Kohl’s Corporation (KSS) operates department stores in 49 states in the U.S. and has annual sales in excess of $18 billion. Its fiscal year ends on the Saturday closest to January 31 each year.

Kohl’s has several line items comprising its stockholders’ equity. See the excerpts to follow from Kohl’s 2015 Form 10-K: its Consolidated Balance Sheets, an enlarged partial Consolidated Balance Sheet (page F-3), its Consolidated Statements of Changes in Shareholders’ Equity (page F-5), and a section from its Notes to Financial Statements (page F-8).

Financial Statements

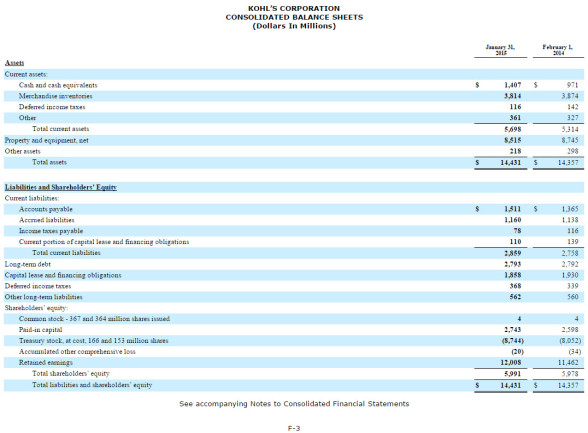

Kohl’s Corporation Consolidated Balance Sheets from p. F-3 of Form 10-K as of January 31, 2015:

Kohl’s Corporation Consolidated Balance Sheets from p. F-3 of Form 10-K as of January 31, 2015 (enlarged Shareholders’ Equity section):

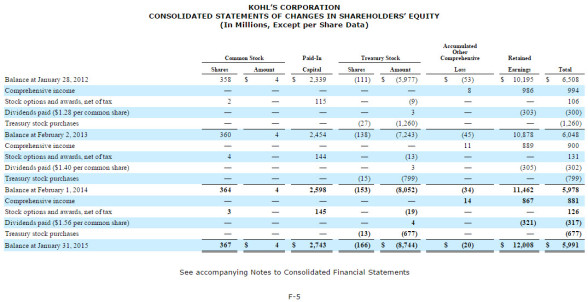

Kohl’s Corporation Consolidated Statements of Changes in Shareholders’ Equity from p. F-5 of Form 10-K as of January 31, 2015:

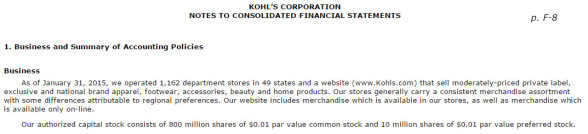

Excerpt from Notes to Financial Statements on p. F-8 of Form 10-K as of January 31, 2015: