3.4: Using Activity-Based Costing to Allocate Overhead Costs (Part 1)

- Page ID

- 847

- Understand how to use the five steps of activity-based costing to determine product costs.

Question: Suppose the managers at SailRite Company decide that the benefits of implementing an activity-based costing system would exceed the cost, and thus the company should use activity-based costing to allocate overhead. What are the five steps of activitybased costing, and how would this method work for SailRite?

- Answer

-

Activity-based costing (ABC)4 uses several cost pools, organized by activity, to allocate overhead costs. (Remember that plantwide allocation uses one cost pool for the whole plant, and department allocation uses one cost pool for each department.) The idea is that activities are required to produce products—activities such as purchasing materials, setting up machinery, assembling products, and inspecting finished products. These activities can be costly. Thus the cost of activities should be allocated to products based on the products’ use of the activities.

ABC in Action at SailRite Company

Five steps are required to implement activity-based costing. As you work through the example for SailRite Company, once again note that total estimated overhead costs remain at $8,000,000. However, the total is broken out into different activities rather than departments, and an overhead rate is established for each activity. The five steps are as follows:

Step 1. Identify costly activities required to complete products.

An activity5 is any process or procedure that consumes overhead resources. The goal is to understand all the activities required to make the company’s products.

This requires interviewing and meeting with personnel throughout the organization. Companies that use activity-based costing, such as Hewlett Packard and IBM, may identify hundreds of activities required to make their products. The most challenging part of this step is narrowing down the activities to those that have the biggest impact on overhead costs.

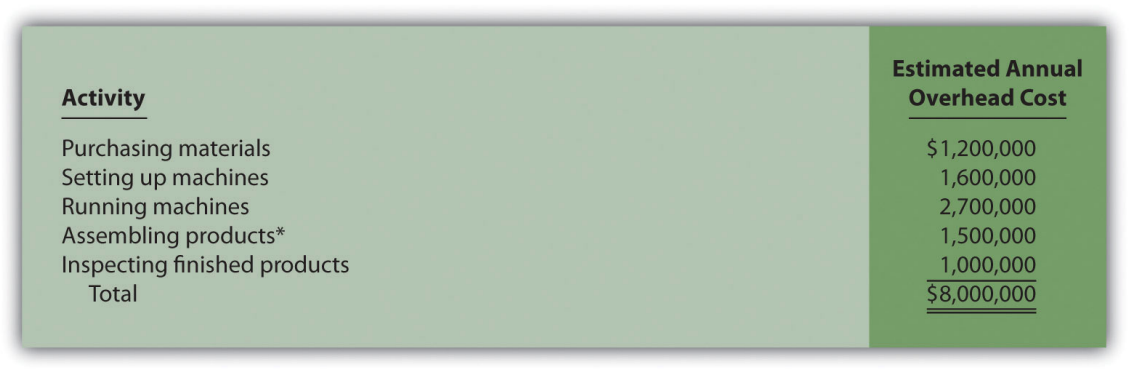

After meeting with personnel throughout the company, SailRite’s accountant identified the following activities as having the biggest impact on overhead costs:

- Purchasing materials

- Setting up machines

- Running machines

- Assembling products

- Inspecting finished products

Step 2. Assign overhead costs to the activities identified in step 1.

This step requires that overhead costs associated with each activity be assigned to the activity (i.e., a cost pool is formed for each activity). For SailRite, the cost pool for the purchasing materials activity will include costs for items such as salaries of purchasing personnel, rent for purchasing department office space, and depreciation of purchasing office equipment.

The accountant at SailRite developed the following allocations after careful review of all overhead costs (remember, these are overhead costs, not direct materials or direct labor costs):

*We should note that this is not the direct labor cost. Instead, this represents overhead costs associated with assembling products, such as supplies and the factory space being used for assembly.

At this point, we have identified the most important and costly activities required to make products, and we have assigned overhead costs to each of these activities. The next step is to find an allocation base that drives the cost of each activity.

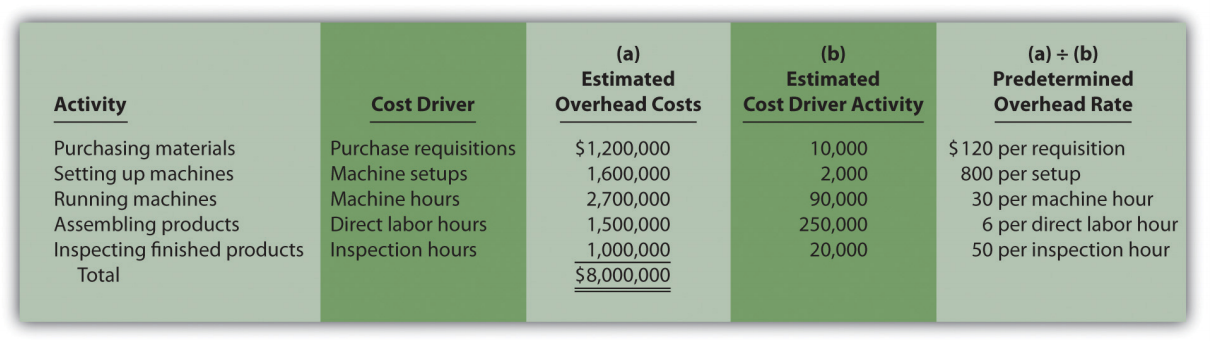

Step 3. Identify the cost driver for each activity.

A cost driver6 is the action that causes (or “drives”) the costs associated with the activity. Identifying cost drivers requires gathering information and interviewing key personnel in various areas of the organization, such as purchasing, production, quality control, and accounting. After careful scrutiny of the process required for each activity, SailRite established the following cost drivers:

| Activity | Cost Driver | Estimated Annual Cost Driver Activity |

|---|---|---|

| Purchasing materials | Purchase requisitions | 10,000 requisitions |

| Setting up machines | Machine setups | 2,000 setups |

| Running machines | Machine hours | 90,000 hours |

| Assembling products | Direct labor hours | 250,000 hours |

| Inspecting finished products | Inspection hours | 20,000 hours |

Notice that this information includes an estimate of the level of activity for each cost driver, which is needed to calculate a predetermined rate for each activity in step 4.

Step 4. Calculate a predetermined overhead rate for each activity.

This is done by dividing the estimated overhead costs (from step 2) by the estimated level of cost driver activity (from step 3). Figure 3.4 provides the overhead rate calculations for SailRite Company based on the information shown in the previous three steps. It shows that products will be charged $120 in overhead costs for each purchase requisition processed, $800 for each machine setup, $30 for each machine hour used, $6 for each direct labor hour worked, and $50 for each hour of inspection time.

Step 5. Allocate overhead costs to products.

Overhead costs are allocated to products by multiplying the predetermined overhead rate for each activity (calculated in step 4) by the level of cost driver activity used by the product. The term applied overhead is often used to describe this process.

Assume the following annual cost driver activity takes place at SailRite for the Basic and Deluxe sailboats:Notice that the total activity levels presented here match the estimated activity levels presented in step 4. This was done to avoid complicating the example with overapplied and underapplied overhead. However, a more realistic scenario would provide actual activity levels that are different than estimated activity levels, thereby creating overapplied and underapplied overhead for each activity. We described the disposition of overapplied and underapplied overhead in Chapter 2.

| Activity | Basic Sailboat | Deluxe Sailboat | Total |

|---|---|---|---|

| Purchasing materials | 7,000 requisitions | 3,000 requisitions | 10,000 requisitions |

| Setting up machines | 1,100 setups | 900 setups | 2,000 setups |

| Running machines | 50,000 hours | 40,000 hours | 90,000 machine hours |

| Assembling products | 200,000 hours | 50,000 hours | 250,000 direct labor hours |

| Inspecting finished products | 12,000 hours | 8,000 hours | 20,000 inspection hours |

Figure 3.5 shows the allocation of overhead using the cost driver activity just presented and the overhead rates calculated in Figure 3.4. Notice that allocated overhead costs total $8,000,000. This is the same cost figure used for the plantwide and department allocation methods we discussed earlier. Activity-based costing simply provides a more refined way to allocate the same overhead costs to products.

*Overhead allocated equals the predetermined overhead rate times the cost driver activity.

**Overhead cost per unit for the Basic model equals $5,020,000 (overhead allocated) ÷ 5,000 units produced, and for the Deluxe model, it equals $2,980,000 ÷ 1,000 units produced.

The bottom of Figure 3.5 shows the overhead cost per unit for each product assuming SailRite produces 5,000 units of the Basic sailboat and 1,000 units of the Deluxe sailboat. This information is needed to calculate the product cost for each unit of product, which we discuss next.

Product Costs Using the Activity-Based Costing Approach at SailRite

Question: As shown in Figure 3.5, SailRite knows the overhead cost per unit using activity-based costing is $1,004 for the Basic model and $2,980 for the Deluxe. Now that SailRite has the overhead cost per unit, how will the company find the total product cost per unit and resulting profit?

- Answer

-

Recall from our discussion earlier that the calculation of a product’s cost involves three components—direct materials, direct labor, and manufacturing overhead. Assume direct materials cost $1,000 for the Basic sailboat and $1,300 for the Deluxe. Direct labor costs are $600 for the Basic sailboat and $750 for the Deluxe. This information, combined with the overhead cost per unit calculated at the bottom of Figure 3.5, gives us what we need to determine the product cost per unit for each model, which is presented in Figure 3.6. The average sales price is $3,200 for the Basic model and $4,500 for the Deluxe. Using the product cost information in Figure 3.6, the Basic model yields a profit of $596 (= $3,200 price – $2,604 cost) per unit and the Deluxe model yields a loss of $530 (= $4,500 price – $5,030 cost) per unit.

Figure \(\PageIndex{6}\): - SailRite Company Product Costs Using Activity-Based Costing As you can see in Figure 3.6, overhead is a significant component of total product costs. This explains the need for a refined overhead allocation system such as activity-based costing.

Definitions

- A method of costing that uses several cost pools, and therefore several predetermined overhead rates, organized by activity to allocate overhead costs.

- Any process or procedure that consumes overhead resources.

- The action that causes the costs associated with an activity.