4.2: Cash

- Page ID

- 43077

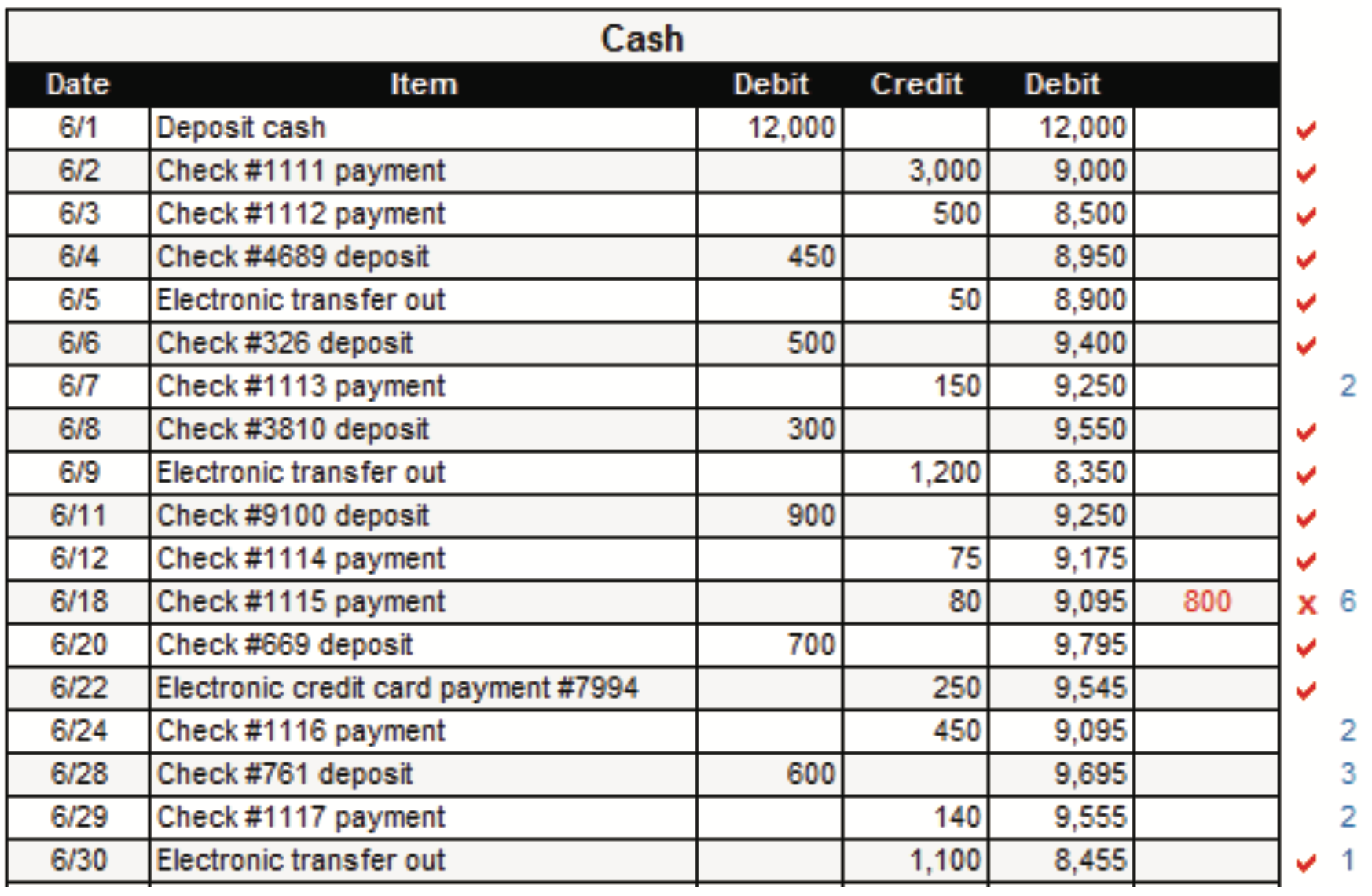

A company journalizes many transactions that involve cash and maintains a Cash ledger to track inflows and outflows and the running cash balance after each entry. A sample ledger for a new business that began on June 1 is shown below.

Almost all companies open a checking account at a bank to safeguard their cash as well as to be able to accept and write checks, transfer funds electronically, and make and receive loan payments.

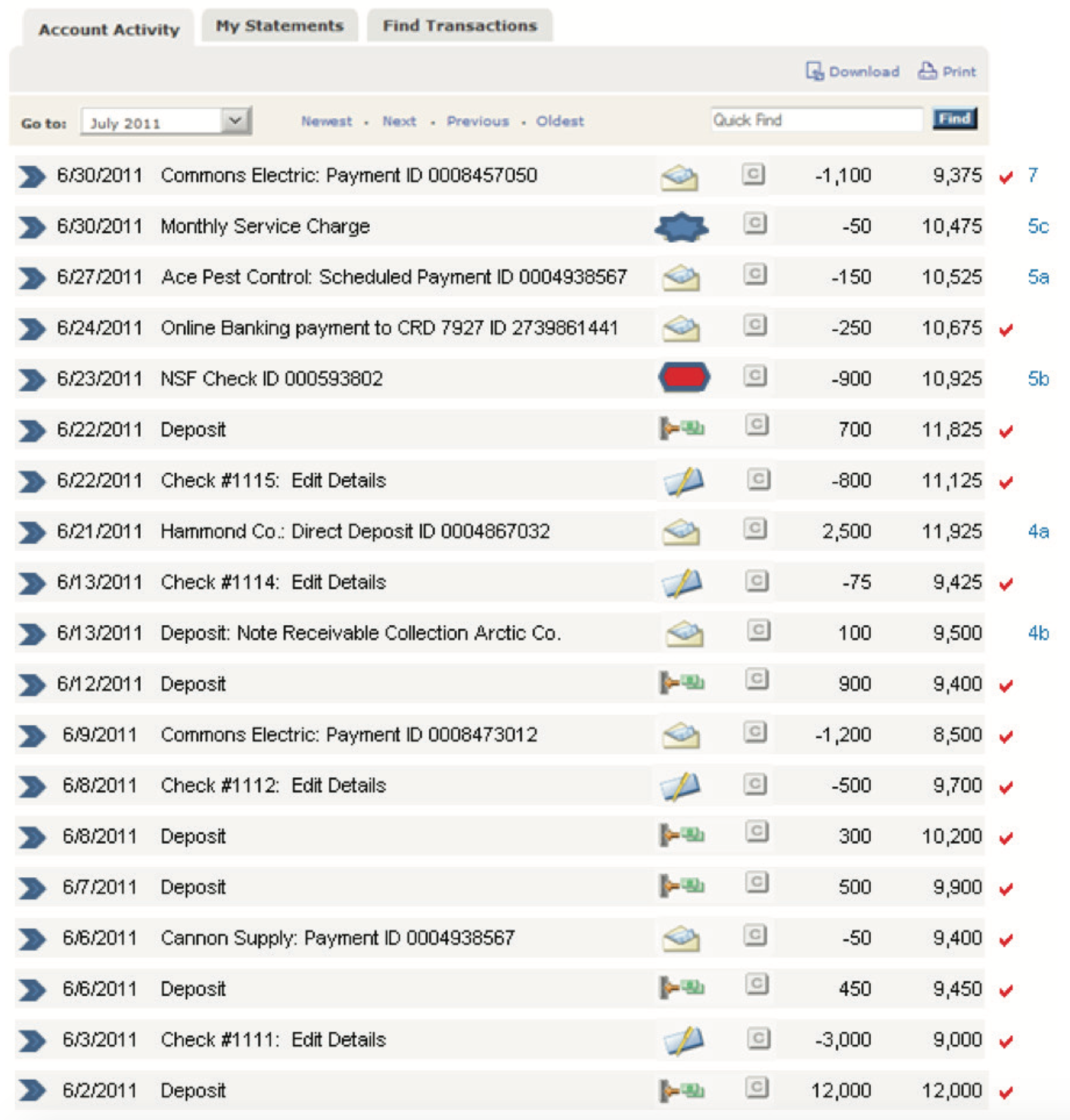

The bank provides an independent record of the account holder’s cash transactions up to the current date on bank statements, which are available online. Each monthly bank statement typically lists a beginning balance, deposits, withdrawals, and an ending balance related to that time period.

The following sample online bank statement lists transactions that a business may typically expect to see each month:

4.2.1 Bank Reconciliation

Since cash is susceptible to theft, fraud, and loss, it is important to continuously verify that the amount shown in the ledger balance is what the business actually has. A bank reconciliation helps do this. A bank reconciliation compares the company’s record of cash on hand to the bank statement, adjusts for missing or incorrect entries, and is complete when the result equals the ending balance on the bank statement. A bank reconciliation should be completed at least once a month but can be done more frequently using online statements that provide up- to-date information.

One key purpose of the bank reconciliation is to notify the account holder of transactions that the bank has processed on the company’s behalf so the company can record them and update its cash balance accordingly.

Begin the reconciliation process by comparing the company’s cash ledger to the bank statement.

First, check off all transactions that match in both the ledger and on the bank statement to indicate that both the company and the bank have recorded these items. This is shown as red checkmarks on the right side in both the sample cash ledger and the sample bank statement on the previous page.

The bank reconciliation is a two-fold process. Essentially what it accomplishes is to update the company’s balance and update the bank balance for items each party did not yet know about and therefore had not recorded at the end of the month.

Secondly, update the company’s Cash ledger balance to include amounts from the bank statement that are not yet listed in the ledger AND adjust for any errors in the ledger. The numbers in blue below correspond to amounts on the previous page in either the Cash ledger account or on the bank statement.

| 1. Note the end-of-month balance in the company’s Cash ledger. | $ 8,455 |

|

Add deposits that appear on the bank statement but not in the ledger. 4a. Electronic transfer in/payment from a customer |

+ 2,500 |

|

Deduct withdrawals that appear on the bank statement but not in the ledger. |

- 150 - 900 - 50 |

| 6. Adjust for any errors in the amounts in the ledger. Since a deduction for check #1115 was entered as $80 rather than $800 in the ledger, the remaining $720 must be deducted. | - 720 |

| Adjusted result | $9,235 |

Next, update the bank statement balance to include amounts in the Cash ledger that do not appear on the bank statement AND adjust for any errors on the bank statement. The numbers in blue below correspond to amounts on the previous page in either the Cash ledger account or on the bank statement.

| 7. Note the end-of-month balance on the company’s bank statement. | $9,375 |

| 3. Add deposits in the ledger that are not yet listed on the bank statement. | + 600 |

| 2. Subtract deductions for checks and withdrawals in the ledger that are not yet listed on the bank statement. |

- 150 - 450 - 140 |

| Adjust for any errors in the amounts on the bank statement. There are none in this example. | |

| Adjusted result | $9,235 |

Then compare the two results to verify that they are equal. They are: both results are $9,235.

The bank reconciliation may be summarized as follows:

| Description | Amount |

| Cash ledger balance per company record as per books | $8,455 |

| Note receivable plus interest collected by the bank | 100 |

| Electronic transfer from a customer's account | 2,500 |

| Bank charges | (50) |

| Electronic transfer to a vendor's account | (150) |

| Returned check due to insufficient funds | (900) |

| Check recording error in the ledger | (720) |

| Adjusted result | $9,235 |

| Description | Amount |

| Bank balance per the bank statement | $9,375 |

| Deposits in transit | 600 |

| Outstanding checks | (740) |

| Adjusted result | $9,235 |

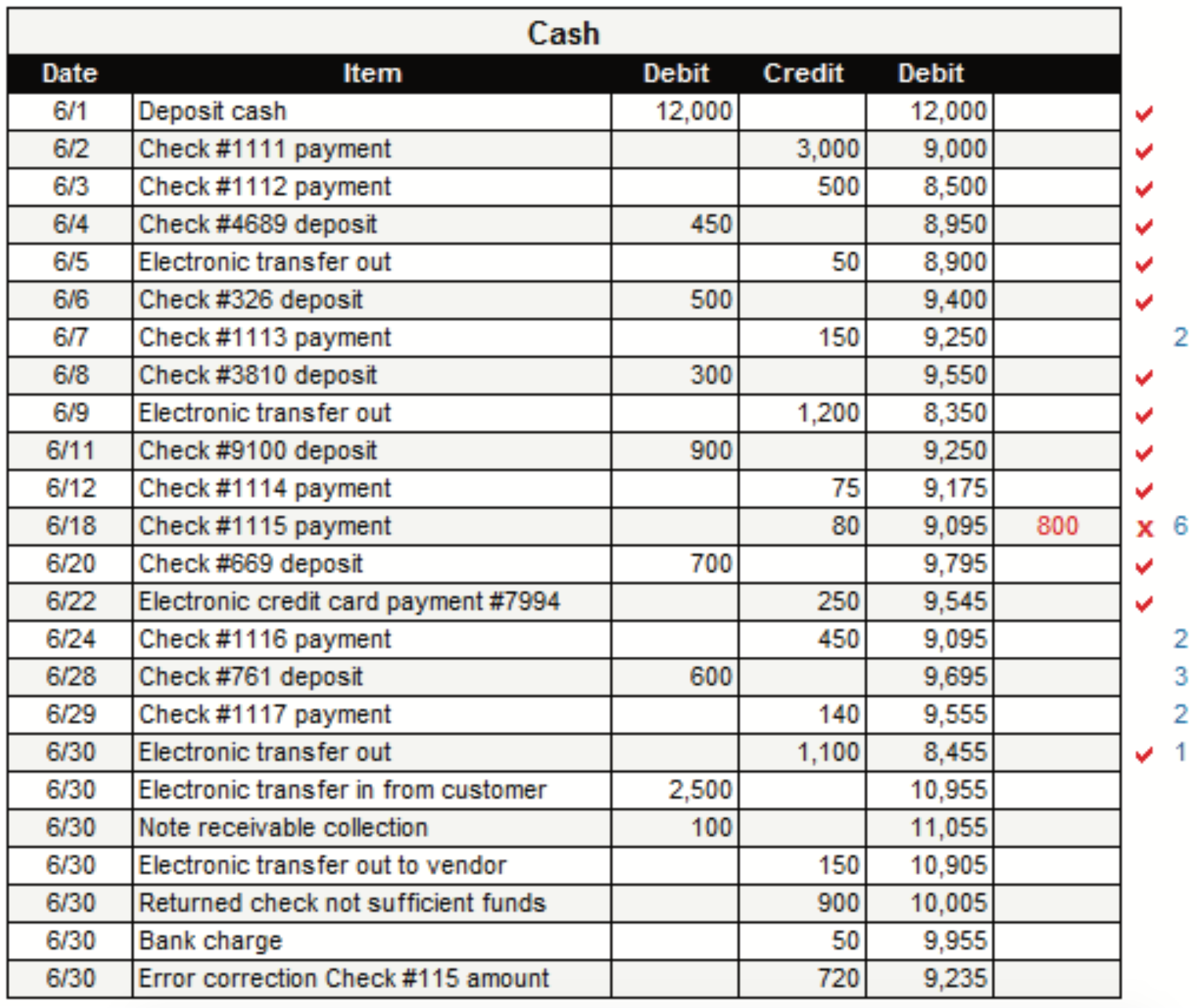

Finally, the company’s Cash ledger must be updated to reflect transactions it has learned about from the bank statement as well as any changes that must be made to correct errors in the company’s books. The notation in blue for each transaction relates back to the instruction numbers on the previous pages.

Electronic payment from customer Hammond Co. on the bank statement

| Date | Account | Debit | Credit | ||

| (4a) | Cash | 2,500 | ▲ Cash is an asset account that is increasing. | ||

| Accounts Receivable | 2,500 | ▼ Accounts Receivable is an asset account that is decreasing. |

Note Receivable collection from Arctic Co. per bank statement

| Date | Account | Debit | Credit | ||

| (4b) | Cash | 100 | ▲ Cash is an asset account that is increasing. | ||

| Note Receivable | 98 | ▼ Notes Receivable is an asset account that is decreasing. | |||

| Interest Revenue | 98 | ▲ Interest Revenue is a revenue account that is increasing. |

Interest Revenue is a revenue account that is increasing.

| Date | Account | Debit | Credit | ||

| (5a) | Maintenance Expense | 150 | ▲ Maintenance Expense is an expense account that is increasing. | ||

| Cash | 150 | ▼ Cash is an asset account that is decreasing. | |||

NSF returned check per bank statement

| Date | Account | Debit | Credit | ||

| (5b) | Accounts Receivable | 900 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Cash | 900 | ▼ Cash is an asset account that is decreasing. | |||

Monthly bank charge per bank statement

| Date | Account | Debit | Credit | ||

| (5c) | Bank Card Expense | 50 | ▲ Bank Card Expense is an expense account that is increasing. | ||

| Cash | 50 | ▼ Cash is an asset account that is decreasing. | |||

Error correction in company’s records – check #1115 should be $800 rather than $80

| Date | Account | Debit | Credit | ▲ Rent Expense is an expense account that is increasing. | |

| Cash | 720 | ▼ Cash is an asset account that is decreasing. | |||

The Cash ledger below has been updated to include the six transactions above.

4.2.2 Bank Card Expense

Businesses that accept credit and debit cards typically pay processing fees to a company that handles the electronic transactions for them. The charges may be flat fees, per transaction fees, or various combinations. The processing company automatically withdraws these fees from the business’s bank account.

On a monthly basis, the processing company sends the business a statement of fees. At that time the business makes the following journal entry to record this cost of accepting credit/debit cards.

18. Paid card processing fees of $300.

| Date | Account | Debit | Credit | ||

| 18 | Bank Card Expense | 300 | |||

| Cash | 300 | ▼ Cash is an asset account that is decreasing. |

Bank Card Expense is an account that keeps track of costs related to accepting credit and debit cards

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Expense | Bank Card Expense | debit | credit | debit | Income Statement | YES |