3.1: The Operating Cycle

- Page ID

- 97792

Use the following as a self-check while working through Chapter 3.

- What is the GAAP principle of timeliness?

- What is the GAAP principle of matching?

- What is the GAAP principle of revenue recognition?

- What are adjusting entries and when are they journalized?

- What are the five types of adjustments?

- Why is an adjusted trial balance prepared?

- How is the unadjusted trial balance different from the adjusted trial balance?

- What are the four closing entries and why are they journalized?

- Why is the Dividends account not closed to the income summary?

- When is a post-closing trial balance prepared?

- How is a post-closing trial balance different from an adjusted trial balance?

NOTE: The purpose of these questions is to prepare you for the concepts introduced in the chapter. Your goal should be to answer each of these questions as you read through the chapter. If, when you complete the chapter, you are unable to answer one or more the Concept Self-Check questions, go back through the content to find the answer(s). Solutions are not provided to these questions.

3.1 The Operating Cycle

LO1 – Explain how the timeliness, matching, and recognition GAAP require the recording of adjusting entries.

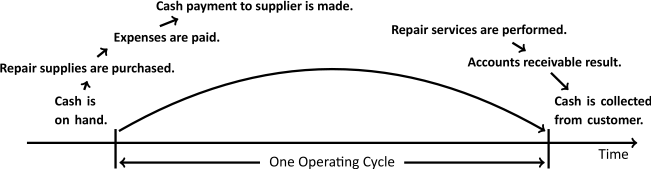

Financial transactions occur continuously during an accounting period as part of a sequence of operating activities. For Big Dog Carworks Corp., this sequence of operating activities takes the following form:

- Operations begin with some cash on hand.

- Cash is used to purchase supplies and to pay expenses.

- Revenue is earned as repair services are completed for customers.

- Cash is collected from customers.

This cash-to-cash sequence of transactions is commonly referred to as an operating cycle and is illustrated in Figure 3.1.

Depending on the type of business, an operating cycle can vary in duration from short, such as one week (e.g., a grocery store) to much longer, such as one year (e.g., a car dealership). Therefore, an annual accounting period could involve multiple operating cycles as shown in Figure 3.2.

Notice that not all of the operating cycles in Figure 3.2 are completed within the accounting period. Since financial statements are prepared at specific time intervals to meet the GAAP requirement of timeliness, it is necessary to consider how to record and report transactions related to the accounting period's incomplete operating cycles. Two GAAP requirements — recognition and matching — provide guidance in this area, and are the topic of the next sections.

Recognition Principle in More Detail

GAAP provide guidance about when an economic activity should be recognized in financial statements. An economic activity is recognized when it meets two criteria:

- it is probable that any future economic benefit associated with the item will flow to the business; and

- it has a value that can be measured with reliability.

Revenue Recognition Illustrated

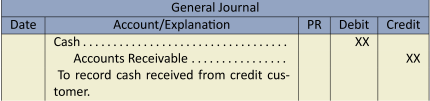

Revenue recognition is the process of recording revenue in the accounting period in which it was earned; this is not necessarily when cash is received. Most corporations assume that revenue has been earned at an objectively-determined point in the accounting cycle. For instance, it is often convenient to recognize revenue at the point when a sales invoice has been sent to a customer and the related goods have been received or services performed. This point can occur before receipt of cash from a customer, creating an asset called Accounts Receivable and resulting in the following entry:

When cash payment is later received, the asset Accounts Receivable is exchanged for the asset Cash and the following entry is made:

Revenue is recognized in the first entry (the credit to revenue), prior to the receipt of cash. The second entry has no effect on revenue.

When cash is received at the same time that revenue is recognized, the following entry is made:

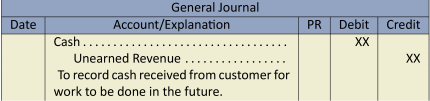

When a cash deposit or advance payment is obtained before revenue is earned, a liability called Unearned Revenue is recorded as follows:

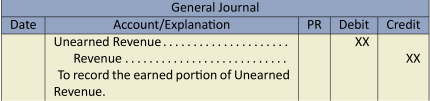

Revenue is not recognized until the services have been performed. At that time, the following entry is made:

The preceding entry reduces the unearned revenue account by the amount of revenue earned.

The matching of revenue to a particular time period, regardless of when cash is received, is an example of accrual accounting. Accrual accounting is the process of recognizing revenues when earned and expenses when incurred regardless of when cash is exchanged; it forms the basis of GAAP. Recognition of expenses is discussed in the next section.

Expense Recognition Illustrated

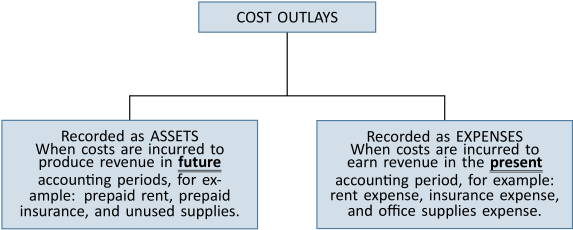

In a business, costs are incurred continuously. To review, a cost is recorded as an asset if it will be incurred in producing revenue in future accounting periods. A cost is recorded as an expense if it will be used or consumed during the current period to earn revenue. This distinction between types of cost outlays is illustrated in Figure 3.3.

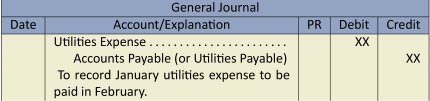

In the previous section regarding revenue recognition, journal entries illustrated three scenarios where revenue was recognized before, at the same time as, and after cash was received. Similarly, expenses can be incurred before, at the same time as, or after cash is paid out. An example of when expenses are incurred before cash is paid occurs when the utilities expense for January is not paid until February. In this case, an account payable is created in January as follows:

The utilities expense is reported in the January income statement.

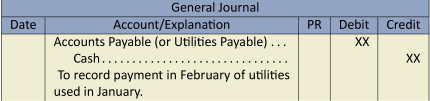

When the January utilities are paid in February, the following is recorded:

The preceding entry has no effect on expenses reported on the February income statement.

Expenses can also be recorded at the same time that cash is paid. For example, if salaries for January are paid on January 31, the entry on January 31 is:

As a result of this entry, salaries expense is reported on the January income statement when cash is paid.

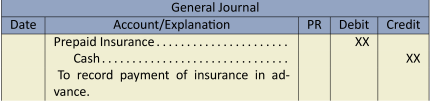

Finally, a cash payment can be made before the expense is incurred, such as insurance paid in advance. A prepayment of insurance creates an asset Prepaid Insurance and is recorded as:

As the prepaid insurance is used, it is appropriate to report an expense on the income statement by recording the following entry:

The preceding examples illustrate how to match expenses to the appropriate accounting period. The matching principle requires that expenses be reported in the same period as the revenues they helped generate. That is, expenses are reported on the income statement: a) when related revenue is recognized, or b) during the appropriate time period, regardless of when cash is paid.

To ensure the recognition and matching of revenues and expenses to the correct accounting period, account balances must be reviewed and adjusted prior to the preparation of financial statements. This is the topic of the next section.

3.2 Adjusting Entries

LO2 – Explain the use of and prepare the adjusting entries required for prepaid expenses, depreciation, unearned revenues, accrued revenues, and accrued expenses.

At the end of an accounting period, before financial statements can be prepared, the accounts must be reviewed for potential adjustments. This review is done by using the unadjusted trial balance. The unadjusted trial balance is a trial balance where the accounts have not yet been adjusted. The trial balance of Big Dog Carworks Corp. at January 31 was prepared in Chapter 2 and appears in Figure 3.4 below. It is an unadjusted trial balance because the accounts have not yet been updated for adjustments. We will use this trial balance to illustrate how adjustments are identified and recorded.

| Big Dog Carworks Corp. | |||

| Unadjusted Trial Balance | |||

| At January 31, 2023 | |||

| Acct. | Account | Debit | Credit |

| 101 | Cash | $3,700 | |

| 110 | Accounts receivable | 2,000 | |

| 161 | Prepaid insurance | 2,400 | |

| 183 | Equipment | 3,000 | |

| 184 | Truck | 8,000 | |

| 201 | Bank loan | $6,000 | |

| 210 | Accounts payable | 700 | |

| 247 | Unearned revenue | 400 | |

| 320 | Share capital | 10,000 | |

| 330 | Dividends | 200 | |

| 450 | Repair revenue | 10,000 | |

| 654 | Rent expense | 1,600 | |

| 656 | Salaries expense | 3,500 | |

| 668 | Supplies expense | 2,000 | |

| 670 | Truck operation expense | 700 | |

| $27,100 | $27,100 | ||

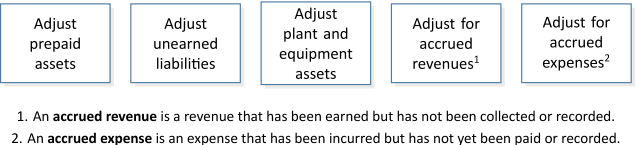

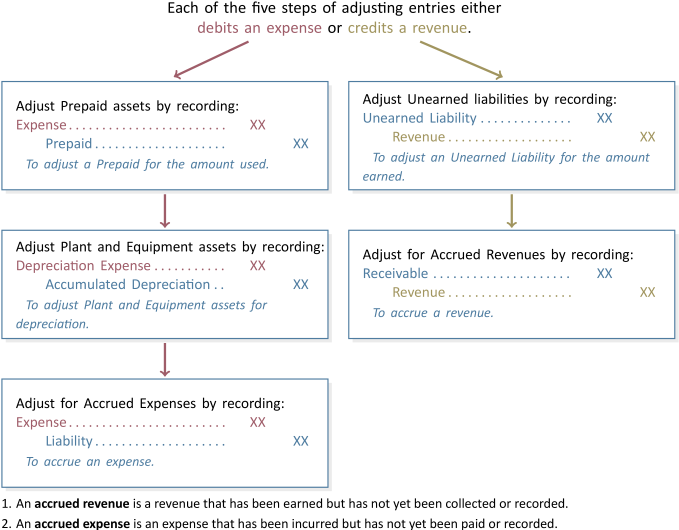

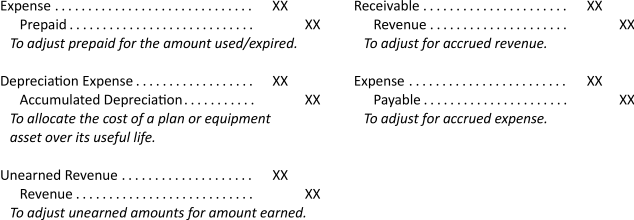

Adjustments are recorded with adjusting entries. The purpose of adjusting entries is to ensure both the balance sheet and the income statement faithfully represent the account balances for the accounting period. Adjusting entries help satisfy the matching principle. There are five types of adjusting entries as shown in Figure 3.5, each of which will be discussed in the following sections.

Adjusting Prepaid Asset Accounts

An asset or liability account requiring adjustment at the end of an accounting period is referred to as a mixed account because it includes both a balance sheet portion and an income statement portion. The income statement portion must be removed from the account by an adjusting entry.

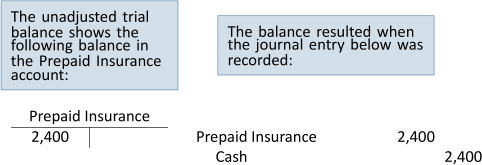

Refer to Figure 3.4 which shows an unadjusted balance in prepaid insurance of $2,400. Recall from Chapter 2 that Big Dog paid for a 12-month insurance policy that went into effect on January 1 (transaction 5).

At January 31, one month or $200 of the policy has expired (been used up) calculated as $2,400/12 months = $200.

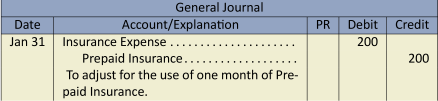

The adjusting entry on January 31 to transfer $200 out of prepaid insurance and into insurance expense is:

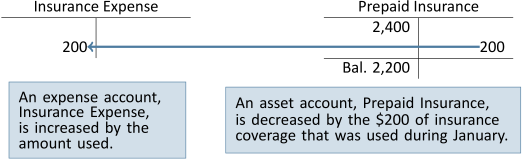

As shown below, the balance remaining in the Prepaid Insurance account is $2,200 after the adjusting entry is posted. The $2,200 balance represents the unexpired asset that will benefit future periods, namely, the 11 months from February to December, 2015. The $200 transferred out of prepaid insurance is posted as a debit to the Insurance Expense account to show how much insurance has been used during January.

If the adjustment was not recorded, assets on the balance sheet would be overstated by $200 and expenses would be understated by the same amount on the income statement.

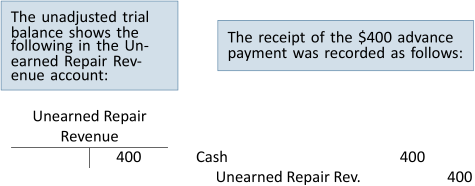

Adjusting Unearned Liability Accounts

On January 15, Big Dog received a $400 cash payment in advance of services being performed.

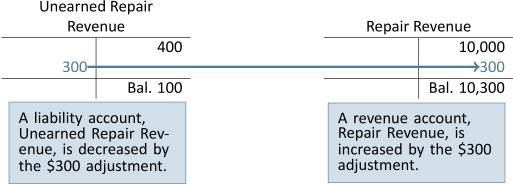

This advance payment was originally recorded as unearned, since the cash was received before repair services were performed. At January 31, $300 of the $400 unearned amount has been earned. Therefore, $300 must be transferred from unearned repair revenue into repair revenue. The adjusting entry at January 31 is:

After posting the adjustment, the $100 remaining balance in unearned repair revenue ($400 – $300) represents the amount at the end of January that will be earned in the future.

If the adjustment was not recorded, unearned repair revenue would be overstated (too high) by $300 causing liabilities on the balance sheet to be overstated. Additionally, revenue would be understated (too low) by $300 on the income statement if the adjustment was not recorded.

Adjusting Plant and Equipment Accounts

Plant and equipment assets, also known as long-lived assets, are expected to help generate revenues over the current and future accounting periods because they are used to produce goods, supply services, or used for administrative purposes. The truck and equipment purchased by Big Dog Carworks Corp. in January are examples of plant and equipment assets that provide economic benefits for more than one accounting period. Because plant and equipment assets are useful for more than one accounting period, their cost must be spread over the time they are used. This is done to satisfy the matching principle. For example, the $100,000 cost of a machine expected to be used over five years is not expensed entirely in the year of purchase because this would cause expenses to be overstated in Year 1 and understated in Years 2, 3, 4, and 5. Therefore, the $100,000 cost must be spread over the asset's five-year life.

The process of allocating the cost of a plant and equipment asset over the period of time it is expected to be used is called depreciation. The amount of depreciation is calculated using the actual cost and an estimate of the asset's useful life and residual value. The useful life of a plant and equipment asset is an estimate of how long it will actually be used by the business regardless of how long the asset is expected to last. For example, a car might have a manufacturer's suggested life of 10 years but a business may have a policy of keeping cars for only 2 years. The useful life for depreciation purposes would therefore be 2 years and not 10 years. The residual value is an estimate of what the plant and equipment asset will be sold for when it is no longer used by a business. Residual value can be zero. There are different formulas for calculating depreciation. We will use the straight-line method of depreciation:

![]()

The cost less estimated residual value is the total depreciable cost of the asset. The straight-line method allocates the depreciable cost equally over the asset's estimated useful life. When recording depreciation expense, our initial instinct is to debit depreciation expense and credit the Plant and Equipment asset account in the same way prepaids were adjusted with a debit to an expense and a credit to the Prepaid asset account. However, crediting the Plant and Equipment asset account is incorrect. Instead, a contra account called accumulated depreciation must be credited. A contra account is an account that is related to another account and typically has an opposite normal balance that is subtracted from the balance of its related account on the financial statements. Accumulated depreciation records the amount of the asset's cost that has been expensed since it was put into use. Accumulated depreciation has a normal credit balance that is subtracted from a Plant and Equipment asset account on the balance sheet.

Initially, the concept of crediting Accumulated Depreciation may be confusing because of how we learned to adjust prepaids (debit an expense and credit the prepaid). Remember that prepaids actually get used up and disappear over time. The Plant and Equipment asset account is not credited because, unlike a prepaid, a truck or building does not get used up and disappear. The goal in recording depreciation is to match the cost of the asset to the revenues it helped generate. For example, a $50,000 truck that is expected to be used by a business for 4 years will have its cost spread over 4 years. After 4 years, the asset will likely be sold (journal entries related to the sale of plant and equipment assets are discussed in Chapter 8).

The adjusting journal entry to record depreciation is:

Subtracting the accumulated depreciation account balance from the Plant and Equipment asset account balance equals the carrying amount or net book value of the plant and equipment asset that is reported on the balance sheet.

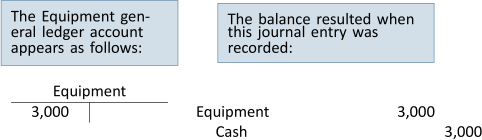

Let's work through two examples to demonstrate depreciation adjustments. Big Dog Carworks Corp.'s January 31, 2023 unadjusted trial balance showed the following two plant and equipment assets:

| Big Dog Carworks Corp. | |||

| Unadjusted Trial Balance | |||

| At January 31, 2023 | |||

| Acct. | Account | Debit | Credit |

| 183 | Equipment | 3,000 | |

| 184 | Truck | 8,000 | |

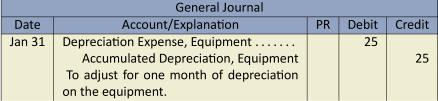

The equipment was purchased for $3,000.

The equipment was recorded as a plant and equipment asset because it has an estimated useful life greater than 1 year. Assume its actual useful life is 10 years (120 months) and the equipment is estimated to be worth $0 at the end of its useful life (residual value of $0).

![]()

Note that depreciation is always rounded to the nearest whole dollar. This is because depreciation is based on estimates — an estimated residual value and an estimated useful life; it is not exact. The following adjusting journal entry is made on January 31:

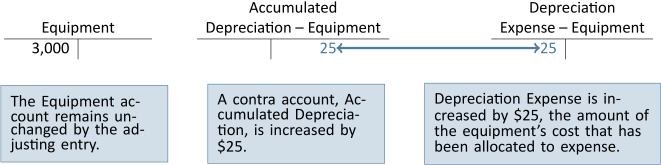

When the adjusting entry is posted, the accounts appear as follows:

For financial statement reporting, the asset and contra asset accounts are combined. The net book value of the equipment on the balance sheet is shown as $2,975 ($3,000 – $25).

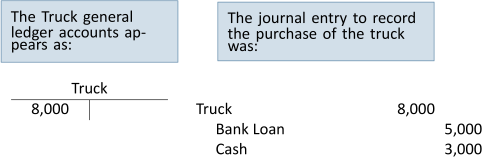

BDCC also shows a truck for $8,000 on the January 31, 2023 unadjusted trial balance.

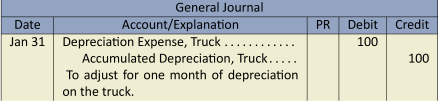

Assume the truck has an estimated useful life of 80 months and a zero estimated residual value. At January 31, one month of the truck cost has expired since it was put into operation in January. Using the straight-line method, depreciation is calculated as:

![]()

The adjusting entry recorded on January 31 is:

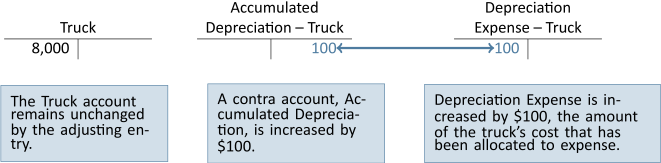

When the adjusting entry is posted, the accounts appear as follows:

For financial statement reporting, the asset and contra asset accounts are combined. The net book value of the truck on the balance sheet is shown as $7,900 ($8,000 – $100).

If depreciation adjustments are not recorded, assets on the balance sheet would be overstated. Additionally, expenses would be understated on the income statement causing net income to be overstated. If net income is overstated, retained earnings on the balance sheet would also be overstated.

It is important to note that land is a long-lived asset. However, it is not depreciated because it does not get used up over time. Therefore, land is often referred to as a non-depreciable asset.

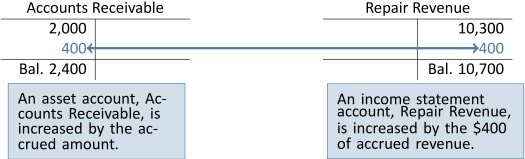

Adjusting for Accrued Revenues

Accrued revenues are revenues that have been earned but not yet collected or recorded. For example, a bank has numerous notes receivable. Interest is earned on the notes receivable as time passes. At the end of an accounting period, there would be notes receivable where the interest has been earned but not collected or recorded. The adjusting entry for accrued revenues is:

For Big Dog Carworks Corp., assume that on January 31, $400 of repair work was completed for a client but it had not yet been collected or recorded. BDCC must record the following adjusting entry:

If the adjustment was not recorded, assets on the balance sheet would be understated by $400 and revenues would be understated by the same amount on the income statement.

Adjusting for Accrued Expenses

Accrued expenses are expenses that have been incurred but not yet paid or recorded. For example, a utility bill received at the end of the accounting period is likely not payable for 2–3 weeks. Utilities for the period have been used but have not yet been paid or recorded. The adjusting entry for accrued expenses is:

Accruing Interest Expense

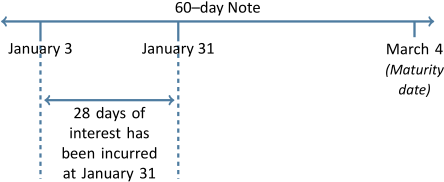

For Big Dog Carworks Corp., the January 31, 2023 unadjusted trial balance shows a $6,000 bank loan balance. Assume it is a 4%, 60-day bank loan1. It was dated January 3 which means that on January 31, 28 days of interest have accrued (January 31 less January 3 = 28 days) as shown in Figure 3.6.

The formula for calculating interest when the term is expressed in days is:

![]()

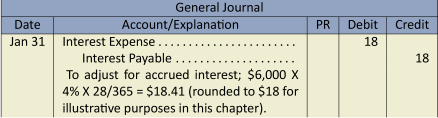

The interest expense accrued at January 31 is calculated as:

![]()

Interest is normally expressed as an annual rate. Therefore, the 28 days must be divided by the 365 days in a year. Normally all interest calculations in this textbook are rounded to two decimal places. However, for simplicity of demonstrations in this chapter, we will round to the nearest whole dollar.

BDCC's adjusting entry on January 31 is:

This adjusting entry enables BDCC to include the interest expense on the January income statement even though the payment has not yet been made. The entry creates a payable that will be reported as a liability on the balance sheet at January 31.

When the adjusting entry is posted, the accounts appear as:

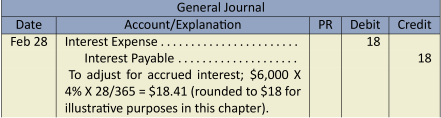

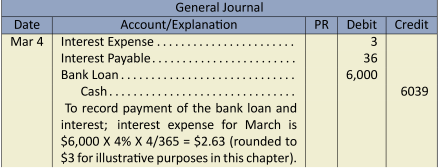

On February 28, interest will again be accrued and recorded as:

On March 4 when the bank loan matures, Big Dog will pay the interest and principal and record the following entry:

The $36 debit to interest payable will cause the Interest Payable account to go to zero since the liability no longer exists once the cash is paid. Notice that the total interest expense recorded on the bank loan was $39 - $18 expensed in January, $18 expensed in February, and $3 expensed in March. The interest expense was matched to the life of the bank loan.

Accruing Income Tax Expense

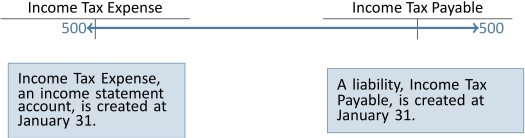

Another adjustment that is required for Big Dog Carworks Corp. involves the recording of corporate income taxes. In most jurisdictions, a corporation is taxed as an entity separate from its shareholders. For simplicity, assume BDCC's income tax due for January 2015 is $500. The adjusting entry is at January 31:

When the adjusting entry is posted, the accounts appear as follows:

The above adjusting entry enables the company to match the income tax expense accrued in January to the income earned during the same month.

The five types of adjustments discussed in the previous paragraphs are summarized in Figure 3.7.

3.3 The Adjusted Trial Balance

LO3 – Prepare an adjusted trial balance and explain its use.

In the last section, adjusting entries were recorded and posted. As a result, some account balances reported on the January 31, 2023 unadjusted trial balance in Figure 2 have changed. Recall that an unadjusted trial balance reports account balances before adjusting entries have been recorded and posted. An adjusted trial balance reports account balances after adjusting entries have been recorded and posted. Figure 3.8 shows the adjusted trial balance for BDCC at January 31, 2023.

In Chapters 1 and 2, the preparation of financial statements was demonstrated using BDCC's unadjusted trial balance. We now know that an adjusted trial balance must be used to prepare financial statements.

| Big Dog Carworks Corp. | ||

| Adjusted Trial Balance | ||

| At January 31, 2023 | ||

| Account Balance | ||

| Account | Debit | Credit |

| Cash | $3,700 | |

| Accounts receivable | 2,400 | |

| Prepaid insurance | 2,200 | |

| Equipment | 3,000 | |

| Accumulated depreciation – equipment | $ 25 | |

| Truck | 8,000 | |

| Accumulated depreciation – truck | 100 | |

| Bank loan | 6,000 | |

| Accounts payable | 700 | |

| Interest payable | 18 | |

| Unearned repair revenue | 100 | |

| Income tax payable | 500 | |

| Share capital | 10,000 | |

| Dividends | 200 | |

| Repair revenue | 10,700 | |

| Depreciation expense – equipment | 25 | |

| Depreciation expense – truck | 100 | |

| Rent expense | 1,600 | |

| Insurance expense | 200 | |

| Interest expense | 18 | |

| Salaries expense | 3,500 | |

| Supplies expense | 2,000 | |

| Truck operation expense | 700 | |

| Income tax expense | 500 | |

| Total debits and credits | $28,143 | $28,143 |

3.4 Using the Adjusted Trial Balance to Prepare Financial Statements

LO4 – Use an adjusted trial balance to prepare financial statements.

In the last section, we saw that the adjusted trial balance is prepared after journalizing and posting the adjusting entries. This section shows how financial statements are prepared using the adjusted trial balance.

The income statement is prepared first, followed by the statement of changes in equity as shown below.

The balance sheet can be prepared once the statement of changes in equity is complete.

Notice how accumulated depreciation is shown on the balance sheet.

3.5 The Accounting Cycle

LO5 – Identify and explain the steps in the accounting cycle.

The concept of the accounting cycle was introduced in Chapter 2. The accounting cycle consists of the steps followed each accounting period to prepare financial statements. These eight steps are:

Step 1: Transactions are analyzed and recorded in the general journal

Step 2: The journal entries in the general journal are posted to accounts in the general ledger

Step 3: An unadjusted trial balance is prepared to ensure total debits equal total credits

Step 4: The unadjusted account balances are analyzed and adjusting entries are journalized in the general journal and posted to the general ledger

Step 5: An adjusted trial balance is prepared to prove the equality of debits and credits

Step 6: The adjusted trial balance is used to prepare financial statements

Step 7: Closing entries are journalized and posted

Step 8: Prepare a post-closing trial balance

Steps 1 through 6 were introduced in this and the preceding chapters. Steps 7 and 8 are discussed in the next section.

3.6 The Closing Process

LO6 – Explain the use of and prepare closing entries and a post-closing trial balance.

At the end of a fiscal year, after financial statements have been prepared, the revenue, expense, and dividend account balances must be zeroed so that they can begin to accumulate amounts belonging to the new fiscal year. To accomplish this, closing entries are journalized and posted. Closing entries transfer each revenue and expense account balance, as well as any balance in the Dividend account, into retained earnings. Revenues, expenses, and dividends are therefore referred to as temporary accounts because their balances are zeroed at the end of each accounting period. Balance sheet accounts, such as retained earnings, are permanent accounts because they have a continuing balance from one fiscal year to the next. The closing process transfers temporary account balances into a permanent account, namely retained earnings. The four entries in the closing process are detailed below.

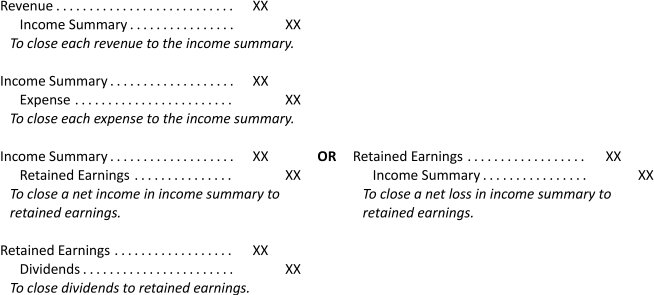

Entry 1: Close the revenue accounts to the income summary account

A single compound closing entry is used to transfer revenue account balances to the income summary account. The income summary is a checkpoint: once all revenue and expense account balances are transferred/closed to the income summary, the balance in the Income Summary account must be equal to the net income/loss reported on the income statement. If not, the revenues and expenses were not closed correctly.

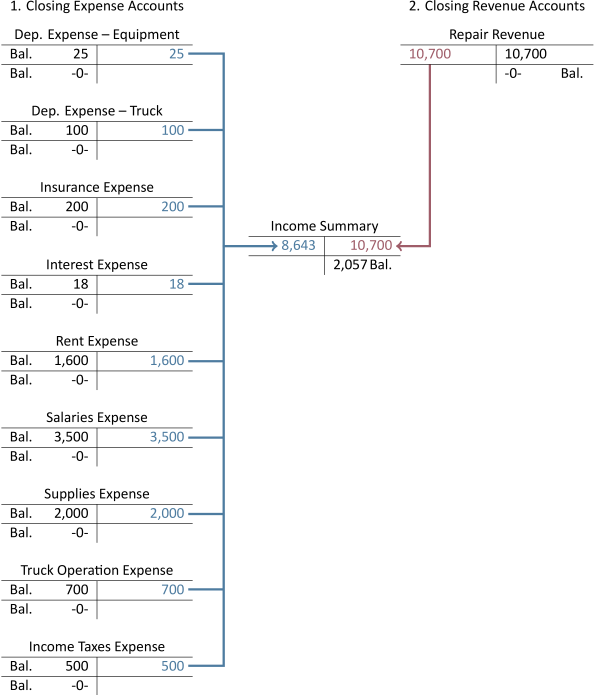

Entry 2: Close the expense accounts to the Income Summary account

The expense accounts are closed in one compound closing journal entry to the Income Summary account. All expense accounts with a debit balance are credited to bring them to zero. Their balances are transferred to the Income Summary account as an offsetting debit.

After entries 1 and 2 above are posted to the Income Summary account, the balance in the income summary must be compared to the net income/loss reported on the income statement. If the income summary balance does not match the net income/loss reported on the income statement, the revenues and/or expenses were not closed correctly.

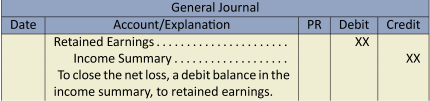

Entry 3: Close the income summary to retained earnings

The Income Summary account is closed to the Retained Earnings account. This procedure transfers the balance in the income summary to retained earnings. Again, the amount closed from the income summary to retained earnings must always equal the net income/loss as reported on the income statement.

Note that the Dividend account is not closed to the Income Summary account because dividends is not an income statement account. The dividend account is closed in Entry 4.

Entry 4: Close dividends to retained earnings

The Dividend account is closed to the Retained Earnings account. This results in transferring the balance in dividends, a temporary account, to retained earnings, a permanent account.

The balance in the Income Summary account is transferred to retained earnings because the net income (or net loss) belongs to the shareholders. The closing entries for Big Dog Carworks Corp. are shown in Figure 3.10.

Posting the Closing Entries to the General Ledger

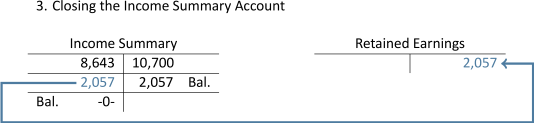

When entries 1 and 2 are posted to the general ledger, the balances in all revenue and expense accounts are transferred to the Income Summary account. The transfer of these balances is shown in Figure 3.11. Notice that a zero balance results for each revenue and expense account after the closing entries are posted, and there is a $2,057 credit balance in the income summary. The income summary balance agrees to the net income reported on the income statement.

When the income summary is closed to retained earnings in the third closing entry, the $2,057 credit balance in the income summary account is transferred into retained earnings as shown in Figure 3.12. As a result, the income summary is left with a zero balance.

This example demonstrated closing entries when there was a net income. When there is a net loss, the Income Summary account will have a debit balance after revenues and expenses have been closed. To close the Income Summary account when there is a net loss, the following closing entry is required:

Finally, when dividends is closed to retained earnings in the fourth closing entry, the $200 debit balance in the Dividends account is transferred into retained earnings as shown in Figure 3.13. After the closing entry is posted, the Dividends account is left with a zero balance and retained earnings is left with a credit balance of $1,857. Notice that the $1,857 must agree to the retained earnings balance calculated on the statement of changes in equity.

The Post–Closing Trial Balance

A post-closing trial balance is prepared immediately following the posting of closing entries. The purpose is to ensure that the debits and credits in the general ledger are equal and that all temporary accounts have been closed. The post-closing trial balance for Big Dog Carworks Corp. appears below.

Note that only balance sheet accounts, the permanent accounts, have balances and are carried forward to the next accounting year. All temporary accounts begin the new fiscal year with a zero balance, so they can be used to accumulate amounts belonging to the new time period.

Summary of Chapter 3 Learning Objectives

LO1 – Explain how the timeliness, matching, and recognition GAAP require the recording of adjusting entries.

Financial statements must be prepared in a timely manner, at minimum, once per fiscal year. For statements to reflect activities accurately, revenues and expenses must be recognized and reported in the appropriate accounting period. In order to achieve this type of matching, adjusting entries need to be prepared.

LO2 – Explain the use of and prepare the adjusting entries required for prepaid expenses, depreciation, unearned revenues, accrued revenues, and accrued expenses.

Adjusting entries are prepared at the end of an accounting period. They allocate revenues and expenses to the appropriate accounting period regardless of when cash was received/paid. The five types of adjustments are:

LO3 – Prepare an adjusted trial balance and explain its use.

The adjusted trial balance is prepared using the account balances in the general ledger after adjusting entries have been posted. Debits must equal credits. The adjusted trial balance is used to prepare the financial statements.

LO4 – Use an adjusted trial balance to prepare financial statements.

Financial statements are prepared based on adjusted account balances.

LO5 – Identify and explain the steps in the accounting cycle.

The steps in the accounting cycle are followed each accounting period in the recording and reporting of financial transactions. The steps are:

- Transactions are analyzed and recorded in the general journal.

- The journal entries in the general journal are posted to accounts in the general ledger.

- An unadjusted trial balance is prepared to ensure total debits equal total credits.

- The unadjusted account balances are analyzed, and adjusting entries are journalized in the general journal and posted to the general ledger.

- An adjusted trial balance is prepared to prove the equality of debits and credits.

- The adjusted trial balance is used to prepare financial statements.

- Closing entries are journalized and posted.

- Prepare a post-closing trial balance.

LO6 – Explain the use of and prepare closing entries and a post-closing trial balance.

After the financial statements have been prepared, the temporary account balances (revenues, expenses, and dividends) are transferred to retained earnings, a permanent account, via closing entries. The result is that the temporary accounts will have a zero balance and will be ready to accumulate transactions for the next accounting period. The four closing entries are:

The post-closing trial balance is prepared after the closing entries have been posted to the general ledger. The post-closing trial balance will contain only permanent accounts because all the temporary accounts have been closed.

- Explain the sequence of financial transactions that occur continuously during an accounting time period. What is this sequence of activities called?

- Do you have to wait until the operating cycle is complete before you can measure income using the accrual basis of accounting?

- What is the relationship between the matching concept and accrual accounting? Are revenues matched to expenses, or are expenses matched to revenues? Does it matter one way or the other?

- What is the impact of the going concern concept on accrual accounting?

- Identify three different categories of expenses.

- What are adjusting entries and why are they required?

- Why are asset accounts like Prepaid Insurance adjusted? How are they adjusted?

- How are plant and equipment asset accounts adjusted? Is the procedure similar to the adjustment of other asset and liability accounts at the end of an accounting period?

- What is a contra account and why is it used?

- How are liability accounts like Unearned Repair Revenue adjusted?

- Explain the term accruals. Give examples of items that accrue.

- Why is an adjusted trial balance prepared?

- How is the adjusted trial balance used to prepare financial statements?

- List the eight steps in the accounting cycle.

- Which steps in the accounting cycle occur continuously throughout the accounting period?

- Which steps in the accounting cycle occur only at the end of the accounting period? Explain how they differ from the other steps.

- Give examples of revenue, expense, asset, and liability adjustments.

- In general, income statement accounts accumulate amounts for a time period not exceeding one year. Why is this done?

- Identify which types of general ledger accounts are temporary and which are permanent.

- What is the income summary account and what is its purpose?

- What is a post-closing trial balance and why is it prepared?