3.1: Introduction to Process Costing

- Page ID

- 44212

Process costing is another method of keeping track of the costs of manufactured items. Once products are completed, their overall costs are marked up and sold at a profit to customers. Process costing is used when large quantities of identical items are manufactured in a continuous flow on a first-in, first-out basis. Examples of products that would use process costing are Cheerios brand cereal, iPhones, or Toyota Camrys.

Items enter production in batches rather than individually. A batch is defined as each time a quantity of materials is added to the first point of production to keep the work flow going. Direct costs accumulate and indirect costs are applied to the batches as they move through the production processes. A unit is one of the products that is manufactured in a batch. Eventually, costs are averaged over the units produced during the period to determine the cost of one item.

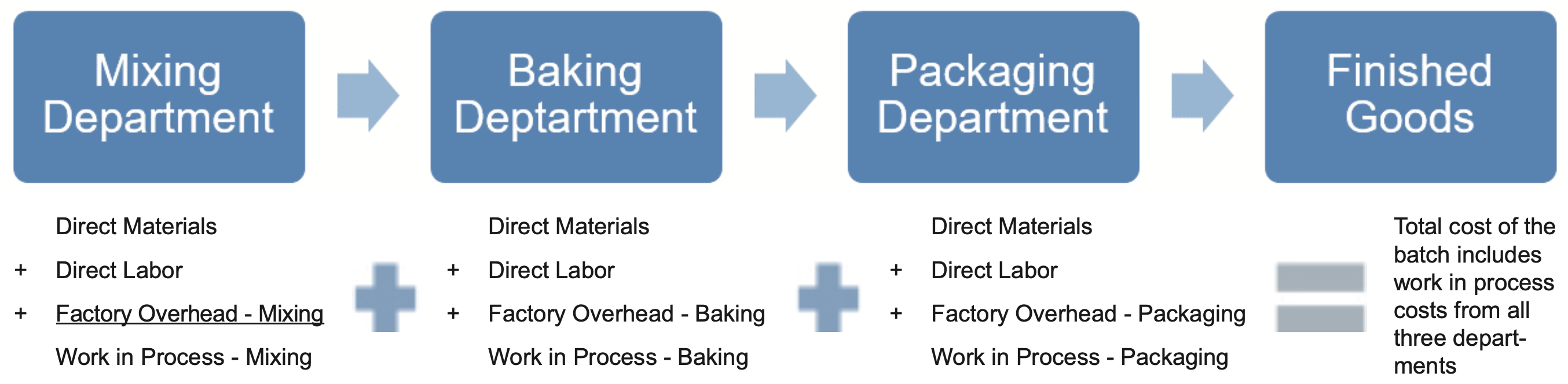

With process costing, products typically move from department to department in a “production line” format instead of the materials and labor coming to the product at one location (as is typically the case in job order costing, where each product is unique). Each department performs a different function and can be considered its own little business or mini-factory. As such, each department adds its own direct materials, direct labor, and factory overhead costs. These three costs accumulate in a departmental account called Work in Process – Department Name, which is like the “tab” of the manufactured item. There will be three debits to Work in Process for each department - one for direct materials, one for direct labor, and one for factory overhead.

As an example, a company manufactures the 16” chocolate chip cookies (yum!) similar to those in the cookie shops in the malls. The company’s factory has three departments: (1) Mixing, (2) Baking, and (3) Packaging. The products move through these departments in order: Mixing first, Baking next, and Packaging last. The process occurs on a FIFO (first in, first out) basis where the first batch started is the first one to be completed. The batch started behind the first batch is the next to be completed, and so forth. Each time the Mixing Department adds more ingredients, a new batch is introduced into the overall production line.

Process costing involves recording product costs for each manufacturing department (or process) as the product moves through. Each department has its own Work in Process and Factory Overhead accounts that include the department names, as follows:

|

Department |

Work in Process account |

Factory Overhead account |

|

Mixing |

Work in Process – Mixing |

Factory Overhead – Mixing |

|

Baking |

Work in Process – Baking |

Factory Overhead – Baking |

|

Packaging |

Work in Process – Packaging |

Factory Overhead – Packaging |

The batch moves from one department to the next. Materials, labor, and factory overhead costs are added in each department. The sum of the departmental work in process costs is the total cost of the batch that is transferred to Finished Goods.