mortgage 5,238 -0- 163,145 -0- Total carrying amount $39,000 $82,250 $163,145 $ -0- The bank loan is due on demand and bears interest at 6% per year. It is secured by accounts receivable and inventories of the company.

The shareholder loan is due on demand, non-interest bearing, and unsecured.

The mortgage is payable to First Bank of Capitalville. It bears interest at 5% per year and is amortized over 25 years. Monthly payments including interest are $960. It is secured by land and buildings owned by the company. The terms of the mortgage will be re-negotiated in 2026.

- Share capital

The share capital of Big Dog Carworks Corp. consists of fully-paid common shares with a stated value of $1 each. All shares are eligible to receive dividends, have their capital repaid, and represent one vote at the annual shareholders' meeting. There were no shares issued during 2022 or 2023.

4.4 Auditor's Report

LO4 – Explain the purpose and content of the auditor's report.

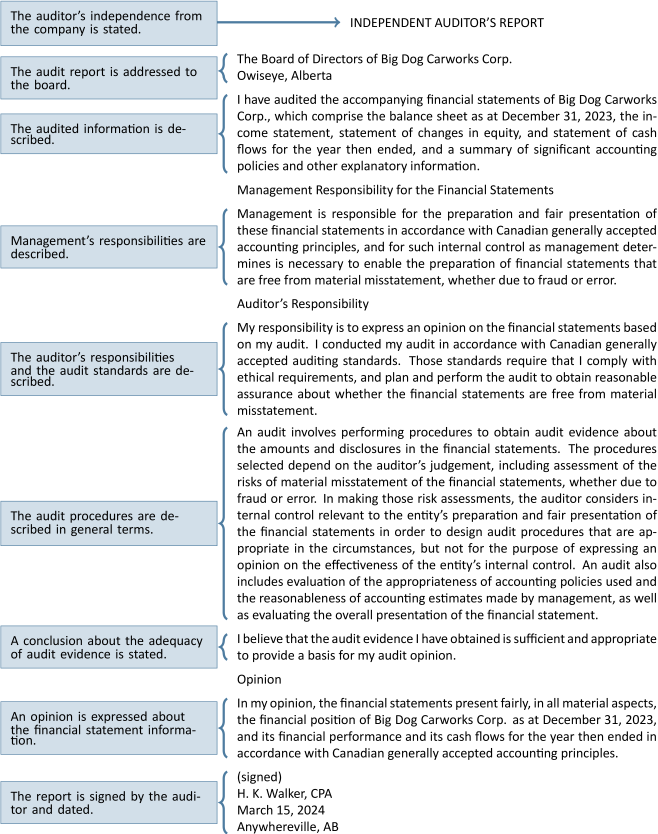

Financial statements are often accompanied by an auditor's report. An audit is an external examination of a company's financial statement information and its system of internal controls.

Internal controls are the processes instituted by management of a company to direct, monitor, and measure the accomplishment of its objectives. This includes the prevention and detection of fraud and error. An audit seeks not certainty, but reasonable assurance that the financial statement information is not materially misstated.

The auditor's report is a structured statement issued by an independent examiner, usually a professional accountant, who is contracted by the company to report the audit's findings to the company's board of directors. An audit report provides some assurance to present and potential investors and creditors that the company's financial statements are trustworthy. Therefore, it is a useful means to reduce the risk of their financial decisions.

An example of an unqualified auditor's report for BDCC is shown below, along with a brief description of each component. Put in simple terms, an unqualified auditor's report indicates that the financial statements are truthful and a qualified auditor's report is one that indicates the financial statements are not or may not be truthful.

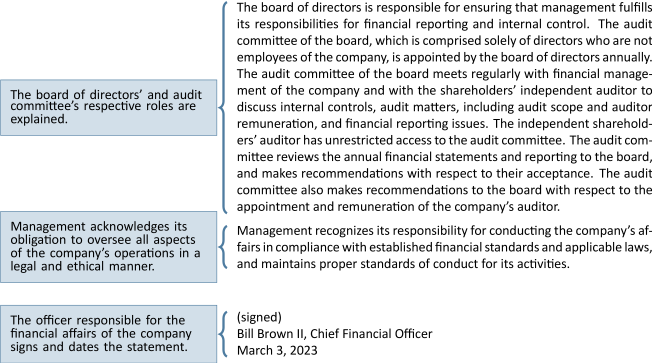

4.5 Management's Responsibility for Financial Statements

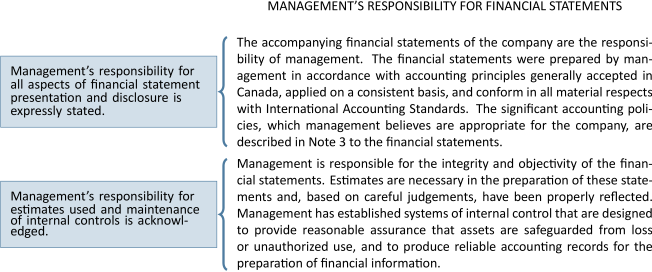

LO5 – Explain the purpose and content of the report that describes management's responsibility for financial statements.

The final piece of information often included with the annual financial statements is a statement describing management's responsibility for the accurate preparation and presentation of financial statements. This statement underscores the division of duties involved with the publication of financial statements. Management is responsible for preparing the financial statements, including estimates that underlie the accounting numbers. An example of an estimate is the useful life of long-lived assets in calculating depreciation.

The independent auditor is responsible for examining the financial statement information as prepared by management, including the reasonableness of estimates, and then expressing an opinion on their accuracy. In some cases, the auditor may assist management with aspects of financial statement preparation. For instance, the auditor may provide guidance on how a new accounting standard will affect financial statement presentation or other information disclosure. Ultimately, however, the preparation of financial statements is management's responsibility.

An example of a statement describing management's responsibility for the preparation and presentation of annual financial statements is shown below.

Summary of Chapter 4 Learning Objectives

LO1 – Explain the importance of and challenges related to basic financial statement disclosure.

The objective of financial statements is to communicate information to meet the needs of external users. In addition to recording and reporting verifiable financial information, accountants make decisions regarding how to measure transactions. Applying GAAP can present challenges when judgment must be applied as in the case of cost-benefit decisions and materiality.

LO2 – Explain and prepare a classified balance sheet.

A classified balance sheet groups assets and liabilities as follows:

| Assets: | Liabilities: |

| Current assets | Current liabilities |

Non-current assets:

|

Non-current or long-term liabilities |

Current assets are those that are used within one year or one operating cycle, whichever is longer, and include cash, accounts receivables, and supplies. Non-current assets are used beyond one year or one operating cycle. There are three types of non-current assets: property, plant, and equipment (PPE), long-term investments, and intangible assets. Long-term investments include investments in shares and bonds. Intangible assets are rights held by the owner and do not have a physical substance; they include copyrights, patents, franchises, and trademarks. Current liabilities must be paid within one year or one operating cycle, whichever is longer. Long-term liabilities are paid beyond one year or one operating cycle. Income statements are also classified (discussed in Chapter 5).

LO3 – Explain the purpose and content of notes to financial statements.

In accordance with the GAAP principle of full disclosure, relevant details not contained in the body of financial statements are included in the accompanying notes to financial statements. Notes would include a summary of accounting policies, details regarding property, plant, and equipment assets, and specifics about liabilities such as the interest rates and repayment terms.

LO4 – Explain the purpose and content of the auditor's report.

An audit as it relates to the auditor's report is an external examination of a company's financial statement information and its system of internal controls. Internal controls are the processes instituted by management of a company to direct, monitor, and measure the accomplishment of its objectives including the prevention and detection of fraud and error. The auditor's report provides some assurance that the financial statements are trustworthy. In simple terms, an unqualified auditor's report indicates that the financial statements are truthful and a qualified auditor's report is one that indicates the financial statements are not or may not be truthful.

LO5 – Explain the purpose and content of the report that describes management's responsibility for financial statements.

This report makes a statement describing management's responsibility for the accurate preparation and presentation of financial statements.

Refer to the Big Dog Carworks Corp. financial statements for the year ended December 31, 2018 and other information included in this chapter to answer the following questions.

- Identify the economic resources of Big Dog Carworks Corp. in its financial statements.

- What comprise the financial statements of BDCC?

- Why does BDCC prepare financial statements?

- From the balance sheet at December 31, 2018 extract the appropriate amounts to complete the following accounting equation: ASSETS = LIABILITIES + EQUITY

- If ASSETS – LIABILITIES = NET ASSETS, how much is net assets at December 31, 2018? Is net assets synonymous with equity?

- What types of assets are reported by Big Dog Carworks Corp.? What types of liabilities?

- What kind of assumptions is made by Big Dog Carworks Corp. about asset capitalisation? Over what periods of time are assets being amortized?

- What adjustments might management make to the financial information when preparing the annual financial statements? Consider the following categories:

- Current asset accounts.

- Non-current asset accounts.

- Current liability accounts.

- Non-current liability accounts.

- What are the advantages of using a classified balance sheet? Why are current accounts shown before non-current ones on BDCC's balance sheet?

- How does Big Dog Carworks Corp. make it easier to compare information from one time period to another?

- Who is the auditor of BDCC? What does the auditor's report tell you about BDCC's financial statements? Does it raise any concerns?

- What does the auditor's report indicate about the application of generally accepted accounting principles in BDCC's financial statements?

- What is BDCC management's responsibility with respect to the company's financial statements? Do the financial statements belong to management? the auditor? the board of directors? shareholders?