6.10: Cash Dividends Calculations

- Page ID

- 43101

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Preferred stockholders are paid a designated dollar amount per share before common stockholders receive any cash dividends. However, it is possible that the dividend declared is not enough to pay the entire amount per preferred share that is guaranteed before common stockholders receive dividends. In that case the amount declared is divided by the number of preferred shares. Common stockholders would then receive no dividend payment.

Preferred stock may be cumulative or non-cumulative. This determines whether preferred shares will receive dividends in arrears, which is payment for dividends missed in the past due to inadequate amount of dividends declared in prior periods. If preferred stock is non-cumulative, preferred shares never receive payments for past dividends that were missed. If preferred stock is cumulative, any past dividends that were missed are paid before any payments are applied to the current period.

25,000 shares of $3 non-cumulative preferred stock and 100,000 shares of common stock. Preferred shares would receive $75,000 in dividends (25,000 * $3) before common shares would receive anything.

| Preferred Stockholders | Common Stockholders | Owed to | ||||

| Year | Total Dividend | Total | Per Share | Total | Per Share | Preferred |

| 1 | $0 | $0 | $0 | $0 | $0 | $0 |

| 2 | $20,000 | $20,000 | $0.80 | $0 | $0 | $0 |

| 3 | $60,000 | $60,000 | $2.40 | $0 | $0 | $0 |

| 4 | $175,000 | $75,000 | $3.00 | $100,000 | $1.00 | $0 |

| 5 | $200,000 | $75,000 | $3.00 | $125,000 | $1.25 | $0 |

| 6 | $375,000 | $75,000 | $3.00 | $300,000 | $3.00 | $0 |

In years 1 through 3, dividends of less than $75,000 were declared. Since preferred stockholders are entitled to receive the first $75,000 in each year, they receive the entire amount of the dividend declared and the common shareholders receive nothing.

In years 4 through 6, dividends of more than $75,000 were declared. In each of those years, the preferred stockholders receive the first $75,000 and the common stockholders receive the remainder.

The preferred stockholders are never “caught up” for the amounts that were less than $75,000 that they missed out on in years 1 through 3.

25,000 shares of $3 cumulative preferred stock and 100,000 shares of common stock. Preferred shares would receive $75,000 in dividends (25,000 * $3) before common shares would receive anything.

| Preferred Stockholders | Common Stockholders | Owed to | ||||

| Year | Total Dividend | Total | Per Share | Total | Per Share | Preferred |

| 1 | $0 | $0 | $0 | $0 | $0 | $75,000 |

| 2 | $20,000 | $20,000 | $0.80 | $0 | $0 | $130,000 |

| 3 | $60,000 | $60,000 | $2.40 | $0 | $0 | $145,000 |

| 4 | $175,000 | $175,000 | $7.00 | $0 | $0 | $45,000 |

| 5 | $200,000 | $120,000 | $4.80 | $80,000 | $0.80 | $0 |

| 6 | $375,000 | $75,000 | $3.00 | $300,000 | $3.00 | $0 |

In years 1 through 3, dividends of less than $75,000 were declared. Since dividends on preferred stock are cumulative, each year that dividends are declared there is a look back to previous years to ensure that preferred shareholders received their full $75,000 for all past years before any dividends are paid to common stockholders in the current year.

In this example, no dividends are paid on either class of stock in year 1.

In year 2, preferred stockholders must receive $150,000 ($75,000 for year 1 and $75,000 for year 2) before common shareholders receive anything. Since only $20,000 is declared, preferred stockholders receive it all and are still “owed” $130,000 at the end of year 2.

In year 3, preferred stockholders must receive $205,000 ($130,000 in arrears and $75,000 for year 3) before common shareholders receive anything. Since only $60,000 is declared, preferred stockholders receive it all and are still “owed” $145,000 at the end of year 3.

In year 4, preferred stockholders must receive $220,000 ($145,000 in arrears and $75,000 for year 4) before common shareholders receive anything. Since only $175,000 is declared, preferred stockholders receive it all and are still “owed” $45,000 at the end of year 4.

In year 5, preferred stockholders must receive $120,000 ($45,000 in arrears and $75,000 for year 5) before common shareholders receive anything. Since $200,000 is declared, preferred stockholders receive $120,000 of it and common shareholders receive the remaining $80,000.

In year 6, preferred stockholders are not owed any dividends in arrears. Of the $375,000 that is declared, they receive the $75,000 due to them in year 6. Common shareholders receive the remaining $300,000.

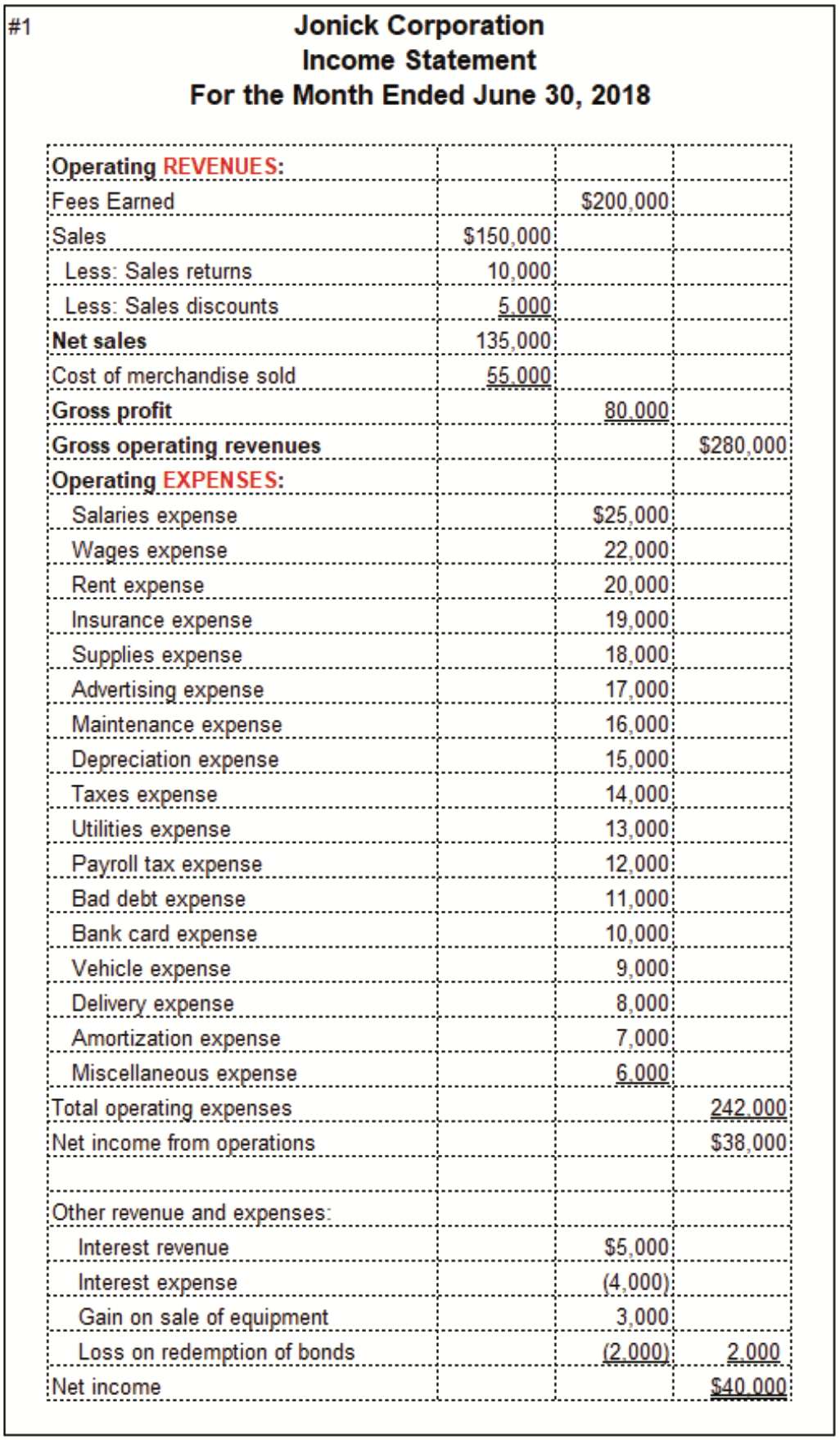

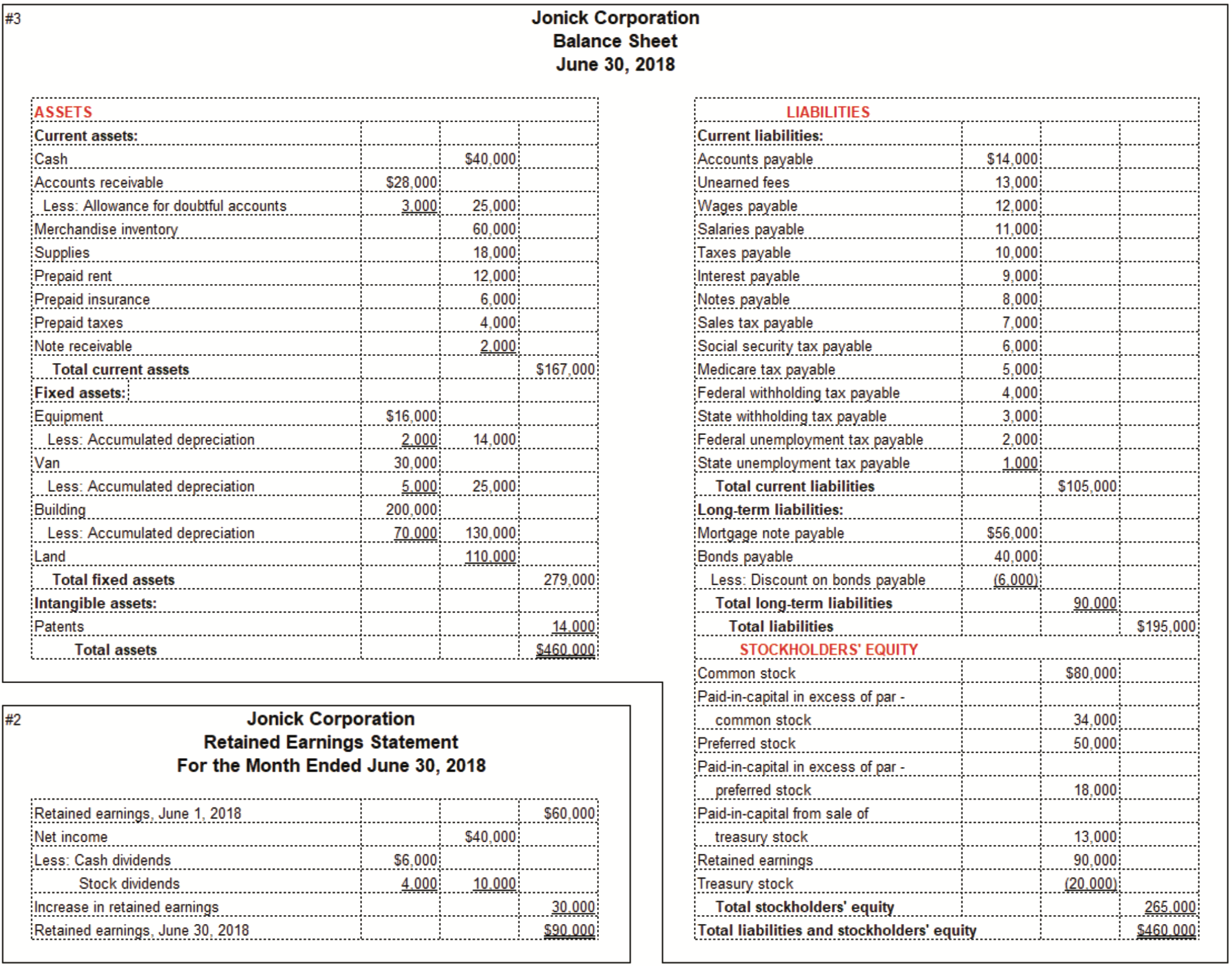

The accounts that are highlighted in bright yellow are the new accounts you just learned. Those highlighted in pale yellow are the ones you learned previously.

At this point you have learned all of the accounts and calculated amounts that are shown below on the income statement, retained earnings statement, and balance sheet. Understanding what these accounts are and how their balances are determined provides you with a sound foundation for learning managerial accounting concepts. You will move from preparing and reading financial statements to using these results for decision making purposes in a business.