5.4: Bonds

- Page ID

- 43090

A corporation often needs to raise money from outside sources for operations, purchases, or expansion. One way to do this is to issue stock. Investors contribute cash to the business and are issued stock in return to recognize their shares of ownership.

Another alternative for raising cash is to borrow the money and to pay it back at a future date. Banks and other traditional lending sources are one option where the corporation may go to take out a loan for the full amount needed.

Another possibility is for the corporation to issue bonds, which are also a form of debt. Bonds are loans made by smaller lenders, such as other corporations and individual people. Corporate bonds are usually issued in $1,000 increments. A corporation may borrow from many different smaller investors and collectively raise the amount of cash it needs. Corporate bonds are traded on the bond market similar to the way corporate stock is traded on the stock market. They are long- term liabilities for most of their life and only become current liabilities as of one year before their maturity date.

The people or companies who purchase bonds from a corporation are called bondholders, and they are essentially lending their money as an investment. The reason bondholders lend their money is because they are paid interest by the corporation on the amount they lend throughout the term of the bond. Bondholders do not become owners of a corporation like stockholders do.

A bond is a loan contract, called a debenture, which spells out the terms and conditions of the loan agreement. At the very least, the debenture states the face amount of the bond, the interest rate, and the term. The face amount is the amount that the bondholder is lending to the corporation. The contract rate of interest is similar to a rental fee that the corporation commits to pay for use of the lenders’ money. It is quoted as an annual percentage, such as 6% per year. Finally, the term is the number of years that the bond covers. The maturity date is the date that the corporation must pay back the full face amount to the bondholders. None of the face amount of the bond is repaid before the maturity date.

There is one other important number to look for: the market rate of interest. Think of it as the interest rate that the competition (other corporations) is offering to the same prospective investors. It may be the same, higher, or lower than an issuing corporation’s contract interest rate.

A corporation’s contract rate is 8%.

| The market rate is 8%. | The contract rate is equal to the market rate. |

| The market rate is 6%. | The contract rate is more than the market rate. |

| The market rate is 10%. | The contract rate is less than the market rate. |

These are new accounts related to issuing bonds:

| Account | Type | Financial Statement | To Increase |

| Bonds Payable | Liability | Balance Sheet | credit |

| Discount on Bonds Payable | Contra liability | Balance Sheet | debit |

| Premium on Bonds Payable | Contra liability | Balance Sheet | credit |

| Interest Expense | Expense | Income Statement | debit |

| Gain on Redemption of Bonds | Revenue | Income Statement | credit |

| Loss on Redemption of Bonds | Expense | Income Statement | debit |

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Liability | Bonds Payable Premium on Bonds Payable | credit | debit | credit |

Balance |

NO |

| Contra Liability | Discount on Bonds Payable | debit | credit | debit | Balance Sheet | NO |

| Revenue | Gain on Redemption of Bonds | credit | debit | credit | Income Statement | YES |

| Expense |

Interest Expense |

debit | credit | debit |

Income |

YES |

There are four journal entries related to issuing bonds, as follows:

- Issuing the bond - accepting cash from bondholders and incurring the debt to pay them back

- Paying semi-annual interest - recording the expense of paying bondholders the contract interest rate every six months

- Amortizing the discount or premium - recording the expense or revenue associated with issuing a bond below or above face amount

- Redeeming the bond - paying back the bondholders on or before the maturity date of the bond

Besides keeping a running balance of each of the new accounts, the key number to determine is the carrying amount of a bond at any point in time. This is the bond’s book value, or what it is worth at the moment.

5.4.1 Bond Transactions When Contract Rate Equals Market Rate

A corporation may borrow money by issuing bonds. In return the corporation will pay the bondholders interest every six months and, at the end of the term, repay the bondholders the face amount. The number of payments bondholders will receive in the future from the corporation is always twice the number of years in the term plus 1.

$100,000 of five-year, 12% bonds when the market rate is 12%.

Number of payments

Over the five-year term of the bond, the bondholders will receive 11 payments: 10 semi-annual interest payments and the one final repayment of the face amount of the bonds.

Semi-annual interest payment amount

To calculate the semi-annual interest, first multiply the face amount of $100,000 by the contract rate of 12% to get the annual amount of interest. Then divide the result by 2 since interest is paid semiannually. The result is (100,000 x 12%)/2 = $6,000 every six months.

Here is a comparison of the 10 interest payments if a company’s contract rate equals the market rate.

| Corporation (pays 12% interest) | Market (pays 12% interest) |

|

$6,000 every six months |

$6,000 every six months |

Since the total interest payments are equal, the corporation’s bond is competitive with other bonds on the market and the bond can be issued at face amount.

Issuing bonds - A journal entry is recorded when a corporation issues bonds.

1/1/11: Issued $100,000 of five-year, 12% bonds when the market rate was 12%.

| Account | Debit | Credit | |

| ▲ | Cash | 100,000 | |

| ▲ | Bonds Payable | 100,000 |

Issuing bonds is selling them to bondholders in return for cash. The issue price is the amount of cash collected from bondholders when the bond is sold. Cash is debited for the amount received from bondholders; the liability (debt) from bonds increases for the face amount.

▲ Cash is an asset account that is increasing.

▲ Bonds Payable is a liability account that is increasing.

Paying semi-annual interest

A corporation typically pays interest to bondholders semi-annually, which is twice per year. In this example the corporation will pay interest on June 30 and December 31.

6/30/11: Paid the semi-annual interest to the bondholders.

| Account | Debit | Credit | ||

| ▲ | Interest Expense | 6,000 | (100,000 x 12%) / 2 | |

| ▼ | Cash | 6,000 | ||

This same journal entry for $6,000 is made every six months, on 6/30 and 12/31, for a total of 10 times over the term of the five-year bond.

▲ Interest Expense is an expense account that is increasing.

▼ Cash is an asset account that is decreasing.

Redeeming bonds - A journal entry is recorded when a corporation redeems bonds.

1/1/16: Redeemed $100,000 of five-year bonds on the maturity date.

| Account | Debit | Credit | |

| ▼ | Bonds Payable | 100,000 | |

| ▼ | Cash | 100,000 | |

Redeeming means paying the bond debt back on the maturity date. The bonds liability decreases by the face amount. Cash decreases and is credited for what is paid to redeem the bonds. In this case, it is the $100,000 face amount. This is the 11th payment by the corporation to the bondholders.

▼ Bonds Payable is a liability account that is decreasing.

▼ Cash is an asset account that is decreasing.

A bond’s contract rate of interest may be equal to, less than, or more than the going market rate.

Compare the contract rate with the market rate since this will impact the selling price of the bond when it is issued.

|

Example: Three interest rate scenarios A three-year, $100,000 bond’s contract rate is 8%. |

|

| The market rate is 8%. |

Contract rate equals market rate |

| The market rate is 10%. |

Contract rate is less than market rate |

| The market rate is 6%. |

Contract rate is greater than market rate |

5.4.2 Bond Transactions When Contract Rate is Less Than Market Rate

There are times when the contract rate that your corporation will pay is less than the market rate that other corporations will pay. As a result, your corporation’s semi-annual interest payments will be lower than what investors could receive elsewhere. To be competitive and still attract investors, the bond must be issued at a discount. This means the corporation receives less cash than the face amount of the bond when it issues the bond. This difference is the discount. The corporation still pays the full face amount back to the bondholders on the maturity date.

$100,000 of five-year, 11% bonds when the market rate was 12%.

Here is a comparison of the 10 interest payments if a company’s contract rate is less than the market rate.

| Corporation (pays 11% interest) | Market (pays 12% interest) |

|

$5,500 every six months |

$6,000 every six months |

In this case, the corporation is offering an 11% interest rate, or a payment of $5,500 every six months, when other companies are offering a 12% interest rate, or a payment of $6,000 every six months. As a result, the corporation will pay out $55,000 in interest over the five-year term. Comparable bonds on the market will pay out $60,000 over this same time frame. This is a difference of $5,000 over ten years.

To compensate for the fact that the corporation will pay out $5,000 less in interest, it will charge investors $5,000 less to purchase the bonds and collect $95,000 instead of $100,000. This is essentially paying them the $5,000 difference in interest up front since it will still pay bondholders the full $100,000 face amount at the end of the five-year term.

You may have heard of ways car manufacturers encourage people to buy vehicles. One is zero-percent financing, which is essentially an interest-free loan. This saves borrowers money because they do not have to pay interest on their loans, which can amount to quite a savings. Another incentive car manufacturers may offer is a rebate, which is an up-front reduction off the purchase price, similar to a coupon for a food purchase.

If a manufacturer offers both zero-percent interest and a rebate, the car buyer can choose one or the other—but not both. Guess what—both deals are probably about equal in terms of savings. So why would both be offered? Because some people will be attracted to buy because of lower payments over time and others will be interested due to the lower up- front purchase price. The deals are designed to appeal to different types of people with different buying preferences.

It is similar with bonds. Some investors prefer to pay full price and have higher interest payments every six months. Others are attracted by paying less up front and being paid back the full face amount at maturity and are willing to live with the lower semi-annual interest payments. Both deals are equal in value but are structured to appeal to different markets.

There are four journal entries that relate to bonds that are issued at a discount.

- Issuing bonds - A journal entry is recorded when a corporation issues bonds.

1/1/11: Issued $100,000 of five-year, 11% bonds when the market rate was 12% for $95,000.

Account Debit Credit ▲ Cash 95,000 (100,000 – 5,000) ▲ Discount on Bonds Payable 5,000 ▲ Bonds Payable 100,000 The company receives cash from bondholders and its liability (debt) from bonds increases for the face amount. The difference between the face amount and the lesser amount of cash received is a discount.

▲ Cash is an asset account that is increasing.

▲ Discount on Bonds Payable is a contra liability account that is increasing.▲ Bonds Payable is a liability account that is increasing.

The corporation will be paying out $5,000 less in interest over the next five years, so to compensate it reduces the purchase price of the bonds by $5,000. Now the value of the corporation’s bond is comparable in value to other bonds on the market.

IMPORTANT: There is one final step to properly issuing bonds at a discount. The Cash and Discount on Bonds Payable amounts must be adjusted to their present value. In this example, the amount of cash received is $96,321, and the discount amount is $3,679.

This is the correct journal entry for issuing the bonds at a discount in this example.

1/1/11: Issued $100,000 of five-year, 11% bonds when the market rate was 12% for $96,321.

Account Debit Credit ▲ Cash 96,321 (100,000 – 3,679) ▲ Discount on Bonds Payable 3,679 ▲ Bonds Payable 100,000 ▲ Cash is an asset account that is increasing.

▲ Discount on Bonds Payable is a contra liability account that is increasing.

▲ Bonds Payable is a liability account that is increasing.

Although it may not seem so, the $96,321 is the $95,000 from above and the $3,679 is the $5,000 from above. These differences are a result of a financial concept called the time value of money, which states that $1 today is worth more than $1 in the future.

- The corporation pays interest of 11% annually, which is the rate it promises to pay in the contract, in spite of the fact that the market rate is 12%.

6/30/11: Paid the semi-annual interest to the bondholders.

Account Debit Credit ▲ Interest Expense 5,500 (100,000 x 11%) / 2 ▼ Cash 5,500 This same journal entry for $5,500 is made every six months, on 6/30 and 12/31, for a total of 10 times over the term of the five-year bond.

▲ Interest Expense is an expense account that is increasing.

▼ Cash is an asset account that is decreasing.

- The corporation issued the bond January 1 at a $3,679 discount: it received $96,321 in cash on the issue date but will pay back $100,000 on the maturity date. That $3,679 difference is a cost of doing business for this company. Instead of claiming this entire discount amount as interest expense when the bond is issued, the company records it in the Discount on Bonds Payable account.

At the end of each year, the corporation will make an adjusting entry that amortizes the discount, or expenses part of it off. The discount amount is divided by the number of years in the term of the bond, and that amount is removed from the Discount on Bonds Payable account and recorded as Interest Expense. Amortization is similar to depreciation in terms of expensing a transaction off over time; it applies to an intangible rather than a physical product.

In this case, the $3,679 discount is divided by 5, the number of years of the term of the bond, resulting in $736 per year (rounded to the nearest dollar.) This becomes a debit to interest expense each year. The original debit balance in the Discount on Bonds Payable account is reduced by a credit of $736 each year.

12/31/11: Amortized the discount for the year.

Account Debit Credit ▲ Interest Expense 736 3,679 / 5 (rounded) ▼ Discount on Bonds Payable 736 This same journal entry for $736 made at the end of each year on 12/31, for a total of five times over the term of the five-year bond. After recording this adjusting entry at the end of each of five years, the balance in Discount on Bonds Payable will be zero.

▲ Interest Expense is an expense account that is increasing.

▼ Discount on Bonds Payable is a contra liability account that is decreasing. - Redeeming bonds - A journal entry is recorded when a corporation redeems bonds.

12/31/15: Redeemed the $100,000 five-year bonds on the maturity date.

Account Debit Credit ▼ Bonds Payable 100,000 ▼ Cash 100,000 Redeeming means paying the bond debt back on the maturity date. The bonds liability decreases by the face amount. Cash decreases and is credited for what is paid to redeem the bonds. In this case, it is the $100,000 face amount. This is the 11th payment by the corporation to the bondholders.

▼ Bonds Payable is a liability account that is decreasing.

▼ Cash is an asset account that is decreasing.After five years the Discount on Bonds Payable account has a zero balance, so nothing needs to be done with this account at this time.

5.4.3 Carrying Amount of Bonds Issued at a Discount

The carrying amount can be thought of as “what the bond is worth” at a given point in time. Initially, the carrying amount is the amount of cash received when the bond is issued.

Calculate the carrying amount as follows:

Bonds Payable credit balance - Discount on Bonds Payable debit balance = Carrying amount

Each year the discount is amortized, the carrying amount changes. The Discount on Bonds Payable debit balance decreases, so the carrying amount increases and gets closer and closer to the face amount over time. At the maturity date, the carrying amount equals the face amount.

In this example, the Bonds Payable credit balance is always $100,000. Notice on the ledger at the right below that each time the end-of-year adjusting entry is posted, the debit balance of the Discount on Bonds Payable decreases. As a result, the carrying amount increases and gets closer and closer to face amount over time.

| Carrying amount = 100,000 – Discount on BP balance | Discount on Bonds Payable | |||||||||

| Carrying amount | Date | Item | Debit | Credit | Debit | Credit | ||||

| 1/1/11 | 100,000 – 3,679 | = | 96,321 | 1/1/11 | 3,679 | 3,679 | ||||

| 12/31/11 | 100,000 – 2,943 | = | 97,057 | 12/31/11 | 736 | 2,943 | ||||

| 12/31/12 | 100,000 – 2,207 | = | 97,793 | 12/31/12 | 736 | 2,207 | ||||

| 12/31/13 | 100,000 – 1,471 | = | 98,529 | 12/31/13 | 736 | 1,471 | ||||

| 12/31/14 | 100,000 – 735 | = | 99,265 | 12/31/14 | 736 | 735 | ||||

| 12/31/15 | 100,000 – 0 | = | 100,000 | 12/31/15 | 735 | 0 | ||||

*Last credit amount differs due to rounding

Besides keeping a running balance of each of the new accounts, the key number to determine is the carrying amount of a bond at any point in time. This is the bond’s book value, or what it is worth at the moment.

5.4.4 Bond Transactions When Contract Rate is More Than Market Rate

There are times when the contract rate that your corporation will pay is more than the market rate that other corporations will pay. As a result, your corporation’s semi-annual interest payments will be higher than what investors could receive elsewhere. Since its future interest payments will be higher in comparison to other bonds on the market, the corporation can command a higher amount up front when the bond is issued, and the bond is sold at a premium. This means the corporation receives more cash than the face amount of the bond when it issues the bond. This difference is the premium. The corporation still pays the face amount back to the bondholders on the maturity date.

$100,000 of five-year, 12% bonds when the market rate was 11%.

Here is a comparison of the 10 interest payments if a company’s contract rate is more than the market rate.

| Corporation (pays 12% interest) | Market (pays 11% interest) |

|

$6,000 every six months |

$5,500 every six months |

In this case, the corporation is offering a 12% interest rate, or a payment of $6,000 every six months, when other companies are offering an 11% interest rate, or a payment of $5,500 every six months. As a result, the corporation will pay out $60,000 in interest over the five-year term. Comparable bonds on the market will pay out $55,000 over this same time frame. This is a difference of $5,000 over five years.

To compensate for the fact that the corporation will pay out $5,000 more in interest, it will charge investors $5,000 more to purchase the bonds and will collect $105,000 instead of $100,000. This is essentially collecting the $5,000 difference in interest up front from investors and essentially using it to pay them the higher interest rate over time. The corporation will still pay bondholders the $100,000 face amount at the end of the five-year term.

There are four journal entries that relate to bonds that are issued at a premium.

- Issuing bonds - A journal entry is recorded when a corporation issues bonds.

1/1/11: Issued $100,000 of five-year, 12% bonds when the market rate was 11% for $105,000.

Account Debit Credit ▲ Cash 105,000 (100,000 + 5,000) ▲ Premium on Bonds Payable 5,000 ▲ Bonds Payable 100,000 The company receives cash from bondholders and its liability (debt) from bonds increases for the face amount. The difference between the amount of cash received and the lesser face amount is a premium.

▲ Cash is an asset account that is increasing.

▲ Premium on Bonds Payable is a contra liability account that is increasing.

▲ Bonds Payable is a liability account that is increasing.

The corporation will be paying out $5,000 more in interest over the next five years, so to compensate it increases the purchase price of the bonds by $5,000. Now the value of the corporation’s bond is comparable in value to other bonds on the market.

IMPORTANT: There is one final step to properly issuing bonds at a premium. The Cash and Premium on Bonds Payable amounts must be adjusted to their present value. In this example, the amount of cash received is $103,769, and the premium amount is $3,679.

This is the correct journal entry for issuing the bonds at a premium in this example.

1/1/11: Issued $100,000 of five-year, 12% bonds when the market rate was 11% for $103,769.

Account Debit Credit ▲ Cash 103,769 (100,000 + 3,769) ▲ Premium on Bonds Payable 3,769 ▲ Bonds Payable 100,000 ▲ Cash is an asset account that is increasing.

▲ Premium on Bonds Payable is a contra liability account that is increasing.

▲ Bonds Payable is a liability account that is increasing.

Although it may not seem so, the $103,769 is the $105,000 from above and the $3,679 is the $5,000 from above. These differences are a result of a financial concept called the time value of money, which states that $1 today is worth more than $1 in the future.

- The corporation pays interest of 12% annually, which is the rate it promised to pay in the contract, in spite of the fact that the market rate is 11%.

6/30/11: Paid the semi-annual interest to the bondholders.

This same journal entry for $6,000 is made every six months, on 6/30 and 12/31, for a total of 10 times over the term of the five-year bond.Account Debit Credit ▲ Interest Expense 6,000 (100,000 x 12%) / 2 ▼ Cash 6,000 ▲ Interest Expense is an expense account that is increasing.

▼ Cash is an asset account that is decreasing.

- The corporation issued the bond January 1 at a $3,769 premium: it received $103,769 in cash on the issue date but will pay back $100,000 on the maturity date. That $3,769 difference is income for this company. Instead of claiming this entire premium amount as a reduction of interest expense when the bond is issued, the company records it in the Premium on Bonds Payable account.

At the end of each year, the corporation will make an adjusting entry that amortizes the premium, or expense part of it off. The premium amount is divided by the number of years in the term of the bond, and that amount is removed from the Premium on Bonds Payable account and recorded an Interest Expense (as a credit, similar to recognizing it as revenue.) Amortization is similar to depreciation in terms of expensing a transaction off over time; it applies to an intangible rather than a physical product.

In this case, the $3,769 premium is divided by 5, the number of years of the term of the bond, resulting in $754 per year (rounded to the nearest dollar.) This becomes a credit to interest expense each year. The original credit balance in the Premium on Bonds Payable account is reduced by a credit of $754 each year.

12/31/11: Amortized the premium for the year.

Account Debit Credit ▼ Premium on Bonds Payable 754 3,769 / 5 (rounded) ▼ Interest Expense 754 This same journal entry for $754 made at the end of each year on 12/31, for a total of five times over the term of the five-year bond. After recording this adjusting entry at the end of each of five years, the balance in Premium on Bonds Payable will be zero.

▼ Premium on Bonds Payable is a contra liability account that is decreasing

▼ Interest Expense is an expense account that is decreasing.

- Redeeming bonds - A journal entry is recorded when a corporation redeems bonds.

12/31/15: Redeemed the $100,000 five-year bonds on the maturity date.

Account Debit Credit ▼ Bonds Payable 100,000 ▼ Cash 100,000 Redeeming means paying the bond debt back on the maturity date. The bonds liability decreases by the face amount. Cash decreases and is credited for what is paid to redeem the bonds. In this case, it is the $100,000 face amount. This is the 11th payment by the corporation to the bondholders.

▼ Bonds Payable is a liability account that is decreasing.

▼ Cash is an asset account that is decreasing.

After five years the Premium on Bonds Payable account has a zero balance, so nothing needs to be done with this account at this time.

5.4.5 Carrying Amount of Bonds Issued at a Premium

The carrying amount can be thought of as “what the bond is worth” at a given point in time. Initially, the carrying amount is the amount of cash received when the bond is issued.

Calculate the carrying amount as follows:

Bonds Payable credit balance + Premium on Bonds Payable credit balance = Carrying amount

Each year the premium is amortized, the carrying amount changes. The Premium on Bonds Payable credit balance decreases, so the carrying amount decreases and gets closer and closer to the face amount over time. At the maturity date, the carrying amount equals the face amount.

In this example, the Bonds Payable credit balance is always $100,000. Notice on the ledger at the right below that each time the end-of-year adjusting entry is posted, the credit balance of the Premium on Bonds Payable decreases. As a result, the carrying amount decreases and gets closer and closer to face amount over time.

| Carrying amount | Date | Item | Debit | Credit | Debit | Credit | ||||

| 1/1/11 | 100,000 + 3,769 | = | 103,769 | 1/1/11 | 3,769 | 3,769 | ||||

| 12/31/11 | 100,000 + 3,015 | = | 103,015 | 12/31/11 | 754 | 3,015 | ||||

| 12/31/12 | 100,000 + 2,261 | = | 102,261 | 12/31/12 | 754 | 2,261 | ||||

| 12/31/13 | 100,000 + 1,507 | = | 101,507 | 12/31/13 | 754 | 1,507 | ||||

| 12/31/14 | 100,000 + 735 | = | 100,753 | 12/31/14 | 754 | 753 | ||||

| 12/31/15 | 100,000 + 0 | = | 100,000 | 12/31/15 | 753 | 0 |

*Last debit amount differs due to rounding

Besides keeping a running balance of each of the new accounts, the key number to determine is the carrying amount of a bond at any point in time. This is the bond’s book value, or what it is worth at the moment.

5.4.6 Calling Bonds

Calling bonds means that a company pays them back early, before the maturity date. Not all bonds are callable; this must be a stipulation in the bond contract. The conditions of the contract will also determine how much the bond will be called for: exactly face amount, less than face amount, or more than face amount.

- The company may pay bondholders the face amount of $100,000.

- The company may call the bonds for less than face amount and, for example, pay bondholders $99,000 for a $100,000 bond. This could also be worded as “called the bond at 99,” which means 99% of the face amount.

- The company may call the bonds for more than face amount and, for example, pay bondholders $102,000 for a $100,000 bond. This could also be worded as “called the bond at 102,” which means 102% of the face amount.

Take the following steps in preparing the journal entry for calling a bond.

- Determine the carrying amount of the bond - what it is currently worth

- Determine how much the company will pay to redeem the bond early

- Determine the amount of any gain or loss by comparing the carrying amount to the redemption amount

- Debit Bonds Payable for the face amount to zero out its credit balance

- Credit Discount on Bonds Payable for its debit balance to zero out the account OR Debit Premium on Bonds Payable for its credit balance to zero out the account

- Credit Cash for the amount paid to bondholders

- Debit Loss on Redemption of Bonds OR credit Gain on Redemption of Bonds if either applies

Bonds may be redeemed at breakeven, at a gain, or at a loss. As with the sale of fixed assets or investments, it is important to note that any gain or loss when bonds are repaid early is incurred on a transaction that is outside of what occurs in normal business operations.

If a corporation redeems a bond prior to its maturity date, the carrying amount at the time should be compared to the amount of cash the issuing company must pay to call the bond. If the corporation pays more cash than what the bond is worth (the carrying amount), it experiences a loss. If it pays less cash than the bond’s carrying amount, there is a gain.

It is important to note that a gain or loss is incurred on a transaction that is outside of what occurs in normal business operations and therefore is not categorized as an operating revenue or expense.

A loss is similar to an expense, except it involves a transaction that is not directly related to the business’ operations. A gain is similar to revenue. It too involves a non-operational transaction. Redeeming bonds is not a corporation’s primary line of business, so these transactions are non-operational.

Let’s say you purchase an airline ticket from Atlanta to San Francisco for $400. While in flight, you learn that the person sitting next to you paid $250 for the same flight. You would probably feel badly and a little cheated for having paid too much. That is similar to paying more than carrying amount to redeem a bond, and that is a loss.

On the flip side, you would feel pretty pleased if you were the one who paid $250 rather than the other passenger’s $400 fare. That is similar to a gain on redemption of bonds, when you pay less than carrying amount to redeem a bond.

The following four examples show bonds at both a discount and a premium that are called at both a gain and a loss.

Bond issued at a discount, called at a loss

| Facts | Calculations |

| Bonds Payable balance: 100,000 credit | Carrying amount is 97,000 (100,000 - 3,000) |

| Discount on Bonds Payable balance: 3,000 debit | Redemption amount is 102,000 (100,000 x 102%) |

| Bonds are called at 102 | Loss on Redemption of Bonds is 5,000 (97,000 - 102,000) |

Calling bonds - A journal entry is recorded when a corporation redeems bonds early.

| Account | Debit | Credit | ||

| ▼ | Bonds Payable | 100,000 | Given | |

| ▲ | Loss on Redemption of Bonds | 5,000 | (100,000 - 3,000) - 102,000 | |

| ▼ | Discount on Bonds Payable | 3,000 | Given | |

| ▼ | Cash | 102,000 | 100,000 x 102% |

Bond issued at a discount, called at a gain

| Facts | Calculations |

| Bonds Payable balance: 100,000 credit | Carrying amount is 97,000 (100,000 - 3,000) |

| Discount on Bonds Payable balance: 3,000 debit | Redemption amount is 96,000 (100,000 x 96%) |

| Bonds are called at 96 | Gain on Redemption of Bonds is 1,000 (97,000 - 96,000) |

Calling bonds - A journal entry is recorded when a corporation redeems bonds early.

| Account | Debit | Credit | ||

| ▼ | Bonds Payable | 100,000 | Given | |

| ▲ | Gain on Redemption of Bonds | 1,000 | (100,000 - 3,000) - 96,000 | |

| ▼ | Discount on Bonds Payable | 3,000 | Given | |

| ▼ | Cash | 96,000 | 100,000 x 96% |

Bond issued at a premium, called at a loss

| Facts | Calculations |

| Bonds Payable balance: 100,000 credit | Carrying amount is 103,000 (100,000 + 3,000) |

| Premium on Bonds Payable balance: 3,000 credit | Redemption amount is 104,000 (100,000 x 104%) |

| Bonds are called at 104 | Loss on Redemption of Bonds is 1,000 (103,000 - 104,000) |

Calling bonds - A journal entry is recorded when a corporation redeems bonds early.

| Account | Debit | Credit | ||

| ▼ | Bonds Payable | 100,000 | Given | |

| ▲ | Premium on Bonds Payable | 3,000 | Given | |

| ▼ | Loss on Redemption of Bonds | 1,000 | (100,000 + 3,000) - 104,000 | |

| ▼ | Cash | 104,000 | 100,000 x 104% |

Bond issued at a premium, called at a gain

| Facts | Calculations |

| Bonds Payable balance: 100,000 credit | Carrying amount is 103,000 (100,000 + 3,000) |

| Premium on Bonds Payable balance: 3,000 credit | Redemption amount is 98,000 (100,000 x 98%) |

| Bonds are called at 98 | Gain on Redemption of Bonds is 5,000 (103,000 - 98,000) |

Calling bonds - A journal entry is recorded when a corporation redeems bonds early.

| Account | Debit | Credit | ||

| ▼ | Bonds Payable | 100,000 | Given | |

| ▼ | Premium on Bonds Payable | 3,000 | Given | |

| ▲ | Gain on Redemption of Bonds | 5,000 | (100,000 + 3,000) - 98,000 | |

| ▼ | Cash | 98,000 | 100,000 x 98% |

5.4.7 Partial Years

In all the previous examples, bonds were issued on January 1 and redeemed on December 31 several years later. In all cases, the bonds were held for full calendar years.

Bonds may also be issued during a calendar year rather than on January 1. They may also be redeemed during a calendar year rather than on December 31. Since the adjusting entries to amortize the discount or premium occur on December 31 of each calendar year, it will be necessary to pro-rate the amortization amount to properly reflect the time during the year that the bond was held.

Issuing bonds mid-year

A five-year bond is issued on April 1, 2012 at a $60,000 premium. The premium is $12,000 per year, or $1,000 per month.

The adjusting entry to amortize the premium on December 31, 2012 is as follows:

| Account | Debit | Credit | The bond was held for 9 months in 2012, so the amount amortized is $9,000 (1,000 x 9). | |

| ▲ | Premium on Bonds Payable | 9,000 | ||

| ▼ | Interest Expense | 9,000 |

Redeeming bonds mid-year

A five-year bond is redeemed on April 1, 2012 at a $60,000 discount. The premium is $12,000 per year, or $1,000 per month.

The adjusting entry to amortize the discount on April 1, 2012 is as follows:

| Account | Debit | Credit | The bond was held for 3 months in 2012, so the amount amortized is $3,000 (1,000 x 3). | |

| ▲ | Interest Expense | 3,000 | ||

| ▼ | Discount on Bonds Payable | 3,000 |

Normally the adjusting entry is recorded on December 31 each year. However, if a bond is redeemed mid-year, an adjusting entry is recorded to bring the carrying up to date as of the date of redemption.

5.4.8 Partial Redemptions

It is possible for a corporation to redeem only some of the bonds that it holds.

Bonds Payable credit balance = $600,000

Discount on Bonds Payable debit balance = $30,000

One-third of the bonds are redeemed for $195,000

| Account | Debit | Credit | ||

| ▼ | Bonds Payable | 200,000 | 600,000 / 3 | |

| ▲ | Loss on Redemption of Bonds | 5,000 | 195,000 - (200,000 - 10,000) | |

| ▼ | Discount on Bonds Payable | 10,000 | 30,000 / 3 | |

| ▼ | Cash | 195,000 | Given |

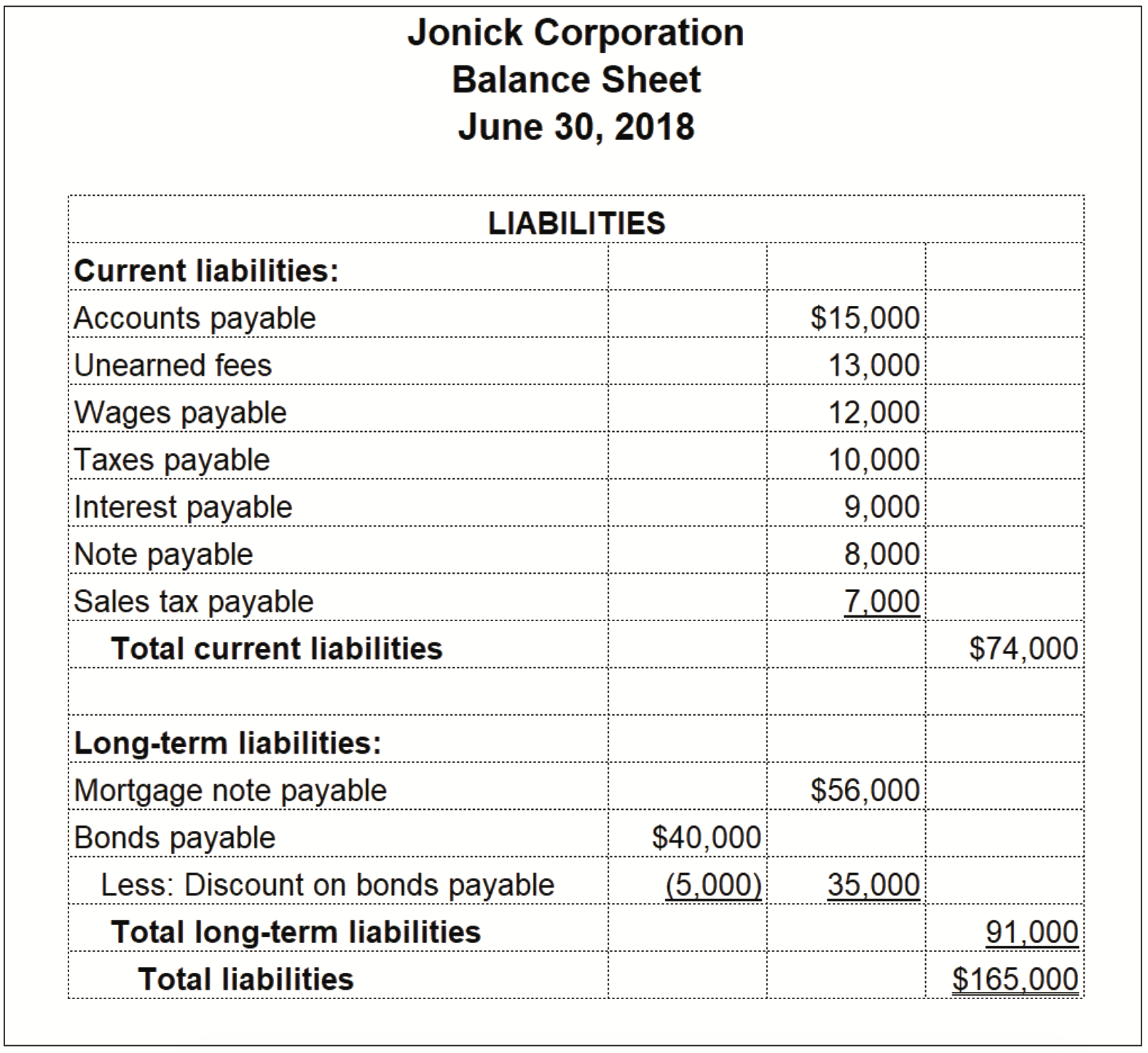

The balances of both current and long-term liabilities are presented in the liabilities section of the balance sheet at the end of each accounting period. When a company has a significant number of liabilities, they are typically presented in categories for clearer presentation. As mentioned previously, a financial statement that organizes its liability (and asset) accounts into categories is called a classified balance sheet.

The partial classified balance sheet that follows shows the liabilities section only. Note that there are two sections. Current liabilities itemizes relatively liabilities that will be converted paid within one year. Long-term liabilities lists liabilities with repayment dates that extend beyond one year. For bond issuances, any unamortized discount or premium amount associated with the debt is listed in conjunction with the bonds payable face amount, and the carrying amount of the bonds is also presented.

The total of each liability category appears in the far-right column of the classified balance sheet, and the sum of these totals appears as total liabilities.

The following Accounts Summary Table summarizes the accounts relevant to issuing bonds.

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Liability |

Sales Tax Payable |

credit | debit | credit | Balance Sheet | NO |

| Contra Liability | Discount on Bonds Payable | debit | credit | debit | Balance Sheet | NO |

| Revenue or Gain | Gain on Redemption of Bonds | credit | debit | credit | Income Statement | YES |

| Expense or Loss |

Interest Expense |

debit | credit | debit | Income Statement | YES |

The accounts that are highlighted in bright yellow are the new accounts you just learned. Those highlighted in light yellow are the ones you learned previously.