7.19: Flow of Costs (Job Order Costing)

- Page ID

- 45869

Learning Outcomes

- Explain the flow of costs in a job order costing system

Let’s go back to Mitchell Manufacturing. They just received a new job for two custom bikes that are identical. The team has met and they have made their materials list. Purchasing has created a materials requisition form and they are bringing in the components needed to build the bikes. Accounting has created a job cost sheet that will follow the bikes through from production to delivery.

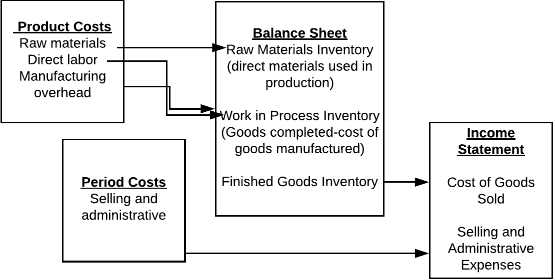

The flow of costs will look like:

So where will they start on their job costing system? Let’s start at the beginning:

- Materials requisition form is prepared with the items from the bill of materials (all the items needed for the job), quantities and costs that will go into the job. These are the direct materials from the cost flow diagram:

| Materials Requisition Number | 1800 | Date | 6/28/2018 | ||

|---|---|---|---|---|---|

| Job Number to be charged | 2912 | ||||

| Department | Production | ||||

| Description | Qty | Unit Cost | Total Cost | ||

| Spokes | 24 | $1 | $24 | ||

| Wheels | 4 | $25 | $100 | ||

| Frames | 2 | $110 | $220 | ||

| Screws and bolts | 16 | $1 | $16 | ||

| $360 |

2. Set up the job costing sheet:

This is where the numbers really start to come together. The job cost sheet includes a variety of information.

- Measure your direct labor cost—Remember that any labor not directly tracked to the manufacturing of a given item is included in your overhead. Most companies track their direct labor with a “time ticket” system, either on paper or electronically. With this system, the employee notes the time they are on each job.

- Add the manufacturing overhead that you already calculated.

- Total your costs, and you are all set!

The paper trail through the production process is helpful to track all of your expenses in one place. This can be provided to the accounting department, who can then properly allocate all of the costs to a job.

If you are a service business, most keep track of direct labor through a time tracking system, again, either manual or computerized. Companies use different systems based on their size and need.

An example of tracking direct labor and materials can be found HERE. This link provides another example, following an electrician through a job process. Each business is very different in the format that they use. Material requisition sheets, job tracking and numbering systems are all individual to the business. When you work as a manager the business you work for will introduce you to their system. The end result is the same, to find out how much it cost to produce the finished product for the job. As a reminder—this process is only used when there is more than one product being manufactured. Job costing would not be used at a plant that makes only one widget!

Practice Questions

- Flow of Costs (Job Order Costing). Authored by: Freedom Learning Group. Provided by: Lumen Learning. License: CC BY: Attribution