4.25: Account Categories

- Page ID

- 45812

Learning Outcome

- Identify general categories of accounts

Accounts in Accounting

The categories into which transactions are classified are called accounts, and, as you have seen, there are three broad categories: assets, liabilities, and equity. However, recording transactions into broad categories does not provide enough detail for managers to make decisions and actually use accounting information, so they are broken down further into more detailed accounts.

For instance, one of the most common accounts is the company checking account. Transactions such as paying bills decrease this account and making deposits increases the account. Assume an ending balance of $1,000 from last month in your company checking account. When you write a check for rent in the amount of $110, you subtract that from the balance. When you make a cash sale in the amount of $500 and deposit the cash into the bank, you increase the balance in your company records.

- Assets

- Checking account

- Beginning balance $1,000

- Check 101 ($110)

- Deposit $500

- Ending balance $1,390

- Checking account

Note that in accounting we usually show negative numbers in parenthesis instead of with a minus sign. The parenthesis are easier to see.

The list of transactions in a particular account is called a ledger. The ledger is chronological and includes the current balance. All of the accounts taken together are called the general ledger. Pre-computer, the general ledger was an actual book with a page (actually, pages) for each account.

The accounting ledger is a chronological listing of all financial transactions of a business, in date order.

In addition to the checking account, a company will have assets such as accounts receivable (amounts that customers owe the company), prepaid expenses (such as insurance paid in advance), and inventory (good held for sale in the ordinary course of business.) These account belong to a subclass of assets called current assets. Current assets are those assets that will turn into cash within the next twelve months. Long-term assets are those assets that would take longer than 12-months to convert them to cash and usually includes things such as land, equipment, building, furniture and fixtures.

In addition to current assets and long-term assets, the company tracks current and long-term liabilities. Current liabilities include accounts payable (amounts owed to vendors that have granted credit terms) and other payables like income tax, payroll taxes, and sales tax, as well as accruals such as wages payable. These current liabilities are those debts that must be paid within one ear or within the normal operating cycle of the business. On the other hand, long term liabilities include long-term debt and other debts that are due in more than 12 months.

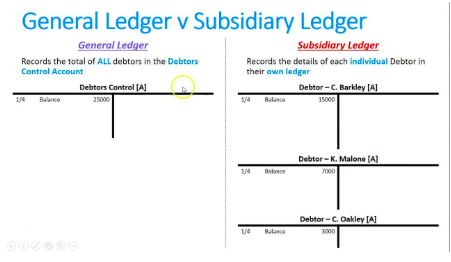

Control Accounts and Subsidiary Ledgers

Assets like accounts receivable and inventory are also called control accounts, since they show a balance, with transactions, that is backed-up by a subsidiary ledger. The account balance in the subsidiary ledger is the same as the account balance in the control account, but the subsidiary ledger is sorted by customer, in the case of accounts receivable, and by item in the case of inventory. For example, assume the accounts receivable general ledger account has a balance of $25,000. The subsidiary ledger would also have a balance of $25,000. The figure below illustrates the difference between a general and subsidiary ledger.

Any transaction posted to the general ledger control account would also be posted to the correct subsidiary ledger account. Thus, the control account and the subsidiary ledger always match. Because the general ledger account is a chronological listing of every transaction, it would be very difficult to find how much a particular customer owes at any given moment. That is the job of the subsidiary ledger.

Rather than relying on the chronological list of transactions in the general ledger, accounts like Office Furniture and Equipment are control accounts supported by a matching subsidiary ledger. Suppose the general ledger account showed a balance of $5,000:

- Equipment

- Balance forward$2,000

- Purchase of computer$1,600

- Purchase of desk$1,400

- Ending balance$5,000

- Balance forward$2,000

The subsidiary ledger would also show $5,000, but would be listed by item instead of chronological by transaction:

- Equipment subsidiary ledger

- Computer: $1,600

- Desk: $1,400

- Printer: $1,200 (purchased in the prior period)

- Water cooler: $800 (purchased in the prior period)

What are the equity accounts?

The equity accounts include capital contributions by the owner(s) and withdrawals. In short, equity is the value of the owner’s investment in the business. It is made up of all of the owner’s contributions to the business (in the form of cash) as well as accumulated earnings that have not been distributed to the owner. In equity accounts, capital contributions increase equity and withdrawals decrease equity

What about business revenues and expenses?

Expenses are the costs of doing business. In fact, the word expense comes from the word expenditure, which means, “used up.” So, as resources are used up to generate income, they are recognized as expenses. Common business expenses include rent, salaries, advertising, administrative expenses and insurance. On the other hand, revenues are the income generated by the company. Revenue may be earned by providing goods or services as well as earnings from investments. In short, revenue is the generation of wealth for the owners, and therefore increases owners’ equity, while expenses are the consumption of resources, and therefore decrease owners’ equity.

Key Takeaways

These categories are summarized below:

- Assets. Items of financial value that the business controls (“owns”) for the purpose of producing income for the owners.

- Liabilities. Monies that the business owes to non-owners.

- Owners Equity. The theoretical value of the business that would be distributed to the owners after the assets were sold and the liabilities paid.

- Revenue. Payments made to the business by customers for the goods and/or services provided by the business.

- Expenses. Costs incurred by the business in providing the goods and/or services purchased by the customers.

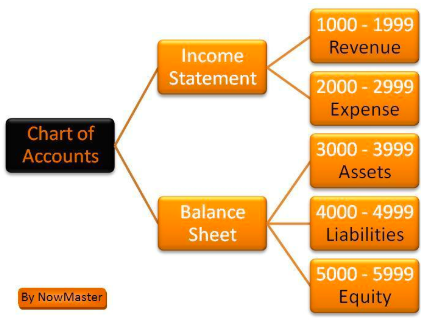

The Chart of Accounts

The following chart of accounts is a summary of various common accounts arranged by classification:

- Assets

- Current Assets

- Checking

- Savings

- Accounts Receivable

- Inventory

- Prepaid Expenses

- Long-term assets

- Equipment

- Land

- Buildings

Furniture - Vehicles

- Other long-term assets (intangible)

- Intellectual property

- Goodwill

- Long-term investments

- Current Assets

- Liabilities

- Current Liabilities

- Accounts Payable

- Sales Tax Payable

- Income Tax Payable

- Wages Payable

- Unearned Revenue

- Long-term Liabilities

- Long-term debt

- Current Liabilities

- Equity

- Owners’ Capital

- Withdrawals

- Revenue

- Sales Revenue

- Service Revenue

- Expenses

- Salaries and Wages

- Rent

- Insurance

- Taxes

Note that every business will have a different chart of accounts based on its business activities.

Practice Questions

- Account Categories. Authored by: Freedom Learning Group. Provided by: Lumen Learning. License: CC BY: Attribution

- account groups (KEY TAKEAWAYS). Authored by: Peter Baskerville. Located at: https://flic.kr/p/cHAMty. License: CC BY-SA: Attribution-ShareAlike

- accounts structure. Authored by: Peter Baskerville. Located at: https://flic.kr/p/cHAMz1. License: CC BY-SA: Attribution-ShareAlike