15.5: Accounting for Investment in Bonds

- Page ID

- 26281

We will look at a similar topic but this time we, as a corporation, are purchasing bonds of another company. We will not have a liability because we are the ones purchasing the bond or loaning the money. We record this as an asset called Investment in Bonds.

I found 2 good videos that would work — which do you prefer??

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=276

OR

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=276

Let’s look at another discount example. Assume we purchase $50,000 in bonds of ABC Corporation for $45,000 cash. The bonds have a stated interest rate of 10% paid semi-annually and the bond matures in 5 years.

To record the purchase of these bonds, we record the amount we actually paid for the bonds (we do not use discount or premium accounts):

| Debit | Credit | |

| Investment in Bonds | 45,000 | |

| Cash | 45,000 | |

| To record purchase of ABC company bonds for cash. |

To record receipt of the semi-annual interest payment, we record the receipt of cash interest AND we capitalize the difference between the bond face value $50,000 and the amount we paid $45,000 of $5,000 over the life of the bond using straight-line amortization. The entry would be:

| Debit | Credit | |

| Cash (50,000 x 10% x 6 months / 12 months) | 2,500 | |

| Interest Revenue | 2,500 | |

| To record bond interest received. | ||

| Investment in Bonds ($5,000 / 10 interest payments) | 500 | |

| Interest Revenue | 500 | |

| To record capitalization of bond premium. |

This entry would be made every 6-months for 10 interest payments. At the end of 10 interest payments, Investment in Bonds account would be equal to the bond face value of $50,000. The entry to record receipt of the bond amount at maturity would be:

| Debit | Credit | |

| Cash | 50,000 | |

| Investment in Bonds | 50,000 | |

| To record receipt of bond at maturity. |

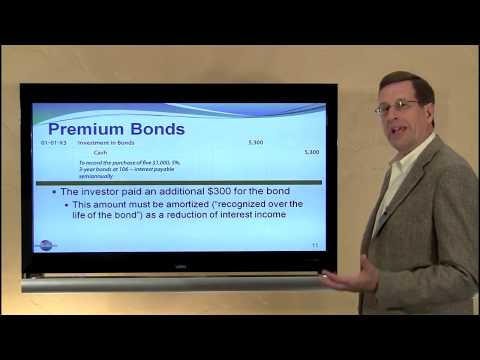

If we pay a higher price for the bonds than the bond face amount, the entries would be the same except we would Debit Interest Revenue and Credit Investment in Bonds with each interest payment.

- Accounting Lecture 15 - Investments in Bonds . Authored by: Craig Pence. License: All Rights Reserved. License Terms: Standard YouTube License

- 9 - Held-to-Maturity Securities . Authored by: Larry Walther. Located at: youtu.be/FCs1lSWa38g. License: All Rights Reserved. License Terms: Standard YouTube License