9.15: The Neoclassical Perspective and Potential GDP

- Page ID

- 47419

Learning Objectives

- Explain the importance of potential GDP in the long run to the neoclassical perspective

- Explain the shape and reasoning for the pure neoclassical aggregate supply curve

The neoclassical perspective on macroeconomics is based on two building blocks (or assumptions):

- Since in the long run, the economy will fluctuate around its potential GDP and its natural rate of unemployment, the size of the economy is determined by potential GDP.

- wages and prices will adjust in a flexible manner so that disturbances such as recessions will be temporary and the economy will always return to its potential level of output on its own.

The key policy implication is this: government should focus more on promoting long-term economic growth and on controlling inflation rather than worrying about recession or cyclical unemployment. This focus on long-run growth instead of short-run fluctuations in the business cycle means that neoclassical economics is more useful for long-run macroeconomic analysis and Keynesian economics is more useful for analyzing the macroeconomic short run. Let’s consider the two neoclassical building blocks in turn, and how they can be embodied in the aggregate demand-aggregate supply model.

The Importance of Potential GDP in the Long Run

When economists refer to potential GDP, they are referring to that level of output that can be achieved when all resources (land, labor, capital, and entrepreneurial ability) are fully employed. While the measured unemployment rate in labor markets will never be zero, full employment in the labor market occurs when there is no cyclical unemployment. There will still be some frictional or structural unemployment, but when the economy is operating with zero cyclical unemployment, the economy is said to be at the natural rate of unemployment, or at full employment.

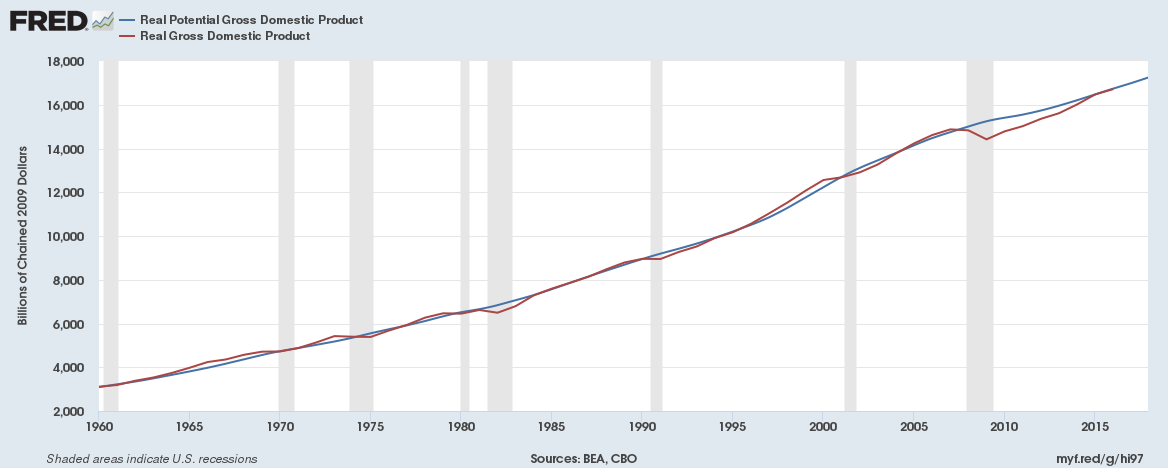

Figure 1 shows potential and actual real GDP from 1960 to 2017 (the data for potential GDP is estimated by the nonpartisan Congressional Budget Office, while the data for real GDP is from the Bureau of Economic Analysis in the U.S. Department of Commerce). What should be clear is that while actual GDP is sometimes above and sometimes below potential, over the long term it tracks potential quite well. For example from 2008 to 2009, the U.S. economy tumbled into recession and remained below its potential. At other times, like in the late 1990s or late 2017, the economy ran at potential GDP—or even slightly ahead. Most economic recessions and upswings are times when the economy is 1–3% below or above potential GDP in a given year. Clearly, short-run fluctuations around potential GDP do exist, but over the long run, the upward trend of potential GDP determines the size of the economy.

The unemployment rate has fluctuated from as low as 3.5% in 1969 to as high as 9.7% in 1982 and 9.6% in 2009. Even as the U.S. unemployment rate rose during recessions and declined during expansions, it kept returning to the general neighborhood of 5.0–5.5%. When the Congressional Budget Office carried out its long-range economic forecasts in 2010, it assumed that from 2015 to 2020, after the recession has passed, the unemployment rate would be 5.0%. From a long-run perspective, the economy seems to keep adjusting back to this rate of unemployment, which we described above as the natural rate.

Growth of Real GDP

Growth in GDP can be explained by investment in physical capital and human capital per person, as well as advances in technology. Physical capital per person refers to the amount and kind of machinery and equipment available to help people get work done. Compare, for example, your productivity in typing a term paper on a typewriter to working on your laptop with word processing software. Clearly, you will be able to be more productive using word processing software. The technology and level of capital of your laptop and software has increased your productivity. More broadly, the development of GPS technology and Universal Product Codes (those barcodes on every product we buy) has made it much easier for firms to track shipments, tabulate inventories, and sell and distribute products. These two technological innovations, and many others, have increased a nation’s ability to produce goods and services for a given population. Likewise, increasing human capital involves increasing levels of knowledge, education, and skill sets per person through vocational or higher education. Physical and human capital improvements with technological advances will increase overall productivity and, thus, GDP.

To see how these improvements have increased productivity and output at the national level, we should examine evidence from the United States. The United States experienced significant growth in the twentieth century due to phenomenal changes in infrastructure, equipment, and technological improvements in physical capital and human capital. The population more than tripled in the twentieth century, from 76 million in 1900 to over 300 million in 2012. The human capital of modern workers is far higher today because the education and skills of workers have risen dramatically. In 1900, only about one-eighth of the U.S. population had completed high school and just one person in 40 had completed a four-year college degree. By 2010, more than 87% of Americans had a high school degree and over 29% had a four-year college degree as well. The average amount of physical capital per worker has grown dramatically. The technology available to modern workers is extraordinarily better than a century ago: cars, airplanes, electrical machinery, smartphones, computers, chemical and biological advances, materials science, health care—the list of technological advances could run on and on. More workers, higher skill levels, larger amounts of physical capital per worker, and amazingly better technology, and potential GDP for the U.S. economy has clearly increased a great deal since 1900.

The Neoclassical Aggregate Supply Curve

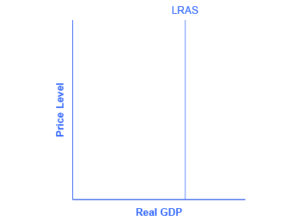

In the aggregate demand-aggregate supply model, potential GDP is shown as a vertical line. Neoclassical economists argue that the long-run aggregate supply curve is located at potential GDP—that is, the long-run aggregate supply curve is a vertical line drawn at the level of potential GDP, as shown in Figure 2. A vertical LRAS curve means that the level of aggregate supply (or potential GDP) will determine the real GDP of the economy, regardless of the level of aggregate demand. More precisely, given flexible prices, whatever the position of the AD curve, prices will adjust so that AD = AS at potential GDP.

Over time, increases in the quantity and quality of physical capital, increases in human capital, and technological advancements shift potential GDP and the vertical LRAS curve gradually to the right. This gradual increase in an economy’s potential GDP is often described as a nation’s long-term economic growth.

Glossary

- Modification, adaptation, and original content. Provided by: Lumen Learning. License: CC BY: Attribution

- The Building Blocks of Neoclassical Analysis. Authored by: OpenStax College. Located at: https://cnx.org/contents/vEmOH-_p@4.17:jHeoKD-2@5/The-Building-Blocks-of-Neoclas. License: CC BY: Attribution. License Terms: Download for free at http://cnx.org/contents/bc498e1f-efe...69ad09a82@4.44

- Potential and Actual GDP. Provided by: FRED. Located at: https://fred.stlouisfed.org/series/GDPPOT. License: Public Domain: No Known Copyright