11.14: How Monopolies Form- Barriers to Entry

- Page ID

- 48431

Learning Objectives

- Describe and give examples of legal monopolies

- Explain how economies of scale and the control of natural resources lead to natural monopolies

- Describe and differentiate between barriers to entry

Barriers to Entry

There are two types of monopoly, based on the kinds of barriers to entry they exploit. One is legal monopoly, where laws prohibit (or severely limit) competition. The other is natural monopoly, where the barriers to entry are something other than legal prohibition.

Legal Monopoly

For some products, the government erects barriers to entry by prohibiting or limiting competition. Under U.S. law, no organization but the U.S. Postal Service is legally allowed to deliver first-class mail. Many states or cities have laws or regulations that allow households a choice of only one electric company, one water company, and one company to pick up the garbage. Most legal monopolies are considered utilities—products necessary for everyday life—that are socially beneficial to have. As a consequence, the government allows producers to become regulated monopolies, to insure that an appropriate amount of these products is provided to consumers.

Promoting Innovation

Innovation takes time and resources to achieve. Suppose a company invests in research and development and finds the cure for the common cold. In this world of near ubiquitous information, other companies could take the formula, produce the drug, and because they did not incur the costs of research and development (R&D), undercut the price of the company that discovered the drug. Given this possibility, many firms would choose not to invest in research and development, and as a result, the world would have less innovation. To prevent this from happening, the Constitution of the United States specifies in Article I, Section 8: “The Congress shall have Power . . . To Promote the Progress of Science and Useful Arts, by securing for limited Times to Authors and Inventors the Exclusive Right to their Writings and Discoveries.” Congress used this power to create the U.S. Patent and Trademark Office, as well as the U.S. Copyright Office. A patent gives the inventor the exclusive legal right to make, use, or sell the invention for a limited time. In the United States, exclusive patent rights last for 20 years. The idea is to provide limited monopoly power so that innovative firms can recoup their investment in R&D, but then to allow other firms to produce the product more cheaply once the patent expires.

A trademark is an identifying symbol or name for a particular good, like Chiquita bananas, Chevrolet cars, or the Nike “swoosh” that appears on shoes and athletic gear. Roughly 1.9 million trademarks are registered with the U.S. government. A firm can renew a trademark over and over again, as long as it remains in active use.

A copyright, according to the U.S. Copyright Office, “is a form of protection provided by the laws of the United States for ‘original works of authorship’ including literary, dramatic, musical, architectural, cartographic, choreographic, pantomimic, pictorial, graphic, sculptural, and audiovisual creations.” No one can reproduce, display, or perform a copyrighted work without permission of the author. Copyright protection ordinarily lasts for the life of the author plus 70 years.

Roughly speaking, patent law covers inventions and copyright protects books, songs, and art. But in certain areas, like the invention of new software, it has been unclear whether patent or copyright protection should apply. There is also a body of law known as trade secrets. Even if a company does not have a patent on an invention, competing firms are not allowed to steal their secrets. One famous trade secret is the formula for Coca-Cola, which is not protected under copyright or patent law, but is simply kept secret by the company.

Taken together, this combination of patents, trademarks, copyrights, and trade secret law is called intellectual property, because it implies ownership over an idea, concept, or image, not a physical piece of property like a house or a car. Countries around the world have enacted laws to protect intellectual property, although the time periods and exact provisions of such laws vary across countries. There are ongoing negotiations, both through the World Intellectual Property Organization (WIPO) and through international treaties, to bring greater harmony to the intellectual property laws of different countries to determine the extent to which patents and copyrights in one country will be respected in other countries.

Natural Monopoly

Natural monopoly occurs where the economics of an industry naturally lead to a single firm dominating the industry. Economies of scale and sole ownership (or control) of a natural resource are two common examples of natural monopoly.

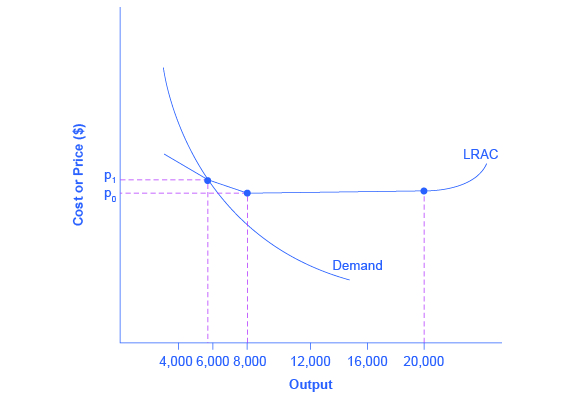

A decreasing cost industry exhibits economies of scale, where the technology is such that the scale of operation matters, so that the long run average cost of production is lower for a large firm than for a small one. Economies of scale can combine with the size of the market to limit competition. Figure 1 presents a long-run average cost curve for the airplane manufacturing industry. It shows economies of scale up to an output of 8,000 planes per year and a price of P0, then constant returns to scale from 8,000 to 20,000 planes per year, and diseconomies of scale at a quantity of production greater than 20,000 planes per year.

Now consider the market demand curve in the diagram, which intersects the long-run average cost (LRAC) curve at an output level of 6,000 planes per year and at a price P1, which is higher than P0. In this situation, the market has room for only one producer. If a second firm attempts to enter the market at a smaller size, say by producing a quantity of 4,000 planes, then its average costs will be higher than the existing firm, and it will be unable to compete. If the second firm attempts to enter the market at a larger size, like 8,000 planes per year, then it could produce at a lower average cost—but it could not sell all 8,000 planes that it produced because of insufficient demand in the market.

Natural monopolies often arise in industries where the marginal cost of adding an additional customer is very low, once the fixed costs of the overall system are in place. Once the main water pipes are laid through a neighborhood, the marginal cost of providing water service to another home is fairly low. Once electricity lines are installed through a neighborhood, the marginal cost of providing additional electrical service to one more home is very low. It would be costly and duplicative for a second water company to enter the market and invest in a whole second set of main water pipes, or for a second electricity company to enter the market and invest in a whole new set of electrical wires. These industries offer an example where, because of economies of scale, one producer can serve the entire market more efficiently than a number of smaller producers that would need to make duplicate physical capital investments.

A natural monopoly can also arise in smaller local markets for products that are difficult to transport. For example, cement production exhibits economies of scale, and the quantity of cement demanded in a local area may not be much larger than what a single plant can produce. Moreover, the costs of transporting cement over land are high, and so a cement plant in an area without access to water transportation may be a natural monopoly.

The following video presents one interesting example of a decreasing cost industry.

Watch it: Decreasing Cost industry

Watch the selected clip from this video to learn about why Dalton, Georgia is known as the “carpet capital of the world.”

An interactive or media element has been excluded from this version of the text. You can view it online here: http://pb.libretexts.org/mecon/?p=362

Control of a Physical Resource

Another type of natural monopoly occurs when a company has sole ownership (or majority control) of a scarce physical resource for which there are no close substitutes. In the U.S. economy, one historical example of this pattern occurred when ALCOA—the Aluminum Company of America—controlled most of the supply of bauxite, a key mineral used in making aluminum. Back in the 1930s, when ALCOA controlled most of the bauxite, other firms were simply unable to produce enough aluminum to compete.

As another example, the majority of global diamond production is controlled by DeBeers, a multi-national company that has mining and production operations in South Africa, Botswana, Namibia, and Canada. It also has exploration activities on four continents, while directing a worldwide distribution network of rough diamonds. Though in recent years they have experienced growing competition, their impact on the rough diamond market is still considerable.

Intimidating Potential Competition

Businesses have developed a number of schemes for creating barriers to entry by deterring potential competitors from entering the market. One method is known as predatory pricing, in which a firm uses the threat of sharp price cuts to discourage competition. Predatory pricing is a violation of U.S. antitrust law, but it is difficult to prove.

Consider a large airline that provides most of the flights between two particular cities. A new, small start-up airline decides to offer service between these two cities. The large airline immediately slashes prices on this route to the bone, so that the new entrant cannot make any money. After the new entrant has gone out of business, the incumbent firm can raise prices again.

After this pattern is repeated once or twice, potential new entrants may decide that it is not wise to try to compete. Small airlines often accuse larger airlines of predatory pricing: in the early 2000s, for example, ValuJet accused Delta of predatory pricing, Frontier accused United, and Reno Air accused Northwest. In late 2009, the American Booksellers Association, which represents independently owned and often smaller bookstores, accused Amazon, Wal-Mart, and Target of predatory pricing for selling new hardcover best-sellers at low prices.

In some cases, large advertising budgets can also act as a way of discouraging the competition. If the only way to launch a successful new national cola drink is to spend more than the promotional budgets of Coca-Cola and Pepsi Cola, not too many companies will try. A firmly established brand name can be difficult to dislodge.

Regulation and Deregulation of Monopolies

Government limitations on competition used to be even more common in the United States. For most of the twentieth century, only one phone company—AT&T—was legally allowed to provide local and long distance service. From the 1930s to the 1970s, one set of federal regulations limited which destinations airlines could choose to fly to and what fares they could charge; another set of regulations limited the interest rates that banks could pay to depositors; yet another specified what trucking firms could charge customers.

What products are considered utilities depends, in part, on the available technology. Fifty years ago, local and long distance telephone service was provided over wires. It did not make much sense to have multiple companies building multiple systems of wiring across towns and across the country. AT&T lost its monopoly on long distance service when the technology for providing phone service changed from wires to microwave and satellite transmission, so that multiple firms could use the same transmission mechanism. The same thing happened to local service, especially in recent years, with the growth in cellular phone systems.

The combination of improvements in production technologies and a general sense that the markets could provide services adequately led to a wave of deregulation, starting in the late 1970s and continuing into the 1990s. This wave eliminated or reduced government restrictions on the firms that could enter, the prices that could be charged, and the quantities that could be produced in many industries, including telecommunications, airlines, trucking, banking, and electricity.

Around the world, from Europe to Latin America to Africa and Asia, many governments continue to control and limit competition in what those governments perceive to be key industries, including airlines, banks, steel companies, oil companies, and telephone companies.

Summing Up Barriers to Entry

Table 1 lists the barriers to entry that have been discussed here. This list is not exhaustive, since firms have proved to be highly creative in inventing business practices that discourage competition. When barriers to entry exist, perfect competition is no longer a reasonable description of how an industry works. When barriers to entry are high enough, monopoly can result.

| Barrier to Entry | Government Role? | Example |

|---|---|---|

| Natural monopoly | Government often responds with regulation (or ownership) | Water and electric companies |

| Control of a physical resource | No | DeBeers for diamonds |

| Legal monopoly | Yes | Post office, past regulation of airlines and trucking |

| Patent, trademark, and copyright | Yes, through protection of intellectual property | New drugs or software |

| Intimidating potential competitors | Somewhat | Predatory pricing; well-known brand names |

Watch It

Watch this video for an overview about monopolies, including their barriers to entry and why the are problematic for market economy.

An interactive or media element has been excluded from this version of the text. You can view it online here: http://pb.libretexts.org/mecon/?p=362

Glossary

[glossary-page][glossary-term]barriers to entry:[/glossary-term]

[glossary-definition]the legal, technological, or market forces that may discourage or prevent potential competitors from entering a market[/glossary-definition][glossary-term]copyright:[/glossary-term]

[glossary-definition]a form of legal protection to prevent copying, for commercial purposes, original works of authorship, including books and music[/glossary-definition][glossary-term]deregulation:[/glossary-term]

[glossary-definition]removing government controls over setting prices and quantities in certain industries[/glossary-definition][glossary-term]economies of scale:[/glossary-term]

[glossary-definition] when a firm faces decreasing long run average costs as its level of output increases[/glossary-definition][glossary-term]intellectual property:[/glossary-term]

[glossary-definition]the body of law including patents, trademarks, copyrights, and trade secret law that protect the right of inventors to produce and sell their inventions[/glossary-definition][glossary-term]legal monopoly:[/glossary-term]

[glossary-definition]legal prohibitions against competition, such as regulated monopolies and intellectual property protection[/glossary-definition][glossary-term]monopoly:[/glossary-term]

[glossary-definition]a situation in which one firm produces all of the output in a market[/glossary-definition][glossary-term]natural monopoly:[/glossary-term]

[glossary-definition]economic conditions in the industry, for example, economies of scale or control of a critical resource, that limit effective competition[/glossary-definition][glossary-term]patent:[/glossary-term]

[glossary-definition]a government rule that gives the inventor the exclusive legal right to make, use, or sell the invention for a limited time[/glossary-definition][glossary-term]predatory pricing:[/glossary-term]

[glossary-definition]when an existing firm uses sharp but temporary price cuts to discourage new competition[/glossary-definition][glossary-term]trade secrets:[/glossary-term]

[glossary-definition]methods of production kept secret by the producing firm[/glossary-definition][glossary-term]trademark:[/glossary-term]

[glossary-definition]an identifying symbol or name for a particular good and can only be used by the firm that registered that trademark[/glossary-definition][/glossary-page]

- Modification, adaptation, and original content. Provided by: Lumen Learning. License: CC BY: Attribution

- How Monopolies Form: Barriers to Entry. Authored by: OpenStax College. Located at: https://cnx.org/contents/vEmOH-_p@4.44:Qr2aBgJh/How-Monopolies-Form-Barriers-t. License: CC BY: Attribution. License Terms: Download for free at http://cnx.org/contents/bc498e1f-efe...69ad09a82@4.44

- Monopolies and Anti-Competitive Markets: Crash Course Economics #25. Provided by: CrashCourse. Located at: https://www.youtube.com/watch?v=Sb_-wfmJnHA&t=533s. License: Other. License Terms: Standard YouTube License

- Entry, Exit, and Supply Curves: Decreasing Costs. Provided by: Marginal Revolution University. Located at: https://www.youtube.com/watch?time_continue=1&v=G82LWt7i8as. License: Other. License Terms: Standard YouTube License