3.6: Putting It Together- Accounting Theory

- Page ID

- 45806

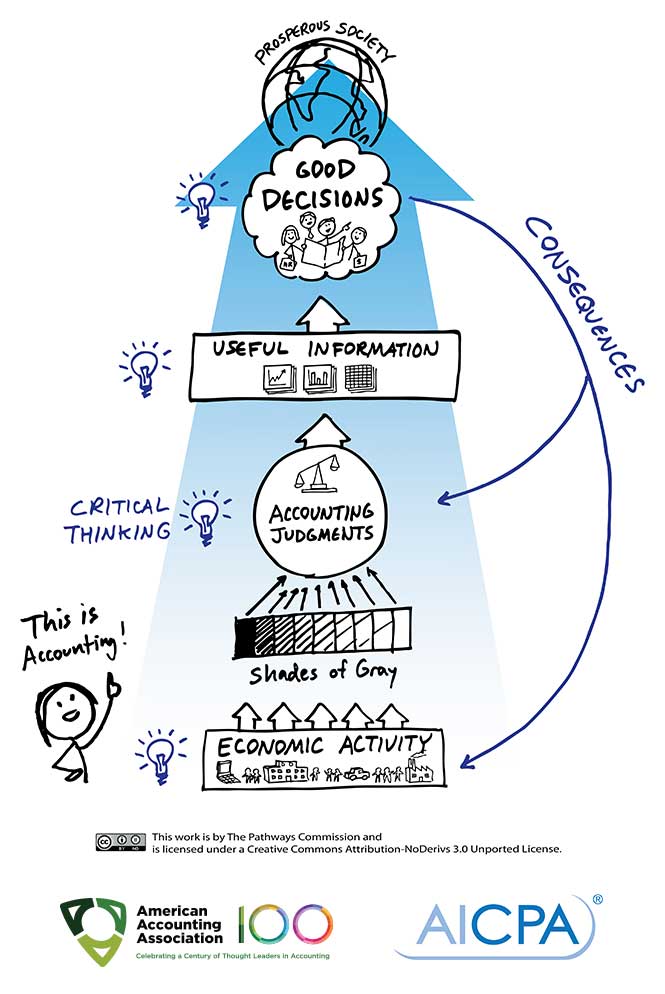

Accountants take massive amounts of data and turn it into useful financial information. It’s the accountant’s job to communicate that financial information, but it is the user’s responsibility to learn the language in order to be able to use the information to make an informed decision, whether it is for long-term investing (as in your retirement plan) or for business planning and operating issues.

Accrual basis accounting may seem complicated. Why bother? Why not keep it simple and just report cash in and cash out? To answer those questions, let’s think about the landscaping example from earlier in this chapter, but let’s make our business this time a carrier, like FedEx and UPS. Assume your target market is Business to Business (B2B) so you do a lot of work on credit. In a summer month you haul packages and bill $1,000,000 to your customers as realizable revenue, and in November and December that amount is triple the summer average, but since you bill your customers, you collect the cash a month or two later. Accrual basis accounting is an economic measure of the health of your business, so we report $3,000,000 in revenue in November, even though it will be collected in December and January. In addition, under accrual basis accounting, we record the increased expenses, like jet fuel and wages, in the same month they are incurred, even though we are paying our suppliers a month later. Recognizing revenues as earned and expenses as incurred gives us an accurate indication of the amount of wealth we earned in November, without regard to the cash flows (this is why we have a statement of cash flows in addition to an income statement.)

So financial accountants follow the sometimes complex rules of accounting under GAAP in order to give reliable, consistent, and relevant financial information to outside users. In so doing, they use their best judgment about which accounting principles to apply in order to provide the best information in each situation. The same goes for managerial accountants who are providing information to internal users. Even though they don’t have to follow GAAP, they are required by the demands of management to provide the same level of useful, timely, and reliable information.

All of this so that you, as a business owner or an investor, can make informed business and investing decisions.

In our society, a robust, well-run business adds to the overall quality of life by creating jobs, products, and opportunities, so it is important that the financial information the company produces is useful, relevant, and timely. And that, in a nutshell, is what accounting is all about.

- Putting It Together: Accounting Theory. Authored by: Joe Cooke. Provided by: Lumen Learning. License: CC BY: Attribution